Many of you would remember an investment consultant visiting you or your parents years back and recommending with integrity on various investment avenues available in market. But then, times were different. People were humane, caring, trustworthy, and seldom would anyone be betrayed.

Today the scenario is at odds. It’s rare to find a ‘financial guardian’, whom you can trust for an advice on investing and wealth creation. There are only a handful who render a financial advice diligently and ethically. There’s rampant mis-selling going on.

But to crack the whip somewhere, the Securities and Exchange Board of India (SEBI) in January 2013, made it mandatory for all mutual fund houses to launch ‘Direct Plans’ for all schemes. The rationale behind the introduction was: simplify investing and provide the benefit of lower expense ratio to those opting for ‘direct plan’ vis-à-vis a ‘regular plan’.

Here are some distinguishing features of a direct plan vs. traditional regular plan:

| Regular Plan |

Direct Plan |

| You transact through mutual fund distributor / investment advisor / relationship manager |

You directly invest either physically or online visiting registrar's or mutual fund company's office |

| The recommendation are guided by the mutual fund distributor / investment advisor / relationship manager, and there is after sales support service |

There’s no guidance. You do your own research to invest and self-help |

| Indirectly commission is paid by the fund house on the money you invest |

Since you invest directly, no commission is paid by the fund house on the money you invest |

| You incur a higher expenses ratio (due to the distributional cost involved) |

The expense ratio is lower as there is no commission to be paid to the distributor |

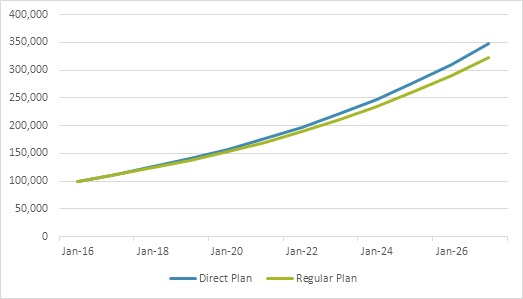

Both the plans have identical underlying portfolio, fund manager and follow same investment strategy. But a lower expense ratio for a ‘direct plan’, enables in clocking better returns than a regular plan. You might feel that the difference in their expense ratio is mere 1%; but in the long-run the returns generated by ‘direct plans’ are higher. Take a look at the chart here...

The cutting edge: Direct Plan vs. Regular Plan

Note: The above table is for illustration purpose only

(Source: PersonalFN Research)

In the above illustration assuming Fund A generates 12% CAGR and you invested Rs 1,00,000 in ‘direct plan’ its value after 10 years would be Rs 3,47,855, while in the same invested in a ‘regular plan’ would be Rs 3,23,073. It makes a difference of good +7.7% in the power of compounding . Although the difference in returns may appear small in the near-term, over the long-term it is worthy – cannot be ignored.

But direct plan is not meant for naïve investors.

If you are a diligent investor, and have fair knowledge about of how to select mutual fund schemes, you may consider investing in ‘direct plans’. But don’t ignore monitoring the funds and rebalancing the portfolio when needed. If you can do this, you don’t require a mutual fund distributor / investment advisor.

On the other hand, if you are an alien to mutual fund space but want to explore the potential of wealth creation, you might as well seek guidance of a ‘financial guardian’ who can guide you in an unbiased and an objective manner. But ensure you’re selecting a ‘financial guardian’ with enough care. Judge his/her financial knowledge and credibility, to be rest assured that you aren’t in wrong hands. A ‘financial guardian’ will help you build a portfolio recognising your risk appetite, investment objectives, investment horizon and financial goals. He will help you manage your hard earned money with as much care as he manages his own.

Investing involves a lot of research and introspection on your part as investors to have the correct investment instruments in your portfolio and to chart the right asset allocation. It is not an easy task. When you’re selecting mutual fund scheme for your portfolio thorough research and analysis is imperative, and can’t merely go by star rated funds by ignoring the rationale on which they’re rated. After all you want rock-star performance of your portfolio, and not something which sets it rolling on rocky road. So, before you reach out to your smartphone / notebook / tablet powered by high-speed internet to buy into a ‘direct plan’, ensure you’ve powered your decision with prudent and unbiased research. Because buying a financial product is not as casual as buying a gadget on amazon; you might lose your hard earned money if you chose an underperforming fund.

If you’re looking for credible, unbiased and independent research on mutual funds PersonalFN’s mutual fund research services can be the answer.

Add Comments

| Comments |

arachni_text

Jan 06, 2019

arachni_text |

arachni_text)

Jan 06, 2019

arachni_text |

arachni_text

Jan 06, 2019

arachni_text) |

arachni_text

Jan 06, 2019

arachni_text |

arachni_text

Jan 06, 2019

arachni_text |

1