The Indian equity market is near its all-time high, sailing over the 30,000 mark on the S&P BSE Sensex and the 9,500-mark on the NSE's Nifty 50. Valuations-wise the Indian equity market seems expensive. During such times investing your hard-earned money at one go, in lump sum, can prove perilous. Hence, opting for the SIPs (or Systematic Investment Plan) instead would be a prudent approach, especially when you're addressing to long-term financial goals.

First, let's understand what is meant by SIP…

Simply put, a SIP refers to Systematic Investment Plan which is mode of investing in mutual funds in a systematic and regular manner. The method of investing is similar to your investment in a recurring deposit (RD) with a bank, where you deposit a fixed sum of money (into your recurring deposit account), but the only difference here is, your money is deployed in a mutual fund scheme (equity schemes and / or debt schemes) and not in a bank deposit, and hence your investments (in mutual funds) are subject to market risk.

A SIP enforces a disciplined approach towards investing, and infuses regular saving habits which we all probably learnt during our childhood days when we used to maintain a piggy bank. Yes, those good old days where our parents provided us with some pocket money, which after expenditure we deposited in our piggy banks and at the end of particular tenure we saw that every penny saved became a large amount.

SIPs too work on the simple principle of investing regularly which enable you to build wealth over the long-term. In case of SIPs, on a specified date which can be on a daily basis, monthly basis, or on a quarterly basis, a fixed amount as desired by you, is debited from your bank account (either through a ECS mandate or through post-dated cheques forwarded) and invested in the scheme as selected by you for a specified tenure (months, years).

Today some Asset Management Companies (AMCs) / mutual fund houses / robo-advisory platforms also provide the ease and convenience of transacting online. They have set up their own online transaction platforms, where one can do SIP investments by following the procedure as made available on the websites.

So, you have fewer hassles while investing as well as tracking your investment dates.

Here are 5 benefits of SIPs:

1. SIPs are light on the wallet

SIPs enable you to invest in smaller amounts at regular intervals (daily, monthly or quarterly). This in turn reduces your burden of defraying a lump-sum - at one go - from your bank account.

If you cannot invest Rs 5,000 in one shot, that's not a huge stumbling block, you can simply take the SIP route and trigger the mutual fund investment with as low as Rs 500 per month.

2. SIPs make market timing irrelevant

SIPs can help you manage (even-out) the market volatility well. Timing the market can be hazardous to your wealth and health. Instead focus on ‘time in the market’ in the endeavour to create wealth by selecting the best mutual fund scheme to invest.

Studies have repeatedly highlighted the ability of equities to outperform other asset classes (debt, gold, even real estate) over the long-term (at least 5 years) and are effective to counter inflation.

Now one may ask: If equities are such a great thing, why are so many investors complaining? Well it’s because they either got their stock or the mutual fund wrong or the timing wrong. In our opinion both these problems can be solved through a SIP in a mutual fund with a steady track record, stay invested for the long-term as the SIP route enables you to even-out the volatility of the equity markets effectively.

3. SIPs enable rupee-cost averaging

Many a time, a SIP works better as opposed to one-time, lump sum investing. This is because of rupee-cost averaging. Under rupee-cost averaging you would typically buy more of a mutual fund unit when prices are low, and similarly, buy fewer mutual units when prices are high. This infuses good discipline since it forces you to commit cash at market lows, when other investors around you are wary and exiting the market. It also enables you to lower the average cost of your investments.

4. SIPs benefit from the power of compounding

As SIPs subscribe you to the habit of investing regularly, it enables you to compound your money invested. So, say you start a SIP of Rs 1,000, in a mutual fund scheme following prudent investment system and processes, with a SIP tenure of 20 years and expect a modest return of 15% p.a., your money would grow to approximately Rs 15 lakh.

So, over the long-term, SIPs can compound wealth better and systematically as opposed to investing a lump sum, especially when the journey of wealth creation is volatile.

5. SIPs are effective medium for goal planning

All of us have financial goals – may be buying a house, buying a dream car, providing good education to children, getting them (children) married well, retiring etc. But all this comes with systematic financial planning. Very often many invest in the equity markets, with a motive of making short-term gains, and often ignore to use the equity markets as a window for long-term wealth creation, in order to achieve one's financial goals. You can effectively achieve your financial goals by enrolling for SIPs. The earlier you start the better it is.

Despite the benefits, many investors have some misbeliefs about SIPs owing to incorrect information shared by friends, family, brokers etc.

7 common myths on SIPs debunked

Myth#1: Only Small investors go in for SIP

Please note that SIP stands for Systematic Investment Plan (SIP) and not Small Investors Plan. Hence, it is incorrect to be under the illusion and arrogance that SIP, is meant only for small investors.

SIP is for everyone, if you wish to create wealth systematically. Just as a piggy bank and recurring deposit subscribes you to habit of saving regularly with the needed discipline, even SIPs do. And you a better rate of return as against parking money in fixed deposits, recurring deposits and endowment policies offered by insurance companies. By investing your savings in a systematic manner –daily, monthly, quarterly -- for a said tenure (period of SIP) helps you build a corpus earning a rate of return, in order to attain your financial goal.

Myth #2: Rupee cost averaging is possible through investing in stock too – then why SIP?

A SIP experimented on single scrip, can expose you to more volatility unlike SIP in mutual funds which reduces the risk, due to benefit of diversification, professional fund management and liquidity offered by mutual funds.

Moreover, as per the market cap bias (i.e. large cap, mid cap and small cap) which a fund follows, you can also strategically structure your portfolio depending upon your risk appetite. Likewise, you can structure your portfolio on the basis of the style (viz. value, growth, blend, opportunities, flexi-cap, multi-cap etc.) of investing followed by the mutual fund. And by adopting the SIP mode of investing for mutual funds, you'll draw two major benefits: rupee cost averaging and compounding.

Myth #3: SIP mutual funds are different from lump sum mutual funds

Well many have this delusion. The fact is, there are no special schemes for SIP investments. SIPs are just a mode of investing.

Myth #4: Lump sum investments cannot be done in a scheme, where a SIP account exists

SIP as you know by now, is just a mode of investing in mutual funds. Hence, pumping a lump sum amount to a mutual fund where your SIP exists is possible. So, say you have a SIP of Rs 1,000 going on in a mutual fund scheme and suddenly you have a surplus of say Rs 50,000, you can pump a lump sum amount to your on-going Rs 1,000 SIP account.

Myth #5: I'll be penalised if I miss one or two SIP dates

While enrolling for the SIP mode of investing you are required to provide a NACH (National Automated Clearing House) mandate from NPCI (National Payments Corporation of India) form along with the common application form. Your SIP details (as selected) are already mentioned in this mandate apart from the SIP form, thus your bank at regular SIP dates keeps debiting the SIP amount in favour of the fund where you have opted a SIP. The start date and end date is mentioned in these forms. You also furnish has your contact details so that you're update on your transactions. Hence, the question of missing dates usually doesn't arise.

However, for some reason – say, you haven't maintained the balance in your bank account – and a SIP instalment doesn't get debited, you simply miss that instalment, but the folio / account remains active for further SIPs to debit from the bank account. So, it's not like the EMI (Equated Monthly Instalment) of your loan, where you miss an instalment; you are penalised.

Similarly, if you're facing financial crunch, today fund houses also allow you to pause your SIPs for period of 1 to 3 months until normalcy returns. So, a short-term crunch should not be a cause of worry for your SIPs. SIP pause facility is explained at great length in ensuing part of this editorial piece.

Myth #6: Markets are high to start a SIP

Well, if that's what you think, then you should be starting a SIP immediately. That's because as the market corrects you would by accumulating more number of units, with every fall in the NAV, thus enabling you to lower you average purchase cost. And, as the markets, post the correction surge once again, you would gain as the yield will work to be higher.

Myth #7: In a tax saver SIP, entire money can be withdrawn after 3 years

In case of a SIP in tax saving mutual funds (commonly known as Equity linked Saving Schemes – ELSS), very often a delusion exists that, the entire investment in a tax saving mutual fund can be withdrawn once the lock-in period is over. But that's not the case!

The fact is: your every instalment of SIP should have completed the lock-in tenure. So say if you put in Rs 5,000 through SIP in the month of January 2017, the lock-in period for only 1 instalment (i.e. January 2012) will get over on January 2020. While other SIP instalments need to complete 3 years as well.

5 Types of SIP

Mutual fund houses while offering SIP facility have been receptive to what investors want. Thus over the years, SIPs have been transformed, they've evolved.

Mutual fund houses have added several new features to the plain vanilla SIP to complement the regular form of investing. So, let's see what more you can do with your monthly SIP…

1. Step-up SIP or Top-up SIP

Step-up SIP (also known as Top-up SIP) enables you to increase your SIP amount at regular intervals. This is helpful especially in goal planning, where you say you have a windfall income or bonus and want to invest. So, you can start with a small amount initially and gradually increase the amount you invest. Consequently, as our income increases, so do our expenses. Therefore, increasing your investment level will protect you on rainy days.

Many a times, investors continue the same monthly investment through SIP for over 5-7 years. Though they may have earned good returns on the investment, they would have lost out on earning an additional income had they topped up or stepped-up their SIP. Adding up the SIP amount regularly is an easy way to build up wealth.

To add on, you have an option to have a fixed or variable top-up (Top-up Cap) amount and a Cap Year. You can either set a fixed limit to your top-up amount or keep it variable. Also, you can set a date until when you would wish to continue your top-up facility.

Top-up option must be specified at the time of enrolment. The amount can be as low as Rs 500 and in multiples of Rs 500 only. Further, the top-up details cannot be modified once enrolment is done. Hence, be sure before applying for it. A half yearly and yearly SIP top-up frequency is available for monthly SIP. Quarterly SIP offers top-up frequency at yearly intervals only. If you miss out on informing your top-up frequency it is assumed to be at yearly intervals.

2. Flex SIP

At times if you do not wish to SIP owing to uncertain cash flows, you can opt in for flex SIP (also known as flexible SIP) and still stay invested. With this, you can adjust your instalment as you would want. Not only this, you can even opt for a trigger-based option (explained in the following point). For example, if you are rewarded by a bonus of Rs 1,00,000, with the help of Flex SIP, you can allocate the investible surplus to directly into one of the funds of your existing portfolio. This gives you the flexibility to either increase or decrease the amount in any particular month.

3. Trigger SIP

This facility is more viable if you are experienced as it involves some amount of awareness and knowledge.

With Trigger SIP, you can set either an index level, NAV, date or an event. This is to take advantage of any movement in anticipation. For example, if you know a certain kind of Government policy is due next week and that will impact the index crossing a certain mark, you can set it as a trigger date.

Similarly, you can set trigger target for your fund NAV appreciation/ depreciation (in percentage terms) or capital appreciation or depreciation trigger.

However, PersonalFN believe this could induce speculative habit and should be avoided. Best is to always have a long-term view in mind to achieve your set of financial goals.

4. Perpetual SIP

Usually when signing up a SIP mandate, you must enter the start and end date. This is for a pre-decided term period say 1 year, 2 years, 3 years, 5 years, etc. And once the SIP matures, many a times investors tend to procrastinate and delay renewal due to operational hassles. In turn, they end up missing few instalments, which upsets the saving discipline and affect returns in the long run.

If you leave the end date block blank in a SIP mandate, by default you opt for perpetual SIP. Most fund houses will assume this SIP to continue till 2099, unless you submit/provide a written communication to the fund house. So, once you achieve your goal corpus, you can redeem your funds as per your convenience.

5. Pause SIP

God forbid, but when in a financial crunch or crisis, you can even pause SIP instalments instead of stopping SIPs altogether and impeding your path to systematic wealth creation. By doing so you don't have to undergo the process of re-starting SIPs all over again.

As mentioned before, you can stop SIPs for period of 1 to 3 months until normalcy returns. This will give you the needed relief for those few months under distress.

Here are steps to pause your SIPs…

✔ Submit the pause form to the mutual fund house (or the AMC) and send an instruction. The form can be downloaded from the mutual fund house's (or the AMC's) website or sourced from the Investor Service Centre.

✔ Submit a Bank Mandate.

Once the form is submitted, do not forget to instruct your bank to stop the auto debit service or stop the post-dated cheque. If you miss out on the bank's mandate, they might charge you for dishonour of payment.

Once your pause period is over, ideally, you should resume your SIP. Proactively ensure, that you aren't jeopardising your long-term financial wellbeing.

Keep in mind that not all mutual fund houses provide the Pause-a-SIP facility. Therefore, it is best to check whether the option is available at the time of registration. Also, bear in mind that pause facility is usually offered only once the whole tenure of your investment.

Although pausing a SIP is option, that provides suppleness to sail through turbulence, avoid pausing (or even cancellations of) a SIP; because in effect it hinders the path to wealth creation and accomplishing your financial goals. Instead, adopt utmost financial discipline and be focussed to achieve your long-term financial goals. Engage in prudent budgeting exercise and maintain a sufficient contingency fund, which can act as a protective shield in times of emergency.

Remember, the key to financial freedom is perseverance

Are there any best SIPs?

Well, by now you know that that SIPs are a medium to invest in mutual funds. Hence, there's nothing like 'best SIPs'; you need to select best or winning mutual fund schemes to invest so that SIPs work best for your objective of wealth creation to achieve long-term financial goals.

So, selecting an appropriate mutual fund scheme for your SIPs is very crucial.

How does one select the best mutual fund schemes to SIP?

While some may say – "I can simply do that going by mutual fund ratings". But the fact is, you can't have blind faith to star ratings, as they are often provided taking into account only few quantitative parameters (such as returns, risk, average AUM (Assets Under Management) etc., thereby ignoring the qualitative parameters. Besides, ratings subscribe to a 'one size fits all' approach. Remember investing and financial planning are personalised activities. So, a fund could be right for one investor and (despite its sterling performance) be completely unsuitable for another. Yes, they could perhaps serve as starting points for identifying a broader set of investment-worthy funds; but investing in a fund, based solely on number of stars against its name may not be the right move.

The fact is, not all mutual funds are same. There are various aspects within a mutual fund scheme, which are vital for investors to study carefully before investing; which are:

-

Performance: The past performance of a fund is important in analysing a mutual fund. But, remember that past performance is not everything, as it may or may not be sustained in future and therefore should not be used as a basis for comparison with other investments.

It just indicates the fund’s ability to clock returns across market conditions. And, if the fund has a well-established track record, the likelihood of it performing well in the future is higher than a fund which has not performed well.

Under the performance criteria, we must make a note of the following:

-

Comparison: A fund’s performance in isolation does not indicate anything. Hence, it becomes crucial to compare the fund with its benchmark index and its peers, so as to deduce a meaningful inference. Again, one must be careful while selecting the peers for comparison. For instance, it doesn’t make sense comparing the performance of a mid-cap fund to that of a large-cap. Remember: Don’t compare apples with oranges.

-

Time period: It’s very important that investors have a long-term horizon (of at least 3-5 years) if they wish to invest in equity oriented funds. So, it becomes important for them to evaluate the long-term performance of the funds. However this does not imply that the short term performance should be ignored. Besides, it is equally important to evaluate how a fund has performed over different market cycles (especially during the downturn). During a rally it is easy for a fund to deliver above-average returns; but the true measure of its performance is when it posts higher returns than its benchmark and peers during the downturn. Remember: Choose a fund like you choose a spouse - one that will stand by you in sickness and in health.

-

Returns: Returns are obviously one of the important parameters that one must look at while evaluating a fund. But remember, although it is one of the most important, it is not the only parameter. Many investors simply invest in a fund because it has given higher returns. In our opinion, such an approach for making investments is incomplete. In addition to the returns, one also needs to look at the risk parameters, which explain how much risk the fund has undertaken to clock higher returns.

-

Risk: To put it simply, risk is a result or outcome which is other than what is / was expected. The outcome, when different from the expected outcome is referred to as a deviation. When we talk about expected outcome, we are referring to the average or what is technically called the mean of the multiple outcomes. Further filtering it, the term risk simply means deviation from average or mean return.

Risk is normally measured by Standard Deviation (SD or STDEV) and signifies the degree of risk the fund has exposed its investors to. From an investor’s perspective, evaluating a fund on risk parameters is important because it will help to check whether the fund’s risk profile is in line with their risk profile or not. For example, if two funds have delivered similar returns, then a prudent investor will invest in the fund which has taken less risk i.e. the fund that has a lower SD.

-

Risk-adjusted return: This is normally measured by Sharpe Ratio (SR). It signifies how much return a fund has delivered vis-à-vis the risk taken. Higher the Sharpe Ratio better is the fund’s performance. As investors, it is important to know the same because they should choose a fund which has delivered higher risk-adjusted returns. In fact, this ratio tells us whether the high returns of a fund are attributed to good investment decisions, or to higher risk.

-

Portfolio Concentration: Funds that have a high concentration in particular stocks or sectors tend to be very risky and volatile. Hence, investors should invest in these funds only if they have a high risk appetite. Ideally, a well-diversified fund should hold no more than 50% of its assets in its top-10 stock holdings. Remember: Make sure your fund does not put all its eggs in one basket

-

Portfolio Turnover: The portfolio turnover rate refers to the frequency with which stocks are bought and sold in a fund’s portfolio. Higher the turnover rate, higher the volatility. The fund might not be able to compensate the investors adequately for the higher risk taken. Remember: Invest in funds with a low turnover rate if you want lower volatility.

-

Fund Management: The performance of a mutual fund scheme is largely linked to the fund manager and his team. Hence, it’s important that the team managing the fund should have considerable experience in dealing with market ups and downs. As mentioned earlier, investors should avoid fund’s that owe their performance to a ‘star’ fund manager. Simply because if the fund manager is present today, he might quit tomorrow, and hence the fund will be unable to deliver its ‘star’ performance without its ‘star’ fund manager. Therefore, the focus should be on the fund houses that are strong in their systems and processes. Remember: Fund houses should be process-driven and not 'star' fund-manager driven.

-

Costs: If two funds are similar in most contexts, it might not be worth buying mutual fund scheme which has a high costs associated with it, only for a marginally better performance than the other. Simply put, there is no reason for an AMC to incur higher costs, other than its desire to have higher margins.

The two main costs incurred are:

-

Expense Ratio: Annual expenses involved in running the mutual fund include administrative costs, management salary, overheads etc. Expense Ratio is the percentage of assets that go towards these expenses. Every time the fund manager churns his portfolio, he pays a brokerage fee, which is ultimately borne by investors in the form of an expense ratio. Remember: Higher churning not only leads to higher risk, but also higher cost to the investor.

-

Exit Load: Due to SEBI’s ban on entry loads, investors now have only exit loads to worry about. An exit load is charged to investors when they sell units of a mutual fund within a particular tenure; most funds charge if the units are sold within a year from date of purchase. As exit load is a fraction of the NAV, it eats into your investment value. Remember: Invest in a fund with a low expense ratio and stay invested in it for a longer duration.

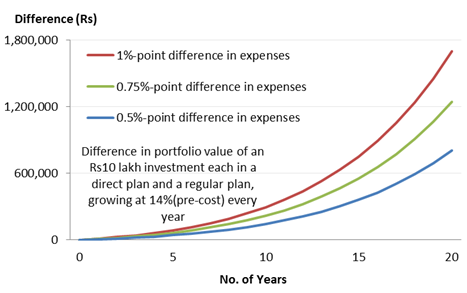

Notwithstanding the above when you invest in mutual funds make it a point to opt for the ‘Direct Plans’ over ‘Regular Plan’. The mutual fund direct plans make a positive difference to your investments every year. These plans generate roughly 0.5% to 1.0% additional returns every year, thanks to lower costs – mainly the expense ratio. By opting for the direct plan you eliminate the services of a mutual fund distributor / agent / relationship manager. The transaction may be performed online or even physically by visiting the registrar’s or the asset management company’s office.

It may not seem much at first, but, if you sow seeds of these small savings, you may harvest rich rewards over 15- 20 years — thanks to the power of compounding .

Save Huge Costs Over The Long Term

For illustration purpose only

(Source: PersonalFN Research)

As can be seen in the chart above, a small difference in costs can result in savings of anywhere between Rs8-17 lakh over 20 years, on a Rs10 lakh investment. Yes, you can earn an additional amount of as much as Rs17 lakh, if the difference in costs is as much as 1% point. The final portfolio value varies with the magnitude difference in expenses. Every 0.25%-point difference in the expense ratio works out to an additional earning of Rs4.50 lakh in 20 years' time, if Rs10 lakh is invested.

This Rs 10 lakh investment is just as assumption. In reality, if you are saving for your long-term goals such as retirement, you will be targeting a corpus of over Rs1 crore for sure. Just imagine the costs then. Surely, you do not want to lose your hard-earned money in the form of costs that can be easily avoided. Moreover, the additional saving to such an extent can make huge difference to your financial goals.

The time has come to ask yourself and judge: Are you compromising on long-term returns for a little comfort in the short-term by availing services of mutual fund distributors, or is there a real value.

SIP vs. Recurring Deposits: Which is better?

Do you reminisce about visiting a post office or bank with your parents to deposit their savings / investible surplus every month into a recurring deposit (RD)?

Perhaps as you grew up and started earning, they might have even pestered you to subscribe to this regular investing habit.

But those were the good old days of saving regularly through banks and post office schemes, although it required patience to stand in long queues. But it was worth it as interest rates were high then.

However, times have changed and today interest rates on bank fixed deposits and recurring deposits are at their multi-year low…and if RBI reduces policy rates abetted by mellowing inflation, deposit rates would go further down.

Besides, in contemporary time that we're in, it's time to embrace new investment avenues. You need to look for promising wealth creating investment avenues for a bright financial future, where you can accomplish many of your financial goals, viz. buying a dream, a car, providing the best education to your children, getting them married in style, travelling abroad for leisure, and living a blissful retirement, and so on …and use technology in investing.

Mutual funds have merits such as:

✔ Diversification;

✔ Professional management;

✔ Lower entry level;

✔ Economies of scale; and

✔ Liquidity

Moreover, today mutual fund houses provide innovative plans and services. There are two modes of investing: Systematic Investment Plans (SIPs); and Systematic Transfer Plans (STPs).

If you select winning or best mutual fund schemes for your portfolio that have exhibited a consistent performance track record and are from fund houses with follow strong investment processes and system, they've demonstrated their worth. And if you take the SIP route to invest in mutual funds, even volatility isn't issue as it get mitigate vide the benefit of rupee-cost averaging offered by mutual funds.

Yes, SIPs are subject to market risk, while in RDs you earn a fixed rate of interest. But here are 4 reasons why SIPping into mutual funds is better than bank RD…

-

Tax benefits

In case of RDs, tax is deducted at source if interest income exceeds Rs 10,000. But that’s not all. The interest income added to your ‘return of total income’ income as ‘income from other sources’, and the tax liability is determined as per one’s tax slab.

On the other hand, SIPs in mutual funds is far more efficient.

When you invest in equity mutual funds and stay invested for period of at least 1 year, the capital gains earned, are tax free. If you sell the equity mutual fund units before a year, the gains will attract a short-term capital gain tax @15%.

Likewise, when you invest in a debt mutual fund scheme vide a SIP and stay invested for holding period of at least 3 years, although the capital gain is taxable, you enjoy a indexation benefit (for inflation) and the Long Term Capital Gain (LTCG) tax payable is @20%. This is far better than paying tax as per your tax slab, particularly when you’re in the highest tax bracket. However, in case of debt mutual fund schemes if the holding period is less than 3 years, the tax levied will be as per you tax slab.

-

Better risk–return trade-off

For the risk you take (which is a function of your age, income, expenses, assets & liabilities, investment horizon, and financial goals), SIPs in mutual funds can prove worthy to achieve your financial goals.

However, take enough care to select mutual fund schemes your portfolio and have a high risk appetite along with an investment horizon of at least 5 years. The average returns generated by diversified equity mutual funds in last 5 years are around 18% CAGR.

When you consider the tax angle and inflation, returns in RD are meagre. As a result achieving some of the vital financial goals in life can be a challenge. Most RDs give around 6.0%-7.5% interest per annum.

-

Mitigate volatility

As mutual funds invest in market-lined securities such as stocks and bonds, your investments are subject to market risk — there is a significant amount of volatility. But, as mentioned before, with SIPs, volatility can be mitigated due to rupee-cost averaging.

Comparatively RDs, while they generate fixed returns and are not volatile, may not help you achieve your vital financial goals due to the meagre real rate of return.

-

Penalty

When you miss a SIP instalment, you’re not penalised – there’s no penalty charged. However, if you miss your SIP payment for three consecutive months, the SIP mandate will get terminated. Having said that, whatever you’ve invested until then, will continue to earn you returns.

On the other hand, if you miss out an instalment in RD in any particular month, usually a penalty would be levied. Moreover, if you wish to withdraw before maturity you will again attract some amount of penalty.

To conclude…

Recurring deposit and SIPs both inculcate discipline and regular investing habit. But for your long-term financial wellbeing, where you need tax efficient and effective inflation-adjusted returns, SIPs are certainly worth the risk of investing in mutual funds.

SIPs vs. EMIs: Which Is Better?

We aspire to live life to the fullest – have a ball of a time.

Living your dreams, doing what you love and are passionate about, encourages you to travel and live in the present, because you only live once (YOLO) and you avail a holiday loan.

But think, can a holiday loan (which carries an EMI or Equated Monthly Instalment) allow you to comfortably plan for the vital financial goals of life?

EMIs can damage your financial health if they exceed 40-50% of your regular monthly income. Hence, it is important to bite only as much you chew – to simply put, live within means before you get into a situation of debt-overhang. Also, when you use credit card to shop, make sure you're thoughtful enough and not adding to your debt obligations.

Here's stark difference between SIP and an EMI…

-

Through an EMI you can satiate many of your gratification, while if you commit a certain amount to SIPs, it can be in the interest of your long-term financial wellbeing and help you accomplish your long-term financial goals.

-

EMIs burn hard-earned money unless you've availed a loan to buy a house. But here too, it is vital to ensure that the deal doesn't make you house poor. Meaning, you aren't buying a swanky house when you don't need it and where the EMI plus the maintenance can be crushing. A commitment towards an SIP on the other hand, facilitates you to systematically compound wealth; build a corpus for your financial goals.

-

Too many EMIs can wreck your financial health as it induces an impulsive buying behaviour on credit. While more number of SIPs in a variety of mutual fund scheme that best suit your needs; investment objectives, instils discipline for your financial health.

So, please note that delayed gratification can be good for financial health in the long run. Through SIPs you accomplish many of your wants and frills.

Daily SIP vs. Monthly SIP: Which One To Choose?

Exercising everyday vs exercising once a month can make a huge difference to your health.

So when it comes to creating wealth, what would be advantageous?

Investing daily or investing monthly?

Some mutual fund houses seem to think investing daily works better.

While investment in mutual funds through Systematic Investment Plans (SIPs) with a monthly frequency was the norm, fund houses even offer a daily and quarterly frequency under SIPs.Which is the best SIP frequency?

Last month, the LIC Mutual Fund offered investors the option to invest in mutual funds through Daily SIP with as low as Rs 300 per day. This facility is available in five equity schemes viz. LIC MF Equity Fund, LIC MF Growth Fund, LIC MF Midcap Fund, LIC MF Infrastructure Fund, LIC MF Index Fund and two hybrid schemes viz. LIC MF Balanced Fund and LIC MF Monthly Income Plan.

“Through Daily SIP, the fund house is trying to promote the habit of investing daily and the aim is to create wealth through investing daily with a minimum sum of Rs 300 across 22 working days, which will lead to a monthly investment of Rs 6,600,” the fund house explained.

But do Daily SIPs truly benefit investors or even help negotiate volatility better than Monthly SIPs in mutual funds?

According to LIC Mutual Fund, “Daily SIP will further help in beating the market volatility and benefit our investors from rupee cost averaging.”

Logically, investing daily will certainly help in averaging your investment cost better, as you will be making many more transactions over the period. But, will it result in a significant difference in returns over the long term? At the end of the day, that is what matters.

PersonalFN crunches the numbers to find out…

Daily SIPs vs Monthly SIPs

Over the five-year period starting from March 1, 2013, PersonalFN compares the Daily SIP returns with the Monthly SIP returns of 147 equity-oriented schemes

There were as many as 1,225 daily instalments of Rs 300 each under the Daily SIP section in mutual fund schemes, leading to a total investment of Rs 3.68 lakh approximately.

To make a like-to-like comparison, Rs 6,126 was the instalment for the Monthly SIP spanning 60 months. The investment was made on the 1st of every month. This resulted in a total investment of Rs 3.68 lakh.

Now the results…

On an average, Monthly SIPs generated a value of approximately Rs 2,516 over Daily SIPs. In percentage terms, this works out to an outperformance of just 0.41%.

Under the Daily SIPs and Monthly SIPs, the portfolio value worked out to Rs 5.86 lakh and Rs 5.88 lakh approximately. The average XIRR generated was 18.8% and 18.7% respectively

Daily SIPs did marginally better in terms of XIRR. This is mainly because the monthly investment, made at the beginning of the month, was distributed across the month.

Below is the list of schemes where the difference was the highest between the Monthly SIP returns and Daily SIP returns.

Top 25 Mutual Fund Schemes Where Monthly SIP Was Better

| Scheme Name |

Portfolio Value* -

Monthly SIP (A) (In Rs) |

Portfolio Value* -

Daily SIP (B) (In Rs) |

Difference

in Value (A-B) |

Difference

in Percentage |

| SBI Small & Midcap Fund |

919,653 |

909,929 |

9,724 |

1.07% |

| Reliance Small Cap Fund |

870,058 |

861,098 |

8,960 |

1.04% |

| DSPBR Micro-Cap Fund |

792,909 |

785,183 |

7,726 |

0.98% |

| LIC MF Equity Fund |

471,492 |

466,956 |

4,536 |

0.97% |

| LIC MF Growth Fund |

500,596 |

495,956 |

4,641 |

0.94% |

| Sundaram S.M.I.L.E Fund |

723,072 |

716,795 |

6,277 |

0.88% |

| Franklin India Smaller Cos Fund |

722,486 |

716,215 |

6,270 |

0.88% |

| Mirae Asset Emerging Bluechip |

754,121 |

747,590 |

6,531 |

0.87% |

| Edelweiss Mid and Small Cap Fund |

705,566 |

700,408 |

5,158 |

0.74% |

| Reliance Mid & Small Cap Fund |

658,512 |

653,756 |

4,756 |

0.73% |

| Canara Robeco Emerging Equities Fund |

748,320 |

742,926 |

5,394 |

0.73% |

| L&T Midcap Fund |

743,379 |

738,042 |

5,338 |

0.72% |

| Aditya Birla SL Small & Midcap Fund |

734,492 |

729,315 |

5,177 |

0.71% |

| Kotak Emerging Equity Scheme |

700,006 |

695,147 |

4,859 |

0.70% |

| Franklin India Prima Fund |

659,898 |

655,512 |

4,386 |

0.67% |

| Aditya Birla SL Pure Value Fund |

750,283 |

745,297 |

4,986 |

0.67% |

| HDFC Mid-Cap Opportunities Fund |

673,698 |

669,256 |

4,441 |

0.66% |

| Sundaram Select Midcap |

681,469 |

677,046 |

4,423 |

0.65% |

| ICICI Prudential Midcap Fund |

676,695 |

672,357 |

4,338 |

0.65% |

| L&T India Value Fund |

685,702 |

681,387 |

4,315 |

0.63% |

| HSBC Midcap Equity Fund |

735,751 |

731,185 |

4,567 |

0.62% |

| Tata Mid Cap Growth Fund |

637,947 |

634,037 |

3,910 |

0.62% |

| BNP Paribas Mid Cap Fund |

628,149 |

624,373 |

3,777 |

0.60% |

| Aditya Birla SL India Opportunities Fund |

649,024 |

645,177 |

3,847 |

0.60% |

| Franklin India High Growth Cos Fund |

609,821 |

606,240 |

3,580 |

0.59% |

*Portfolio value as on February 26, 2018 | SIPs starting March 1, 2013

(Source: ACE MF, PersonalFN Research)

*Please note, this table only represents the funds based solely on past returns and is NOT a recommendation. Mutual Fund investments are subject to market risks. Read all scheme related documents carefully. Past performance is not an indicator for future returns.

Below is the list of schemes where the difference was the lowest between the Monthly SIP returns and Daily SIP returns.

Mutual Fund Schemes Where Daily SIPs Were Better

*Portfolio value as on February 26, 2018 | SIPs starting March 1, 2013

(Source: ACE MF, PersonalFN Research)

In the tables above, high volatility schemes where exposure to small-caps and mid-caps has been the highest resulted in a bigger difference between the Monthly SIPs and Daily SIPs.

If Daily SIPs help in beating the market volatility, why weren't the returns higher?

Well, Daily SIPs do help in averaging out costs better, but this does not necessarily mean that the average cost of investment through Daily SIPs will be lower than Monthly SIPs.

Take for example, at the beginning of the month, the NAV of a scheme is Rs 100. For the Monthly SIP, this is the cost price. If we assume that over the month, the NAV of the scheme gradually rises to Rs 110, the average cost under Daily SIP will naturally be higher than that of the Monthly SIP investment.

However, if the NAV was headed lower, Daily SIPs would have scored better. Hence, the difference in returns is primarily a factor of how the market behaves over this period. But, over the long term, the variation will be insignificant.

During a period where the market was continuously hitting all-time highs, investments through Daily SIPs were gradually made at higher prices, hence the returns suffered marginally.

Thus, if you invest with the expectations that the market will move higher over the long term, Monthly SIPs should be an apt choice.

If you wish to calculate the future value of your Monthly SIPs, use PersonalFN's SIP Calculator.

3 reasons why you should opt for Monthly SIPs over Daily SIPs

As seen in the analysis above, in terms of returns, there is hardly much difference between a Monthly SIP and Daily SIP. The quantum variance in returns will change over different market cycles. Hence, you need to choose an option that is simple and convenient. Here's is where Monthly SIPs score over Daily SIPs.

-

Convenience – Over a five-year period, there will be over 1,200 Daily SIP transactions. This compares to just 60 transactions through a Monthly SIP. Imagine viewing your bank statement with daily entries on entries because of mutual fund investments through a Daily SIP. If you invest in multiple schemes through Daily SIPs, the number of entries multiply.

You certainly do not want important bank transactions to get lost in sea of SIP entries. The same goes for your mutual fund transaction statement. Imagine the inconvenience of reading through the statements in order to identify non-SIP transactions.

-

Better tracking – With a reduced number of entries under Monthly SIP, you will be able to track your investments better. Imagine comparing your bank statement to your mutual fund statement to check if all transactions were successful. This would be easier to track if you invested through the Monthly SIP route. Also, when it comes to calculating the returns, you would be able to do it faster with investment through a Monthly SIP.

-

Ability to plan better – If you are salaried, you get a monthly salary credit. Thus, you can smoothly plan what proportion of your salary can be invested every month. And this can be effortlessly be converted into a mutual fund investment through a monthly SIP. Many opt for a Monthly SIP date that is a few days after their salary credit. Unplanned expenditures towards the end of the month may lead to a lower bank balance, hence, nobody wishes to take the risk of the SIP instalment getting returned. This can get a little tricky with a Daily SIP. Hence, with a Monthly SIP, you should be able to plan your finances better.

In times of volatility, a SIP would undoubtedly be a prudent route as compared to investing your corpus as a lumpsum. As seen in our analysis above, a Monthly SIP will be a prudent choice.

When investing in equity, it is important to keep a long-term investment horizon of five to seven years or more, even if you are investing via a SIP. The returns may be a few percentage points lower as compared to a lumpsum investment, but it will still be sufficient to meet your financial goals.

It is important to note that there are several benefits of investing via a SIP as a regular form of investment.

The top three reasons why you should invest in mutual funds through SIPs:

-

A hassle-free investment route

-

Deals with market volatility

-

Devoid of behavioural biases

Clearly, SIP-ping into mutual funds, with all these benefits and much more, will help achieve your financial goals.

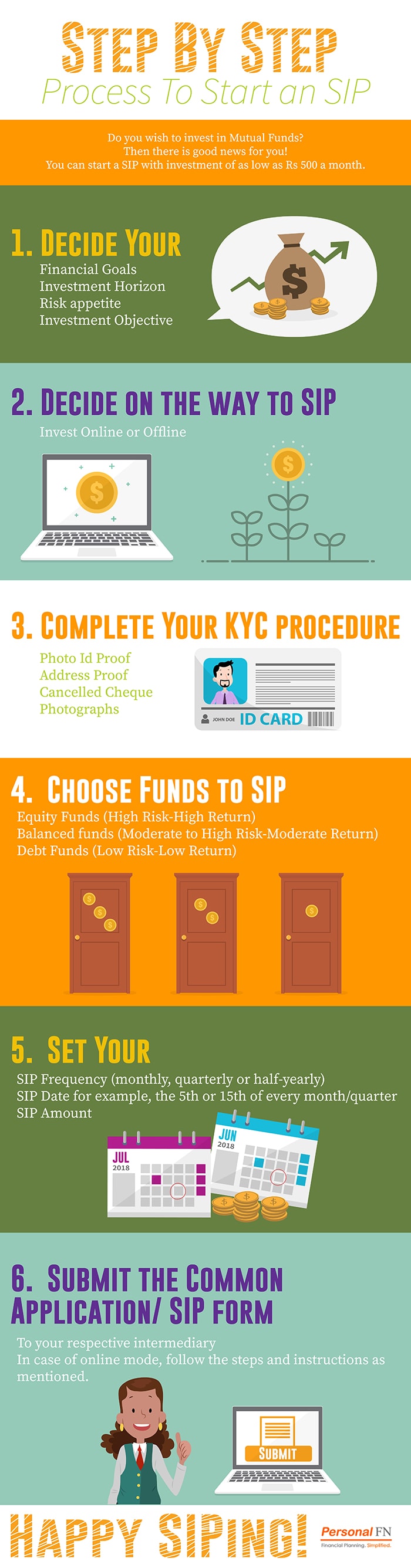

Finally, how to start a SIPs?

Well, you have broadly two ways: offline and online.

In case of the former, approach the office a mutual fund house / mutual fund distributor / agent / relationship manager / investment adviser. For prudent handholding, seek services of a Certified Financial Guardian who is a mark of trust and respect. They can help you construct a robust investment portfolio based on your financial goals.

Here’s what you need to do to start a SIP offline:

-

Select a mutual fund scheme that best suits your needs, investment objectives, financial goals

-

Fill in the Common Application Form / SIP form carefully and completely mentioning the name of the scheme and other details

-

Provide your NACH mandate form mentioning all you SIP details

-

If the KYC is not done, fill in the KYC form and comply with it

-

Hand over the forms (as mentioned above) to the office of mutual fund distributor / agent / relationship manager / investment adviser / Certified Financial Guardian, or you can even directly submit to Registrar and Transfer Agents (RTAs) / AMC.

In case if you choose to SIP online, you can log on to respective mutual fund house’s website, or use other transaction platforms viz. MFU, or opt for services of robo-advisory platforms and follow the steps and instructions mentioned.

But when buying into mutual funds, ensure that you are opting for only ‘direct plans’ owing to the benefit we explained earlier.

Go ahead and take SIPs today!

Happy investing!

© Quantum Information Services Pvt. Ltd. All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021.. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667

SEBI-registered Investment Adviser. Registration No. INA000000680, SEBI (Investment Advisers) Regulation, 2013

Add Comments

| Comments |

Irsh_2009@yahoo.co.in

Apr 07, 2018

I would like to know about SIP to invest. |

deven@personalfn.com

Dec 04, 2017

good information |

padiahemang@gmail.com

Feb 26, 2018

good information about sip at https://goo.gl/758oF2

this app to good and user friendly and also year wise and month wise download pdf and excel sheet.https://goo.gl/758oF2 |

mvrakesh79992@gmail.com

Jan 02, 2018

Actually I have no idea about sip ..bt when I read this...I fully satisfied about sip |

mvrakesh79992@gmail.com

Jan 02, 2018

Actually I have no idea about sip ..bt when I read this...I fully satisfied about sip |

1