Does Your Liquid Fund Follow the Principle of Safety? Know Here…

Divya Grover

Jan 07, 2022

Listen to Does Your Liquid Fund Follow the Principle of Safety? Know Here…

00:00

00:00

Liquid funds are perceived to be the safest in the debt mutual funds category. These funds invest in debt and money market instruments with a maturity of up to 91 days. The primary objective of a Liquid Fund is to provide optimal returns with a low level of risk and high liquidity through judicious investments in money market and debt instruments. Returns are secondary when you invest in Liquid Funds. As a result, Liquid Funds are a low risk - low return investment avenue.

However, in the past there have been instances where some Liquid Funds swayed from the guiding principle of the product and invested in riskier instruments. If you recall, in late 2018, when the IL&FS crisis broke out, several liquid funds took a hit in the range of 0.5% to 8% as the funds had to mark down instruments issued by the company along with its group companies owing to sudden rating downgrades.

Since investors generally hold Liquid funds for their short term investment needs, a significant write-off of a particular asset in the portfolio would mean that investors would have to hold on to the fund longer than expected to recover from the losses. Thus, it is important to stay away from Liquid funds that take higher credit risk and prefer only pure Liquid Funds that strictly prioritise safety over returns.

(Image source: www.freepik.com - photo created by ijeab)

Is your Liquid Fund safe?

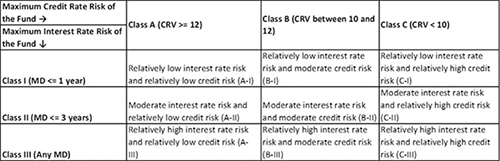

SEBI had recently introduced the Potential Risk Class (PRC) matrix for classification of debt mutual fund schemes based on interest rate risk and credit risk. Asset Management Companies (AMCs) have the option to select any of the 9 combinations (see Table below) to highlight the interest rate and credit risk attributes of the schemes. A scheme classified in the A-I cell carries the least risk potential while those classified under the C-III carries the highest risk potential. However, once the classification is done, the subsequent changes would be treated as the changes in the fundamental attributes of the scheme.

Table: Risk Class Matrix for Debt Mutual Funds

(Source: SEBI)

Despite the fact that Liquids are expected to carry the least risk at all times, and should be ideally placed in the A-I cell, several fund houses have placed these schemes in the moderate risk category in the PRC matrix. As you can see in the table below, popular and large-sized Liquid Funds such as SBI Liquid Fund, HDFC Liquid Fund, ICICI Pru Liquid Fund, Kotak Liquid Fund, and Nippon India Liquid Fund, among many others are placed in the moderate credit risk category (B-I cell) of the PRC Matrix. This signifies that the fund manager of these schemes may take slightly higher credit risk to generate extra returns by investing in moderately risky securities.

Very few Liquid Funds such as, Parag Parikh Liquid Fund, Quantum Liquid Fund, and JM Liquid Fund are placed in the A-I cell. Meaning, these funds will avoid taking excessive credit or interest rate risk, thus providing safety and liquidity to investors at all times.

Table: How are Liquid Funds placed in the PRC matrix?

The above list is not exhaustive

(Source: PersonalFN Research)

The special care to take when you select Liquid Funds for your portfolio

A Liquid fund is supposed to be an alternative to parking money in a savings bank account for various purposes like contingency planning, addressing short-term goals, etc. That's the reason its primary objective is to keep the investors' hard-earned money safe and offer high liquidity. You would be better off sticking to a pure Liquid Fund where the fund manager doesn't chase returns by taking higher credit risk.

It is important to note that PRC matrix does not denote the current risk the portfolio is exposed to but the maximum interest rate risk and credit risk that a debt fund is willing to take. The actual risk that the fund manager is taking is captured by the 'Risk-o-meter'. The Risk-o-meter can change on a monthly basis based on the scheme's portfolio.

If the Liquid Fund that you have invested in undertakes higher risk (based on its Risk-o-meter and classification in PRC matrix), consider switching to relatively safer schemes in the category.

Ideally, you should avoid investing in liquid funds that have higher allocation to moderate-rated instruments or those investing predominantly in instruments issued by Private issuers. If your preference is safety over returns, you should consider Liquid funds that primarily focus on investing in Government and Quasi-government securities.

[Read: What Should be Your Debt Mutual Fund Strategy in 2022 Amid Expectation of Interest Rate Hike by RBI?]

Additionally, ensure that the scheme's portfolio is well diversified across a range of securities and that it is not concentrated towards a certain company or group of companies.

Most importantly, always give higher importance to fund houses that follow sound risk management techniques and have robust investment systems and processes in place. It is crucial that you understand the overall philosophy of the fund house; whether they aim to create wealth for investors, or are they in a race to garner more AUM by showcasing higher returns generated by chasing higher yields and taking higher risk.

PS: If you are looking for quality mutual fund schemes (including Equity-linked Saving Schemes) to add to your investment portfolio, I suggest you subscribe to PersonalFN's premium research service, FundSelect. PersonalFN's FundSelect service provides insightful and practical guidance on which mutual fund schemes to Buy, Hold, and Sell.

Currently, with the subscription to FundSelect, you could also get Free Bonus access to PersonalFN's Debt Fund recommendation service DebtSelect.

If you are serious about investing in a rewarding mutual fund scheme, subscribe now!

Warm Regards,

Divya Grover

Research Analyst

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds