Why Gold Is Falling After Modi 3.0's Budget 2024-25 and Should You Invest Now

Rounaq Neroy

Jul 30, 2024 / Reading Time: Approx. 9 mins

Listen to Why Gold Is Falling After Modi 3.0's Budget 2024-25 and Should You Invest Now

00:00

00:00

In the last couple of years, particularly since the COVID-19 pandemic, gold has had a dream run taking the price per 10 grams of gold to a historical high of over Rs 74,000.

Since March 2020, the precious yellow metal has produced a compounded annualised return of nearly 12% (in INR terms).

However, after Modi 3.0's full budget 2024-25 (presented on July 23, 2024), gold has retraced by nearly 6% (as of July 29, 2024).

So, what did finance minister Ms Nirmala Sitharaman state in her budget speech that the precious yellow metal lost some sheen?

Well, the budget proposed to reduce the basic customs duty on gold from 15% to 6%. This led to a remarkable fall in the price of gold. Nearly, Rs 10.7 trillion in value was lost in a day on the commodities exchange.

Reduction in basic customs duty, which was a long-standing demand of gold merchants, (as it would reduce smuggling and yield higher tax revenue for the exchequer), made gold import cheaper.

Moreover, the customs duty was reduced by the finance minister to enhance the domestic value addition in gold along with precious metal jewellery in the country.

How Did Investors React?

The reduced price of gold has revived demand. It has encouraged many individuals to buy gold, ahead of the festive season. Jewellers have already reported a rise in daily demand.

So, it looks like the dip in gold is temporary. Abetted by demand, gold still looks resilient.

Should You Buy Gold?

In India, as you know, gold is a coveted asset class, symbolic of Goddess Laksmi.

The spotlights still continue to be on the precious yellow metal, owing to factors such as:

- Looming geopolitical tensions

- Geoeconomic fragmentation

- Increased incidences of climate shocks

- Potential supply chain disruptions

- Risks to the inflation trajectory

- The burgeoning debt-to-GDP ratio of many major economies -- higher than the pre-pandemic levels

Further, the results of the forthcoming general elections in the U.S. shall give insight as to how the geopolitical landscape takes shape and the economic policies that would be rolled out, which, in turn, would pave the way forward for gold.

[Read: How Would Gold Perform in 2024]

To know how gold will fare in 2024, watch this video:

Much also depends on policy interest rate actions of central banks (which hinges on the inflation trajectory).

The European Central Bank (ECB), earlier in June 2024, cut its policy interest rate from a record high. Another rate cut by the ECB in September 2024 seems to be a possibility.

The U.S. Federal Reserve, too, would open the door for rate cuts as soon as September by reducing rates by around 25 basis points, acknowledging that inflation has moved closer to the central bank's inflation target of 2% and backed by signs of economic vigour.

If enabled by inflation, major central banks, cut the policy interest rates, it would act as a catalyst for gold, according to the World Gold Council (WGC).

The aforementioned backdrop makes it worthwhile to own gold in your portfolio at these lower prices. The precious yellow metal would play the role of being a hedge, a store of value, and a safe haven in times of economic and political uncertainty.

Even central banks, recognising the risks in play, as part of their reserve management, are buying gold.

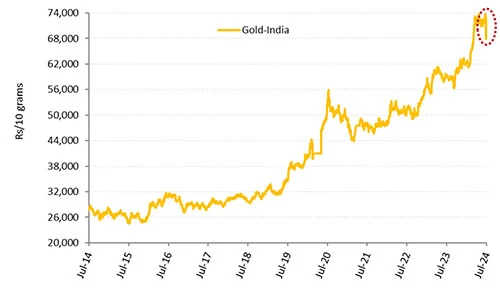

Graph 1: Gold Has Exhibited a Long-Term Uptrend

Data as of July 29, 2024MCX spot price of gold used.

Data as of July 29, 2024MCX spot price of gold used.

Past performance is not indicative of future returns.

(Source: MCX, data collated by PersonalFN Research)

The graph above shows that gold has fared remarkably well in the last decade. Even a stronger U.S. Dollar -- typically seen during the stagflation period - hasn't dampened the sentiments toward gold.

The long-term uptrend exhibited by gold cannot be ignored and it highlights the importance of owning it in the portfolio.

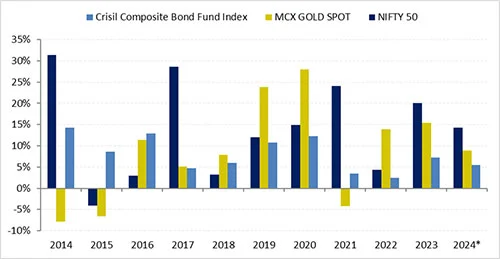

Graph 2: Gold Shall Play Its Role in Your Portfolio

*Data as of July 29, 2024

*Data as of July 29, 2024

MCX spot price of gold used. Returns expressed are in absolute terms considering domestic currency.

Past performance is not indicative of future returns.

(Source: MCX, ACE MF, data collated by PersonalFN Research)

You see, in years such as 2016, 2018, and 2022, when equities disappointed investors with poor returns, gold turned bold and proved to be a hedge (due to an inverse correlation usually between the two asset classes) and played the role of effective diversifier.

A fact is that, unlike financial assets, gold is a real asset - meaning gold does not carry credit or counterparty risk.

Thus, strategically allocate around 10% to 15% of your entire investment portfolio towards gold and hold with a long-term view (of over 8 to 10 years) by assuming moderately high risk.

How to Buy Gold Now?

I suggest buying gold the smart way - in the form of a Gold ETF and/or Gold Savings Fund (which essentially are gold mutual funds), instead of buying physical gold, which adds to storage and security costs, plus the risk of theft or being misplaced.

[Read: Top 5 Gold Mutual Funds for 2024]

Gold ETFs aim to track the domestic price of physical gold; they are passively managed and make direct investments in gold. To gain exposure to gold without having the hassle of physically holding it, a gold ETF is a worthwhile option.

The investment objective of a gold ETF is to generate returns broadly in line with the domestic price of gold. If gold appreciates, you benefit.

The units purchased will be backed by 0.995 finesse of physical gold by the respective fund house. The physical gold is held in vaults by an appointed custodian for the ETF on your, the investors' behalf, plus insured and valued periodically, as per the guidelines stipulated by the Securities and Exchange Board of India (SEBI).

To invest in Gold ETFs, you need a demat account and trading account, and the purchase order can be placed through your broker - just like the way you buy shares on the recognised stock exchange. Conversion of gold ETF units into physical gold at a future date is also possible for a certain quantity (usually 1 kg.)

A Gold Saving Fund, on the other hand, is a fund-of-fund scheme investing in underlying Gold ETFs, which benchmarks the performance against the prices of physical gold. It strives to produce parallel returns that closely resemble the underlying Gold ETF and price of gold.

The investment objective of a Gold Savings Fund is to generate returns that closely correspond to returns generated by the underlying Gold ETF.

The advantage of investing in a Gold Savings Fund is that you can invest through the regular investment process without holding or opening a demat account. The units of the Gold Savings Fund will be purchased at the NAV declared by the fund house, and the allotted units will be reflected in your mutual fund account statement.

Furthermore, it facilitates investing in a disciplined manner through the Systematic Investment Plan (SIP) mode with a sum of as little as Rs 500. It offers affordability, convenience, flexibility, potential for long-term wealth creation, and liquidity.

At a time when gold in INR terms has corrected, it makes sense to add gold even by making a lump sum investment.

Beware of the Tax Implications

In the full budget 2024-25, changes are also made to the capital gain tax regime.

Now units of gold ETF and/or gold mutual funds (which are 'financial assets'), when held for less than 24 months and sold at a capital gain, will be classified as Short Term Capital Gain (STCG) and taxed as per your, the investor or assessee's, income-tax slab (i.e. at the marginal rate of taxation).

On the other hand, if the units of gold ETF and/or gold mutual funds were held for 24 months or more and sold at a gain, it will be classified as Long Term Capital Gain (LTCG). The LTCG will be taxed at a flat 12.5% without any indexation benefit available.

Before July 23, 2024, the capital gains or returns from gold ETFs and gold mutual funds were taxable as per one's income-tax slab, irrespective of whether STCG or LTCG.

[Read: Key Changes in Taxation of Mutual Funds After the Union Budget 2024-25]

As regards, the tax implication of physical gold -- a 'non-financial asset' -- the union budget 2024-25 proposed that the STCG (holding period of less than 24 months) will continue to attract the applicable tax rate of the assessee - in other words as per one's income-tax slab (i.e. at the marginal rate of taxation).

On the other hand, the LTCG on physical gold, like all financial assets, is now taxed at 12.5% with no indexation benefit available.

Earlier, i.e. before July 23, 2024, in the case of physical gold, when the holding period was 36 months or more, LTCG were taxed 20% with indexation benefit available, whereas STCG (holding period of less than 36 months) were taxed as per one's income-tax slab.

To conclude...

Add gold sensibly to your portfolio by taking advantage of the price correction being mindful of the asset allocation best suited for you. During the festive season, as demand increases, gold prices would see an uptick.

Safeguard your financial future with sensible allocation to gold in your portfolio. The precious yellow metal shall play its role of being an effective portfolio diversifier and be store of value.

Be a thoughtful investor.

Happy Investing!

Join Now: PersonalFN is now on Telegram. Join FREE Today to get PersonalFN’s newsletter ‘Daily Wealth Letter’ and Exclusive Updates on Mutual Funds.

-New.png)

ROUNAQ NEROY heads the content activity at PersonalFN and is the Chief Editor of PersonalFN’s newsletter, The Daily Wealth Letter.

As the co-editor of premium services, viz. Investment Ideas Note, the Multi-Asset Corner Report, and the Retire Rich Report; Rounaq brings forth potentially the best investment ideas and opportunities to help investors plan for a happy and blissful financial future.

He has also authored and been the voice of PersonalFN’s e-learning course -- which aims at helping investors become their own financial planners. Besides, he actively contributes to a variety of issues of Money Simplified, PersonalFN’s e-guides in the endeavour and passion to educate investors.

He is a post-graduate in commerce (M. Com), with an MBA in Finance, and a gold medallist in Certificate Programme in Capital Market (from BSE Training Institute in association with JBIMS). Rounaq holds over 18+ years of experience in the financial services industry.

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. Registration granted by SEBI, Membership of BASL and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.

Disclaimer: This article is for information purposes only and is not meant to influence your investment decisions. It should not be treated as a mutual fund recommendation or advice to make an investment decision in the above-mentioned schemes. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and use such independent advisors as he believes necessary.