Your Guide To ELSS

Last week my best-friend Pritha called me for some mutual fund investing tips. Her goal was tax saving with ELSS mutual funds. She being an Artist is an Alien in mutual funds space. She only knew the permissible limit under Section 80C of Income Tax Act is Rs 1.5 lakh. And realised she too must invest in mutual funds. She heard stories of her colleagues who invested in ELSS last year and the stellar returns earned. Moreover, she also had to submit all her investment declaration proof to the HR department of the company where she works.

Are you too intending to invest in ELSS funds?

Planning to make last minute tax saving investments in ELSS?

Then, you must read this Guide on ELSS before you start your space craft and head towards the unknown world of Tax.

Because it is better to know where you are heading before you start.

Here is the outline to this guide:

Chapter #1: Learn Basics Of ELSS

Simply put, ELSS is a type of diversified equity mutual fund, which qualifies for tax exemption under Section 80C of the Income Tax Act.

ELSS stands for Equity Linked Savings Scheme. It works like any other open-ended equity fund that invests predominantly in the stock market to generate growth by way of capital appreciation (dividends) for investors.

A distinguishing feature about ELSS is that they are subject to a compulsory lock-in period of 3 years, but the minimum application amount in most of them is as little as Rs 500, with no upper limit. In ELSS, you can make either lump sum investments or investments through a Systematic Investment Plan (SIP). In case of the latter, each instalment has a 3-year lock-in period.

And if you ask, who can invest in ELSS? Individuals and HUFs can invest in ELSS. It is noteworthy that, in the long-term if you intend to create wealth, then this tax saving funds has potential to give you luring inflation-adjusted returns.

You may say – “but there is risk involved”. Well, no doubt about that; but in order to even out the shocks of volatility in the equity markets you can adopt the SIP route of investing here which will provide you the advantage of “compounding” along with “rupee-cost averaging”.

SIPs in ELSS can help you tackle volatility and may help you gradually create wealth in the long run.

While considering an ELSS mutual fund for your market-linked tax-saving portfolio, give importance to those ELSS mutual funds that have completed at least 3 years of track record and select schemes from mutual fund houses which follow strong investment systems and processes.

Don’t get lured just by returns clocked because there’s more to evaluating a mutual fund scheme than just returns. Moreover, past performance does not guarantee that the fund will continue to fare in the same manner in the future. Hence look for a fund with a consistent performance track record besides qualitative aspect like fund house pedigree, investment process, quality of fund management team, among others.

Chapter #2: Why Everyone Is Gung-ho About ELSS Funds

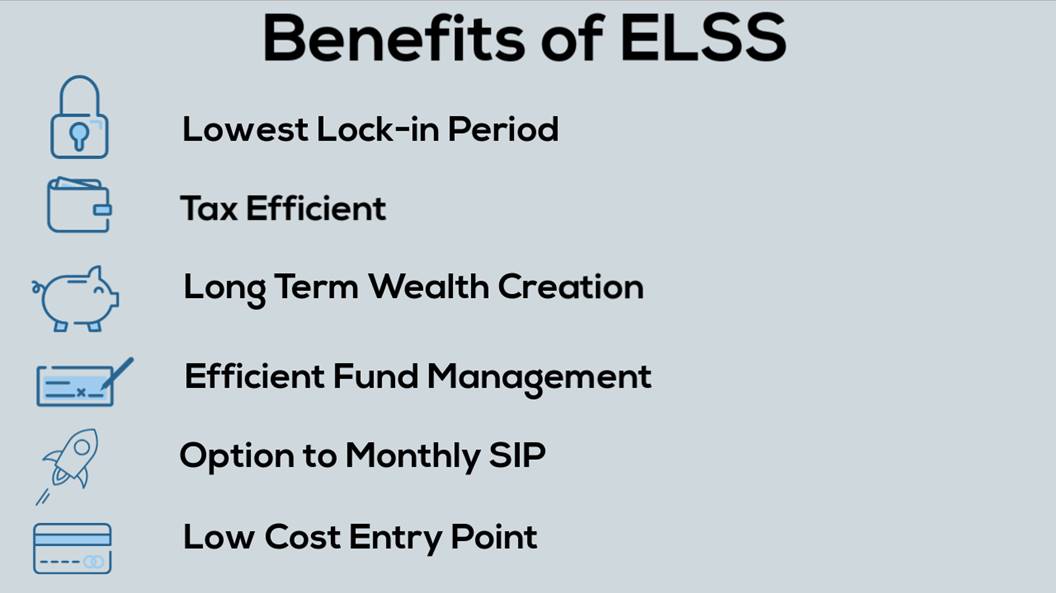

For those who still want to know more why they should invest in ELSS Mutual Funds, here is a list of merits you cannot ignore.

-

Lowest Lock-in Period

This is what makes ELSS better than all other investment options.

While your tax saving investments in PPF is locked in for 15 years, NSC for 6 years and tax saving bank fixed deposits for 5 years, your investments in ELSS is locked in for just 3 years. So, if you are looking for tax benefits along with higher return potential, but do not want to commit your money for very long period of 5 to 15 years, ELSS is something you should look for.

-

Tax Efficient

When compared with any other diversified equity mutual fund, the taxation on the gains are the same.

So, what makes ELSS differ from any other diversified mutual fund? You can invest up to Rs 1.5 lakh in an ELSS and get that as a tax deduction under Section 80C in a financial year.

Mind you, you cannot get that from any equity mutual fund.

And when compared to other popular tax saving instruments such as Tax Saving Fixed Deposits or PPF, ELSS is definitely better.

Not only does an ELSS reap higher returns, long-term gains from an ELSS is absolutely tax free just like that of PPF.

But what about Tax Saving Fixed Deposits? My elders always saved tax there?

Well, the answer is you can also park your money in FDs, but you may earn lesser returns on your investments. Plus, the returns earned on fixed deposits are taxable too.

-

Long Term Wealth Creation

Like other equity mutual fund schemes, these mutual funds too are optimized for highest returns possible.

You can depend on the best ELSS to potentially grow your money in a matter of 3 to 5 years (considering the market is favourable, of course).

-

Efficient Fund Management

Unlike in a term deposit or a NSC, where you put your money in, and the issuer just lends it out, while paying you a nominal return; a mutual fund is geared to grow your investment in a much more efficient way.

Why?

Because a mutual fund is expected to be managed by professional fund managers. They invest with an aim to make higher gains for their investors.

Agreed, investing in a mutual fund is risky per se. But if you invest in the RIGHT mutual fund, you would reap much higher gain than you can probably expect from a fixed deposit, PPF account or savings certificate.

And the reason behind it is, perhaps the long-term experience and market knowledge of the fund managers working to grow your money day in and day out.

In other words, if you are looking to grow your investment, in a shorter time compared to other tax-saving instruments and that also, not paying the government any share of it.

-

Option to Monthly SIP

The best approach to sail the tides of market volatility, is to opt for Systematic Investment Plans (SIPs), a mode investing in mutual fund schemes offered by mutual fund houses.

You need not wait till the last quarter of the year to make a lump-sum investment in ELSS.

-

Low Cost Entry Point

As mentioned above, you can invest in ELSS funds with investments as low as Rs 1000 via SIP route. Hence, you no longer can give an excuse that I cannot afford to invest in ELSS.

Unlike PPF contributions, there is no maximum limit on your investments in ELSS. However, tax benefits can be availed only for investments made upto Rs 1.5 lakh.

These benefits make it more desirable for investors looking to invest in ELSS with an objective of tax saving along with long term wealth creation.

Chapter #3: Comparison Of A Star Performer With Others in Tax Saving Class

Here is comparison between ELSS and other Tax Saving Instruments. Though each one has its own merits and demerits, you should invest in instruments as per your financial goals, age, risk appetite and needs. Do not invest blindly in an instrument which does help you to meet your crucial financial goals.

Comparison Between ELSS and Other Tax Saving Instruments

| Schemes |

Interest Rate |

Tenure |

Min – Max Investment |

Current Tax on returns |

| Equity Linked Savings Scheme (ELSS) |

Market-Linked Returns |

Term: Ongoing;

Lock-in-period: 3 years |

Varies from scheme to scheme. Can range from Rs 500 - No upper Limit |

Dividend & Long Term Capital Gains Tax is applicable |

| Unit Linked Insurance Plans (ULIPs) |

Market-Linked Returns |

Term: 10 - 20 years;

Lock-in-period: 5 years |

Premium varies from scheme to scheme |

Capital gains post lock-in are tax free

+

maturity amount would be tax-free (exempt) as per Section 10(10D) |

| National Pension System (NPS) |

Market-Linked Returns |

30-35 years |

Rs 500 per month or Rs 6,000 per annum, no upper limit |

Capital gains taxed on withdrawal |

| Public Provident Fund |

7.6% p.a.#

(compounded annually) |

15 years^ |

Rs 500 - Rs 1. 5 lakh |

Interest income is tax free |

| Sukanya Samriddhi Scheme |

8.1% p.a. (compounded annually) |

21 years |

Rs 1,000 - Rs 1. 5 lakh |

Interest income is tax free |

| National Savings Certificate |

7.6% for 5 yr deposit#

(compounded annually) |

5 years |

Rs 100 - No upper Limit |

Interest accrued

is taxed every

year as per one's income-tax slab |

| Bank Deposits |

6.00% - 7.50% |

5 years |

No upper Limit |

| Post Office Time Deposit |

7.6% for 5-Yr deposit (compounded quarterly & paid annually) |

5 years |

Rs 200 - No upper Limit |

| Senior Citizens Savings Schemes |

8.3% p.a. (compounded quarterly payable quarterly) |

5 years |

Rs 1,000 - Rs 15 lakh |

| Non-ULIP Insurance Plans |

Sum Assured Only

(i.e. Insurance Cover) |

5-40 years |

Premium depends upon the insurance cover |

Redemption amount is tax free |

* Partial withdrawals allowed subject to conditions; ^can be extended in tranches of 5 years; #Interest rates would be re-set every quarter.

Now you have many tax saving instruments and each one is advantageous over the other. But you need to select the instruments as per your needs.

For instance, ELSS vs PPF – what would you prefer?

Here is a short comparison between the two:

| Particulars |

ELSS |

PPF |

| Returns |

15% to 18% |

7% to 8% |

| Lock-in |

3 years |

15 years |

| Min-Max Invest. Amount |

Rs 1000 - No upper limit |

Rs 500 - Rs 1.5 lakh |

| Tax Benefits |

Dividend & Long Term Capital Gains Tax is applicable |

Exempt-Exempt-Exempt |

(Interesting Read: LTCG Tax Breaks The Spine Of Bulls. Will Bears Have A Last Laugh?)

Well, a lot of factors need to be considered over here.

ELSS is a market linked security and returns on your ELSS funds depend on the performance of stock market at large and other fund specific characteristics.

PPF on the other hand is a Government backed, long-term small savings scheme. For years PPF has been most favourite instruments by Indian Citizens.

But keep in mind your liquidity needs, because under PPF account your money is blocked for good 15 years.

So, if you are keen on a safe corpus, earning a decent tax-free rate of return, enjoying tax benefit; then PPF is for you. The contributions (i.e. investments) made to the PPF account, will earn a tax-free interest and the maturity proceeds are exempt from income-tax. Further, the contributions made into PPF account are yours for keeping – it cannot be attached by the order of a court to any debt or liability you may have.

(Infographic: Your Tax Savings Investment Picks for 2018)

Now that you know so much about ELSS, I am sure you want to take next step and learn about – How to Invest in ELSS

Chapter #4: Steps To Start Your Spaceship

As a newbie, you may be wondering about how and which ELSS mutual fund schemes to invest in.

With innovations in technology and investor-focused regulations, you can invest in ELSS mutual fund schemes in multiple ways. And, before we explore the different avenues you can choose from, let’s understand that mutual funds offer two different plans for every scheme:

- A regular plan, for investors investing through a distributor, and

- A direct plan, for investors coming directly to the AMC or through an Investment Adviser

The plans differ from each other only in terms of cost. The regular plan charges a higher expense ratio, as compensation to the distributor. The direct plan, is devoid of this additional cost, hence, investors benefit with higher returns.

If you prefer simplicity and the process of investing sounds incomprehensible, opt for a mutual fund distributor. They will take care all administration, paperwork activity such as form filing, etc. All you need to do is submit relevant documentation and sign on the dotted line to begin your investment journey in mutual funds.

Just remember, “caveat emptor”... Buyer Beware.

Yes, there are several cases where distributors have mis-sold mutual fund investments. So, you need to read the fine print carefully before you sign anything.

When it comes to a direct plan, if you are tech-savvy and have basic financial knowledge, investing in mutual funds though this route will be a much better option. Alternatively, you can seek guidance from a fee-based mutual fund investment adviser about the right mutual fund schemes for your financial goals.

Investing in direct mutual fund plans is a much better option as you can save a significant amount of money over the long term.

But before you embark on the journey of investing with ELSS funds in mutual funds, you need to complete your KYC (Know Your Customer) formalities. KYC is a prerequisite for investing in mutual funds (and almost all financial instruments). It is vital compliance on the part of financial product manufacturers, to know their investor better.

Investing in ELSS Fund – Regular Plan

If you are

investing in mutual funds through a distributor such as a bank or investment broker, they will assist you with the transaction forms and other required documentation. Some big distributors may offer online investment facilities to add to the convenience, while local distributors may offer purely offline services. The advice and service might be more personalised in the latter. Some may charge an additional fee for services offered, in addition to the commissions earned from your mutual fund investments.

If you would like to save on costs, you may opt for the direct route.

Investing in ELSS Fund – Direct Plan

If you decide to invest in mutual funds directly, here are the different paths:

-

AMC or Registrar office

Once you have decided in which fund to invest, you can visit the nearest AMC office or the office of their registrar (CAMS or Karvy) to invest in the mutual fund.

You can check the list of AMC offices on AMFI website.

If you prefer the online route, you may invest in mutual fund schemes directly through the online portal of the fund house. However, if you have multiple funds, you will need to register and invest in each fund house individually. This can be inconvenient if you have a number of schemes from different fund houses.

The registrars also facilitate online investing in mutual funds, however, the investment will be limited to the mutual funds enrolled with them.

-

Mutual Fund Utilities

Mutual Fund Utilities is a shared platform of different fund houses. You need to create an account first, before transacting. We explain how you can create a Common Account Number (CAN) later in the article. You can transact in mutual funds of almost all the AMCs. Through a single transaction form, you can invest in multiple funds of different fund houses.

You can even invest in mutual funds though the online route. Once your CAN is created, you can invest in mutual fund schemes through the portal of MFU portal.

-

Investment Adviser

An investment adviser will guide through your investment journey and will bring ease in the process of investing.

If you hire the services of a fee-based investment adviser, you may send over your transaction documents to them to begin investing in mutual funds. Your investment adviser will also receive newsfeed from the fund house and they can keep track of your mutual fund investments.

-

Robo-Advisers

Robo-advisers on the other hand are digital advisers. They provide portfolio management and financial planning services online, without any human intervention. These types of advisers are usually more affordable than human advisers to all classes (of investors). The advantage with robo-advisers is zero human bias in the advice, but there could be few limitations to the way information is sought without human intervention.

A robo-adviser can offer you a world of convenience, thanks to the advancement in technology. Opt for a specialised robo-advisory service that will ensure your financial well-being through mutual funds—one that proves to be worth more than it costs. Opt for robo-advisers who are genuinely concerned about your long-term financial well-being. Be careful of not investing your hard-earned money through fly-by-night operators. Opt for robo-advisers backed by established companies in the financial services space. Check if sound and ethical research processes fully support their investment recommendations. They should be fee-based to ensure that the commissions they earn do not influence their advice.

Opt for a specialised robo-adviser who can ensure your financial well-being with prudent recommendations. With a 24x7-service window, robo-advisers are the future of financial planning and investments in a time-strapped world.

Before you begin your mutual funds journey calculate the returns on lump sum investments using our Mutual Funds Calculator and SIP Calculator for your monthly SIP instalments. This will help you make informed decision.

Chapter #5: Want To Take Baby Steps – Start SIP

Most investors wait till the eleventh hour. Many invest in ELSSs in the last quarter of the financial year, at one go. This results in sub-optimal tax planning.

Additionally, this is not the best way to make equity investments.

When you invest a lump sum––at one go–– in equity mutual funds, you might expose yourself to a high-volatility risk. Hence, even if you wish to invest lump sum, a staggered approach is prudent.

Like other mutual funds, you can opt for Systematic Investment Plan (SIP) to invest in ELSS fund as well.

SIP is a mode of investing in Mutual Funds in a staggered manner.

With this simple technique, you give yourself a chance to accumulate more units when markets go down, and as the Net Asset Value (NAV) falls. But start a SIP in an ELSS at the beginning of the financial year. This will facilitate better rupee-cost averaging while you endeavour to compound wealth over period of time.

Please note that each instalment in ELSS will be locked-in for a period of 3 years. In other words, if your first SIP payment was made on January 05, 2016 then lock-in period will end on January 05, 2019 for that instalment. Hence, it is a staggered manner investing.

Before you invest in tax saving mutual funds this year – avoid committing these 7 common mistakes

Chapter #6: Wish To Select Star Fund?

There is no dearth of choices in the ELSS mutual fund category. Hence, you need to analyse the fund performance minutely before investing. Remember, that under ELSS, the lock-in is three years. Thus, if you pick the wrong fund, you will have to bear the cost of underperformance for the entire period.

The performance of ELSS funds can vary wildly over the years. A top ELSS fund in one period may not necessarily be the best ELSS fund for the next period. Thus, you need to pick the right ELSS fund, one that has performed consistently and one that has generated a superior risk-adjusted performance.

Let us have a look at the three-year return of the top ELSS funds from three years ago (as on December 31, 2014). We will then compare these funds to the top performing ELSSs over three years, as on December 31, 2017.

Top Performing ELSS Funds as on February 2015

Data as on February 28, 2015

Returns are compounded

(Source ACE MF, PersonalFN Research)

Axis Long Term Equity Fund, Reliance Tax Saver (ELSS) Fund, Aditya Birla Sun Life Tax Relief '96, Aditya Birla Sun Life Tax Plan and Invesco India Tax Plan followed closely behind.

But among these five funds, just two— Principal Tax Savings Fund and Aditya Birla Sun Life Tax Relief’96 continued their top ranking performance. The others featured lower down the order when ranked as per their performance in the following three-year period (2015-18).

Which were the top ranking ELSS funds in the past three years? Take a look below:

Top Performing ELSS Funds as on February 2018

Data as on February 28, 2018

Returns are compounded

(Source ACE MF, PersonalFN Research)

There were some unexpected performers over the past three years. Among the top five performing ELSSs were MOSt Focused Long Term Fund, L&T Tax Saver Fund, Principal Tax Savings Fund, and IDFC Tax Advantage (ELSS) Fund. Among these, just Principal Tax Savings Fund was present among the top 10 in the earlier period as well.

Just seven funds were present among the top 15 funds in both the periods. This is concerning because there were just 38 ELSS funds on the list. Thus, if you select ELSS funds solely by the basis of past performance, you may end up disappointed. So, before locking-in your investment for three years, think again.

How To Pick The Best ELSSs In 2018?

tax planning. While there are a host of provisions under the Income Tax Act and numerous investment avenues; in this video tutorial, we will take you through how to use mutual funds in your tax planning exercise. Also, the aspects you must consider while investing in them, so as to save tax through this investment instrument the prudent way.

Chapter #7: Conclusion – ELSS Guide

‘Do not dig well when the well only after the house catches fire’.

PersonalFN’s Exclusive Report - 3 Tax-Saving Mutual Funds For 2018.

In this report, you will find the Top 3 ELSS that are geared to grow your investment multi-fold over long term while saving your taxes. These Top 3 ELSS are handpicked through our special 7-point Selection Matrix methodology and are considered to be potentially the best tax-saving mutual funds in the Indian market.

Click here to know more about Top 3 ELSS report.

info@personalfn.com or simply contact us at 022 6136 1200.

Everything You Need To Know About Tax Planning here.

Tax Planning Guide here.

Happy Tax Planning!