Are you worried about market volatility?

You've probably read that prudent asset allocation can help you handle volatile markets effectively.

But what is asset allocation? Simply put, this is one of the most important decisions, apart from scheme selection and risk profile assessment, in your overall plan for investments.

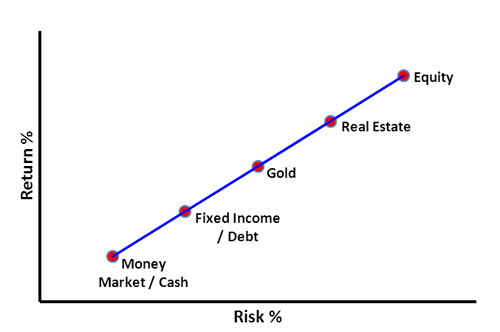

Risk-return trade off of various asset classes

Note: for illustrative purpose only,

(Source: PersonalFN Research)

Asset allocation is the proportion in which you invest in various asset classes such as debt, equity, gold, and real estate among others. It can be fixed, i.e. remains static irrespective of market conditions, or it can be dynamic, i.e. changes with market conditions.

[Read: Why You Should Not Ignore Personalized Asset Allocation While Investing ]

It works because the factors driving the prices of each of these assets are different. Basically, equity and debt as asset classes share a negative co-relation with the other asset classes. This means they often don't move in the same direction.

In 2007, investors were overinvested in equity and at the beginning of 2009 perhaps the same investors were underinvested in equity. With this, they not only lost the opportunity to encash gains, but also lost some once-in-lifetime buying opportunities.

Are you sailing in the same boat? Do you often miss attractive investment opportunities due to your behavioural biases?

If yes, why not consider balanced advantage funds at this juncture.

What are balanced advantage funds?

According to SEBI's recategorisation norms, balanced advantage funds are hybrid funds that are managed dynamically. In simple words, hybrid funds that shuffle their equity-debt mix based on market valuations and available opportunities in respective asset classes are termed as balanced advantage funds.

The best aspect of balanced advantage funds is the flexibility to invest upto 100% of their corpus in either debt or equity and optimising your returns by dynamically shifting the allocation of their portfolio in debt and equity.

Markets are likely to be extremely volatile in the election year, for many other factors apart from elections. Under such circumstances flexibility enjoyed by the balanced advantage funds can help investors tide over potentially tricky phase.

Is market outlook conducive to invest in balanced advantage funds?

The following are some of the key factors in 2019:

-

Lok Sabha election in 2019

-

Geopolitical tensions

-

International Trade impact

-

Brexit

-

Flagging economic growth

-

Need to see how central banks respond in their monetary policy action

-

Fiscal deficit management in India

-

Growth in corporate earnings

Although currently there is geopolitical tension between India and Pakistan in the South Asia region, Indian markets may not react negatively further unless both the nations engage in a full-blown war. Given the growing support of global powers to India's stand on the 'surgical strikes on terrorism' and considering Pakistan's fragile economic condition, escalation is a remote possibility.

On the global front, China and the U.S. are yet to reach mutually agreeable trade pacts. Speaking about Europe, hard Brexit might spook the markets. It remains to be seen if the U.K. gets an extension.

The Federal Reserve's monetary policy stance would be crucial; because it will largely affect the flow of global capital to emerging markets. No rate hike or rate cuts would be positives for emerging markets.

As far as the political stability in India goes, there are expectations of a stable government. It might be seen as a positive for Indian markets if the NDA government manages to retain the centre.

Although India's widening fiscal deficit is a real worry, all the other factors that drive bond markets, viz. inflation, credit growth, policy stance, liquidity, etc. continue to remain benign. Unless mutual fund houses goof up the credit quality of the portfolio, the debt component of the portfolio might remain a lot steady in 2019 as compared to that in 2018.

Suitability of balanced advantage funds in 2019...

The tactical allocation of balanced advantage funds would prove advantageous.

Some balanced advantage funds use various pre-set parameters such as Price-to-Earnings (PE) ratio or Price-to-Book (PB ratio) to name a few, to gauge the attractiveness of equity. When markets are attractively valued, they increase their equity allocation and vice-a-versa.

While others decide the asset allocation of the portfolio on various factors such as interest rates, economic outlook, equity valuations, and medium and long term market outlook, among others.

Let's suppose the markets stage a massive rally on favourable election outcomes, or otherwise, a fund manager of a balanced advantage fund can decide when to cash-in. Inversely, if markets nosedive, based on unfavourable election outcomes, valuations might cool off giving balanced advantage funds an opportunity to accumulate.

Most of the responsible and process-driven fund houses would ensure that quality portfolio of equity and debt instruments is held plus adequately diversified to deal with adverse market conditions. Markets would be keen to know if India Inc. manages to report better number in FY 2019-20. Higher growth in corporate profits might push equity indices higher.

Hence investing in balanced advantage funds at this juncture might be beneficial.

How have balanced advantage funds performed?

In the recent times, balanced advantage funds have struggled to outperform Crisil Hybrid 35+65-Aggressive Index. However, their 3-year and 5-year performance has been encouraging.

Table: Top-5 balanced advantage funds of 2018

Data as on March 11, 2019

(Source: ACE MF)

*Please note, this table only represents the best performing balanced advantage funds based solely on past returns and is NOT a recommendation.

Mutual Fund investments are subject to market risks. Read all scheme related documents carefully.

Past performance is not an indicator for future returns. The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

Balanced advantage funds that have outperformed in the long run are:

Reliance Balanced Advantage Fund(G)-Direct Plan

HDFC Balanced Advantage Fund(G)-Direct Plan

In the calendar year 2018, ICICI Pru Balanced Advantage Fund(G)-Direct Plan and Union Balanced Advantage Fund(G)-Direct Plan did well.

How to select a balanced advantage fund wisely?

Quantitative Parameters

-

Performance and risk analysis

This is to analyse if the fund has shown consistency in performance across various market periods with decent risk-adjusted returns.

Under this, the fund needs to be ranked on quantitative parameters like rolling returns across short-term and long-term periods, such as 1-year, 3-year, and 5-year as well as on risk-reward ratios like Sharpe Ratio, Sortino Ratio, and Standard Deviation over a 3-year period.

[Read: Why Comparing Returns to Risk Is More Meaningful!]

-

Performance across market cycles

You need to ensure that the fund has the ability to perform consistently across multiple market cycles. Therefore, compare the performance of the schemes vis-a-vis their benchmark index across bull phases and bear market phases.

A fund that performs well on both sides of the market should rank higher on the list.

Qualitative Parameters

-

Portfolio Quality

Adequate Diversification - The scheme should not hold a highly concentrated portfolio. The portfolio should be well-diversified and the exposure to the top-10 holdings should be ideally under 50%.

Credit Quality - For debt component, you need to ensure that the fund does not hold a high proportion of low-rated (securities rated AA or below) or unrated debt instruments. A fund with a higher credit quality should be ranked higher.

Low Churn - Engaging in high churning can result in trading and high turnover cost. Therefore, you also need to consider the portfolio turnover ratio and expenses, and penalise funds involved in high churning, i.e. those funds with a turnover ratio of more than 100%.

-

Quality of Fund Management

You also need to consider the fund manager's experience, his workload, and the consistency of the fund house. Therefore, assess the following:

The fund manager's work experience: He/she should have a decent experience in investment research and fund management, ideally over a decade. But note that experience isn't always enough. Some schemes managed by fund managers with 15-20 years of experience haven't necessarily done consistently well for a long time.

The number of schemes managed: A fund manager usually manages multiple schemes. Thus, you need to check if the fund manager is not loaded with a large number of schemes. If he is managing more than five open-ended funds, it should raise a red flag.

The efficiency of the fund house in managing your money: Do your research about the fund house's consistent performance across schemes. Find out if only a few selected schemes are doing well. A fund house that performs well across the board is an indication that their investment processes and risk management techniques are sound and efficient.

Know more about PersonalFN's research methodology here.

Watch this short video on selecting mutual fund schemes:

How to invest in balanced advantage funds?

Once you select worthy balanced advantage funds for your portfolio, start investing in them preferably through Systematic Investment Plans (SIPs). Ensure you have an investment time horizon of at least five years and an appetite for moderately high risk. With SIP, you will be able to mitigate the risk involved better vide the benefit of rupee-cost averaging. And finally, choose direct plans over a Regular Plan to invest.

Remember this when you invest in mutual funds:

-

Clearly identify your financial goals.

-

Recognise the financial goals you want to achieve and align them with your mutual fund investments.

-

Gauge the time horizon before the financial goals befall.

-

Assess your risk appetite. Only if you have a high-risk appetite and longer time horizon (at least 3-5 years) for the fulfilment of goals, invest more in equity-oriented mutual funds; otherwise, stick to debt mutual funds and other fixed-income investments.

-

Based on your risk appetite, draw up a personalised asset allocation chart and invest accordingly.

-

And last but not the least; keep reviewing your investment so as to ensure you're on track to accomplishing your envisioned financial goals.

Editor's note: Are you looking for "high investment gains at relatively moderate risk"? We have a ready solution that could be suitable for you -- PersonalFN's Premium Report, "The Strategic Funds Portfolio For 2025( 2019 Edition)".

In the 2019 Edition of PersonalFN's Premium Report, "The Strategic Funds Portfolio For 2025", you will get access to a readymade portfolio of its top recommended equity mutual funds for 2025 that have the ability to generate lucrative returns over the next five to six years. Subscribe now!

Author: PersonalFN Content & Research Team