Are you among the many people who have resolved to make smart money practices to lead a healthy financial life and create wealth in this New Year?

If yes, then, you would agree that a disciplined approach to investing will take you far ahead in this journey.

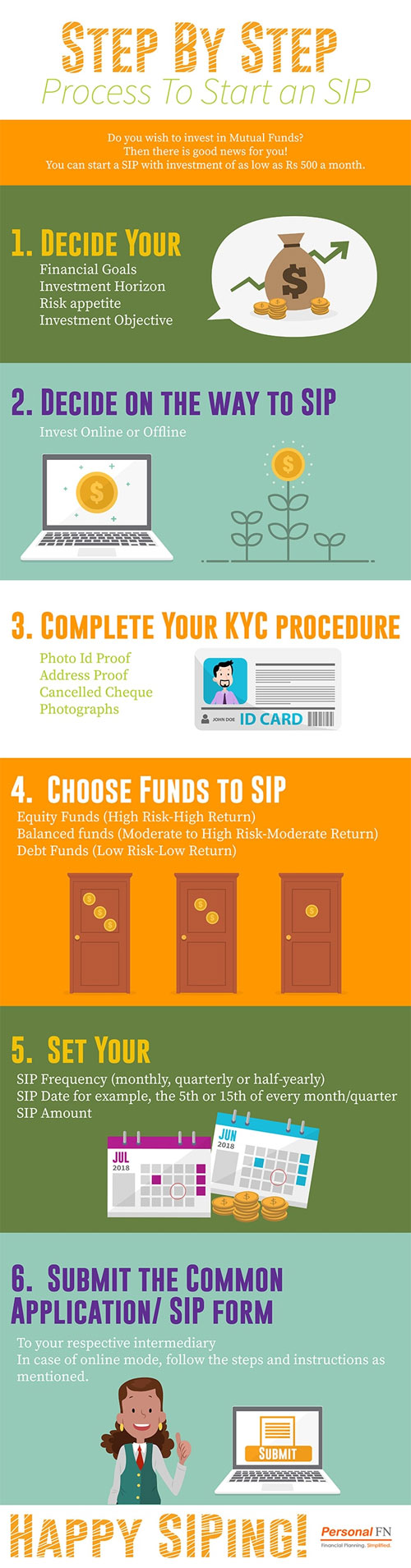

Building a portfolio of the best mutual funds and investing through the SIP mode is one of the most efficient ways to do it.

photo created by freepik - www.freepik.com

Many times, investing a lump sum in mutual funds becomes a risky proposition. This is where Systematic Investment Plan (SIP) comes to the rescue. With SIP, you can invest on a daily basis, monthly basis, or on a quarterly basis in a mutual fund scheme of your choice. This investment amount can be as low as Rs 500 per month.

SIP has made life easy -- it's lighter on the wallet, you don't need to time the market to generate wealth, you inculcate the habit of investing regularly, and it is an effective medium to accomplish vital financial goals such as, buying a dream home, children's education needs, their marriage, and your retirement, among others.

As it's said, "little drops of water make a mighty ocean"; SIP just does that. If you follow the right discipline and ensure that you do not miss or stop SIP instalment, it can help you achieve the envisioned financial goals.

Table: Top ranking schemes based on 3-year SIP return

SIP returns are XIRR %, Lump sum returns are CAGR %

Data as on January 06, 2020

(Source: ACE MF)

*Please note, this table only represents the best performing Mutual Funds based solely on past returns and is NOT a recommendation. Mutual Fund investments are subject to market risks. Read all scheme related documents carefully. Past performance is not an indicator for future returns. The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

Out of the diversified equity schemes analysed, Axis Bluechip Fund, IIFL Focused Equity Fund, Axis Focused 25 Fund, Axis Midcap Fund, and SBI Focused Equity Fund stood as the top performers based on 3-year SIP returns. The top performing schemes delivered double-digit returns across period. As we can see in the table above, over the longer horizon of 5-years, SIP returns were higher than lump sum returns. This goes on to show that SIP is a worthy mode for your long term goals.

Regular investment through SIP helps to average out the cost of investment and compound your wealth. Through the SIP mode, you can buy more units when the markets are low, so when the market bounces back, it results in higher returns. And if market volatility, such as the one we witnessed in the last couple of years, makes you wary, taking the SIP route would help you mitigate the risk.

But make sure that you select the best schemes that align with your financial goals, risk appetite and investment horizon. While equity investment have the potential to generate high returns, don't ignore the risk involved, and select funds that are most suited for you -- as per the asset allocation meant for you.

Your equity SIP portfolio should contain a fair proportion of large-caps and mid-caps, as well as growth and value-styled schemes for optimum diversification. Pick funds using stringent rating parameters. Some schemes perform well over the shorter time horizon but they may not necessarily generate higher returns over the long term. Therefore, select funds that perform well across market phases and cycles as compared to the benchmark and category peers.

[Read: The Special Care to Select the Best Mutual Funds in 2020]

Here are the other parameters you need to look into to select the best mutual fund for SIP:

Quantitative Parameters:

-

Performance and risk analysis

Analyse if the fund has shown consistency in performance across various market periods with decent risk-adjusted returns.

Under this, you need to rank the fund based on quantitative parameters like rolling returns across short-term and long-term periods, such as a 1-year, 3-year, and 5-year timeframe, and on risk-reward ratios like Sharpe Ratio, Sortino Ratio, and Standard Deviation over a 3-year period.

-

Performance across market cycles

You need to ensure that the fund has the ability to perform consistently well across multiple market cycles. Therefore, compare the performance of all the available funds in a particular category vis-a-vis their benchmark index as well as category peers across bull phases and bear market phases.

A fund that performs well on both sides of the market should rank higher on the list.

Qualitative Parameters

-

Portfolio Quality

Adequate Diversification - The scheme should not hold a highly concentrated portfolio. It should have a well-diversified portfolio and the exposure to the top-10 holdings should be ideally under 50% while concentration to one particular sector should not exceed 30-35%.

Low Churn - Engaging in high churning can result in higher cost impacting the overall return of the scheme. Therefore, you also need to consider the portfolio turnover ratio and expenses, and penalise funds involved in high churning, i.e. those funds with a turnover ratio of more than 100%.

-

Quality of Fund Management

You must consider the fund manager's experience, workload, and the consistency of the fund house. Therefore, assess the following criteria:

The fund manager's work experience - He/she should have a decent experience in investment research and fund management, ideally over a decade.

The number of schemes managed - A fund manager usually manages multiple schemes. Thus, you need to check if the fund manager is burdened with managing a large number of schemes. If he is managing more than five open-ended funds, it should raise a red flag.

The efficiency of the fund house in managing your money - Research about the fund house's performance across schemes; find out if only a few selected schemes are doing well. A fund house that performs well across the board is an indication of sound investment processes and risk management techniques in place.

Yes, we know that the above list is a lot for an average investor to look at. It involves a lot of number crunching and much of the data is not easily available in one place. But if you do need to narrow down on the top funds, these factors are of utmost importance.

Watch this short video on selecting mutual fund schemes:

At PersonalFN, we select and recommend mutual funds on quantitative and qualitative parameters using our S.M.A.R.T Score Matrix:

-

S - Systems and Processes

-

M - Market Cycle Performance

-

A - Asset Management Style

-

R - Risk-Reward Ratios

-

T - Performance Track Record

Editor's Note:

If you wish to select worthy mutual fund schemes, I recommend you subscribe to PersonalFN's unbiased premium research service, FundSelect.

PersonalFN's mutual fund recommendations tend to beat the market by a significant margin over long time periods. FundSelect has beaten the market by over 70% in a decade.

Each fund recommended under FundSelect goes through our stringent process, where they are tested on both quantitative as well as qualitative parameters.

Every month,PersonalFN's FundSelect service will provide you with insightful and practical guidance on equity mutual funds and debt schemes - the ones to Buy, Hold, or Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Author: Divya Grover