How Will the ‘T+1 Rolling Settlement’ Impact Equity Market and Mutual Funds

Listen to How Will the ‘T+1 Rolling Settlement’ Impact Equity Market and Mutual Funds

00:00

00:00

We are in a world where fintech and e-commerce have significantly influenced our way of living. The capital markets too, have been riding on the wave of digitization nearly for the past 18 months. Those who earlier preferred the physical mode of investing are now, gradually becoming more accustomed to investing online.

Investing in equities online is on the way to be more quick and liquid from January 1, 2022. After receiving a request from various stakeholders, the Securities and Exchange Board of India (SEBI) last week (on September 07, 2021), introduced a circular to move to 'T+1 Rolling Settlement' from the current 'T+2 Rolling Settlement' cycle that was introduced way back in April 2003.

Under the 'T+1 Rolling Settlement' cycle transaction, when you as an investor sell securities, the money gets credited to your bank account (pay-in) within one day from the date of transaction, and similarly, when you buy, you receive the securities within a day from the date of transaction post the funds pay-out.

The new 'T+1 Rolling Settlement' cycle will be optional, at least to begin with, plus will offer the stock exchanges the flexibility to determine the settlement cycle for individual stocks.

However, this cannot be done randomly. The capital market regulator has laid down a standard procedure to follow.

If stock exchanges decide to change the settlement cycle from 'T+2' to 'T+1' for particular scrip, they will have to give a notice of such changes one month in advance. Once implemented, the T+1 cycle can't be altered for at least 6 months. If exchanges want to switch back to the 'T+2 Rolling Settlement' cycle thereafter, they will have to give one month's notice again. This process will repeat as many times as the exchanges switch the settlement cycle.

Once the stock exchanges select a cycle, no further distinction can be made based on the type of deals-regular deals and block deals etc.

Currently, under the 'T+2 Rolling Settlement' cycle, the custodian confirmation and delivery generation happen on a 'T+1' basis. And other functions such as pay-in, pay-out, debit valuation and auction are completed by the second working day, excluding the day of trade i.e. 'T+3'.

(Image source: freepik.com; photo created by rawpixel.com)

(Image source: freepik.com; photo created by rawpixel.com)

With the introduction of this, 'T+1 Rolling Settlement' cycle, India has certainly come a long way from following a fortnightly settlement cycle in the early 90s. At present, China is the only other major country that follows the 'T+0'/ 'T+1' settlement cycle.

Once the 'T+1 Rolling Settlement' cycle is adopted, the post-settlement cycle constituting functions such as auction settlement, bad delivery reporting, pay-ins and pay-outs associated with bad delivery amongst others would also be shortened. The regulator has directed stock exchanges, clearing corporations, and depositories to take necessary steps to put in place proper systems and procedures for a smooth introduction of the 'T+1 Rolling Settlement' cycle on an optional basis, including necessary amendments to the relevant bye-laws, rules and regulations.

What are the potential positives of the shortening of the settlement cycle?

The migration to the 'T+1 Rolling Settlement' cycle (from 'T+2') is likely to enhance the liquidity, turnover, and perhaps stimulate the animal spirits in the Indian equity markets.

It is a big positive for domestic investors (retail, High Net-worth Individuals, and Domestic Institutional Investors) since it would improve market efficiency and may lower margin requirements. Longer settlement cycles often give rise to a higher counterparty risk which becomes quite relevant during extreme market conditions. Higher counterparty risks often call for higher margins. Thus, moving towards the 'T+1 Rolling Settlement' cycle will free up capital for further trading/investing which otherwise will be required to be parked as margins.

Potentially greater volume and enhanced liquidity backed by pronounced domestic participation would bode well for the momentum of shares of companies and, in consequence, the underlying portfolio of equity mutual funds benefiting the investors at large.

However, there are challenges, including for mutual funds...

For Foreign Portfolio Investors (FPI), due to the time zones differences, the new 'T+1 Rolling Settlement' cycle may be difficult to follow. This is one of the key reasons why most other equity markets in the developed and developing economies are still following the 'T+2 Rolling Settlement' cycle.

The introduction of the new 'T+1 Rolling Settlement' cycle that comes into effect from January 1, 2022, although on an optional basis, is currently drawing a lot of negative feedback from the institutional investors.

As you might be aware, the decision to buy/sell and its execution goes through various levels of coordination between the fund managers, back-office staff, brokerage houses and custodians to name a few. Thus, the implementation of the 'T+1 Rolling Settlement' cycle is likely to put an additional cost burden on the institutional investors, including mutual funds. To make up for the cost, certain schemes may raise their expense ratio.

Employees of banks and brokerage houses may have to work long hours each trading day to facilitate the 'T+1 Rolling Settlement' cycle. Currently, a fact is that not all cheques drawn pan-India are settled on the same day.

Moreover, investors who don't hold their trading and demat accounts with one entity will face trouble in issuing delivery instruction slips for the transfer of shares.

Transactions in the Securities Lending and Borrowing (SLB) might also reflect the negative impact of the shortening of the settlement cycle.

The Association of National Exchanges Members of India (ANMI) has insisted that the 'T+1 Rolling Settlement' cycle should be introduced only after addressing the operational and technical challenges involved in it.

So, although shortening the settlement cycle appears to be a positive development, there are numerous operational challenges.

To sum-up...

Such capital market reforms, of course, help improve overall financial market efficiency and participation. But it also calls for added investment to make for the operational challenges.

As the market penetration improves and more retail investors start planning their long term goals with equities as an asset class; the market turnover, liquidity and momentum will improve further with the 'T+1 Rolling Settlement' cycle and retain the vivacious market sentiments.

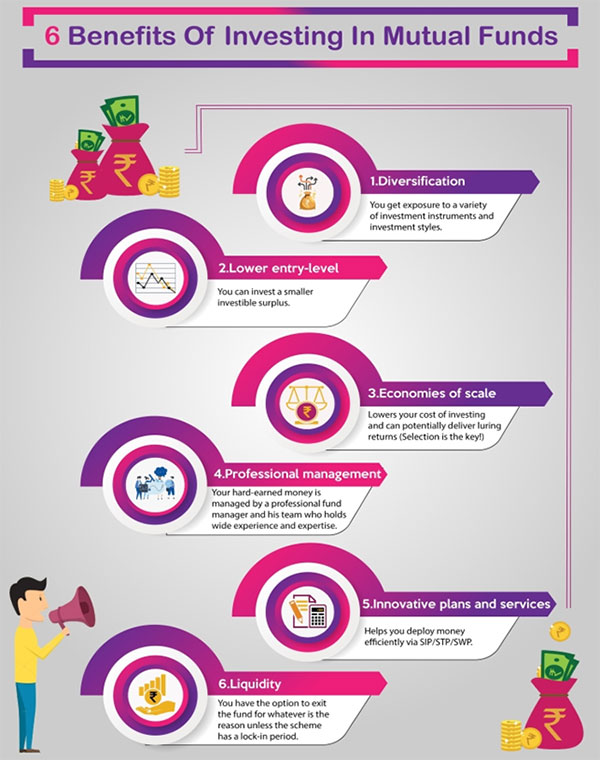

Equity is a promising asset class to generate wealth and counter inflation over the long run. Further therein, the equity-oriented mutual funds are a promising avenue, given the six benefits highlighted in the infographic below.

But given that the markets have scaled up--more than doubled since March 23, 2020, low--and volatility would intensify in the near future; you must devise a sensible strategy and take exposure to only worthy diversified equity funds.

Taking the Systematic Investment Plan (SIP) would be prudent. This will help you to mitigate the risk better and sensibly negotiate market volatility. If the market corrects from the current level -- which is possible -- the inherent rupee-cost averaging feature would help mitigate the risk involved while you endeavour to compound your hard-earned money. More units would be allotted against your SIP instalments in a corrective phase, and when the market begins to ascend again, it would compound your wealth.

But make sure you select the best mutual fund schemes for your SIP investments. When you choose a scheme for SIP, ensure that you pick worthy schemes that align with your financial goals, risk appetite and investment horizon. While equity investments have the potential to generate high returns, don't ignore the risk involved, and select funds that are most suited for you as per the asset allocation meant for you.

Your equity SIP portfolio should contain a good mix of a Large-cap Fund, a Large & Mid-cap Fund, a Multi-cap/Flexi-cap Fund, a Mid-cap Fund, and a Value Fund for optimum diversification. You may also invest in small-cap funds if your risk appetite permits it.

Some of the best performing mutual fund schemes to SIP into based on PersonalFN's research and analysis are:

These schemes have delivered superior risk-adjusted returns across various market phases and cycles and have fared well on qualitative parameters as well. That said, do keep in mind that past performance is not indicative of future returns.

[Read: Best Mutual Funds for SIP in 2021]

If you are looking for quality mutual fund schemes to add to your investment portfolio, subscribe to PersonalFN's premium research service, FundSelect.

At PersonalFN we follow a S.M.A.R.T Score Matrix, wherein we evaluate:

-

S - Systems and Processes

-

M - Market Cycle Performance

-

A - Asset Management Style

-

R - Risk-Reward Ratios

-

T - Performance Track Record

The stringent process has helped our valued mutual fund research subscribers to own some of the best mutual fund schemes in the investment portfolio with a commendable long-term performance track record.

With FundSelect, you will get insightful guidance and recommendations on some worthy funds having high growth potential in the years to come.

We will also help you choose some of the best Equity Linked Saving Schemes (ELSS) for your tax-saving with PersonalFN's premium research service, FundSelect.

Backed by our compressive research, we will tell you which mutual fund schemes you should you Buy, Hold, and Sell.

If you are serious about investing in a rewarding mutual fund scheme, Subscribe now!

Happy Investing!

Warm Regards,

Rounaq Neroy

Editor, Daily Wealth Letter

Join Now: PersonalFN is now on Telegram. Join FREE Today to get ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds