Medical costs are increasing day by day and your

existing health insurance policy may not be sufficient to cover all your hospitalization expenses. To help you bear medical costs Aegon Religare has come up with Aegon Religare iHealth Plan.

This plan has some new and exciting features which are being highlighted by the company when speaking to potential customers, such as:

- This policy pays a guaranteed amount irrespective of hospital bill

- It does not increase premium even in case of a claim

- It allows you to increase your coverage amount

- Guaranteed Lifelong Renewal

- It covers your family members under one policy

When looking at any health insurance policy, it is very important to ask the right questions, especially about features that are being highlighted. Let's get started:

1. What is Aegon Religare iHealth Plan?

This policy is essentially a surgery payout and daily cash benefit policy which also gives you Critical Illness as a rider. It is not a Mediclaim policy and should not be considered one. If you choose to take this policy, you must also have a separate

Mediclaim policy for yourself.

2. What are the key features of this policy?

For starters, the policy offers 3 payments: a) Surgery - fixed, pre-determined lump sum payout on surgery, depending on the category b) Daily Hospitalization - regardless of what your daily hospital charges come to, you will receive a fixed amount (details are given ahead). Your daily charges (room rent, doctor's visits, medication and treatment, injections etc) may be less or more than what your fixed Daily Hospitalization payout is under this policy. c) Critical Illness - fixed, pre-determined lump sum payout on diagnosis

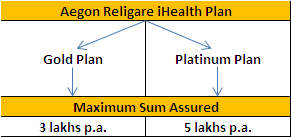

The policy has 2 options under it, each with different sum assured limit:

Under both the Gold and Platinum Plan 849 different Surgeries are covered. If you have to undergo any of the 849 surgeries then you will receive a lump sum payment based on the surgery category as defined by Aegon Religare. Payout for any surgery will depend upon the category to which the surgery falls in as these 849 surgeries are divided into 5 different categories. Each category has a different payout:

| Surgical Cash Benefit: |

Payout under Gold Plan (Rs.) |

Payout under Platinum Plan (Rs.) |

| Category 1 |

300,000 |

500,000 |

| Category 2 |

240,000 |

400,000 |

| Category 3 |

120,000 |

200,000 |

| Category 4 |

60,000 |

100,000 |

| Category 5 |

30,000 |

50,000 |

| Category 6 (Min. 24 hours Hospitalization Req.) |

15,000 |

25,000 |

| Lifetime Limit for Surgical Cash Benefit |

1,500,000 |

2,500,000 |

Example:If you have opted for Platinum Plan and you have to undergo a surgery which falls under Category 2 then you will receive Rs. 4 lakhs as Surgical Cash Benefit.

But there's an important point to note: There's a maximum annual payout. If you have to again undergo a surgery within the same policy year and this time your surgery falls under Category 3 then you will not receive Rs. 2 lakhs, instead you will receive just Rs. 1 lakh as the annual limit under Platinum Plan is Rs. 5 lakhs. In short, for surgery, you have a maximum annual payout allowed each year under this policy, if you undergo surgery which costs more; the additional payment has to be borne by you.

3. Is the lifetime renewal guaranteed?

Yes, Aegon Religare iHealth Health Plan can be renewed till lifetime. But here's a sub-point that goes with it: it has Lifetime Limit for Surgical Cash Benefit. This means that if you have opted for the Platinum Plan for example, and have claimed 5 times already i.e. (5 * Rs. 5 lakhs) under Category 1 by the age of 70 years for example, then you have exhausted your Lifetime Limit for Surgical Cash Benefit which is Rs.25 lakhs and the policy can no longer be renewed.

This is restrictive because in effect, what the company is doing is saying 'if you need more surgeries, we won't pay beyond a certain amount'. It makes sense for the company, but not for the policyholder of course.

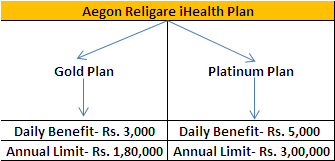

4. What about the Daily Hospitalization payout?

Apart from the Surgical Cash Benefit this policy also provides a fixed Daily Hospitalization Cash Benefit. This benefit is paid out for the number of days you are admitted in the hospital.

The annual limit is determined by multiplying the daily limit x 60 days (assuming you will be hospitalized for a maximum of 2 months in the year). The assumption of 60 days is generous, but the daily payout is not. So if you are hospitalized in a top class hospital for even a few days, this will not cover your daily hospital expenses completely.

5. What about the Critical Illness payout?

This is a convenient feature of the policy. Once the policyholder is diagnosed with a

critical illness, it makes a payout (fixed and pre-determined), regardless of whether you are admitted to hospital or not.

Take the example of somebody who has been diagnosed with a critical illness.

He contacts Aegon Religare, who upon receiving the relevant documentation, makes a cheque payment to the policyholder. Then later he gets admitted to hospital. The policy pays a daily hospitalization benefit. During his stay it is advisable that he undergoes a surgery. The policy makes a fixed surgery payout to the policyholder. So this policy covers critical illness payout (on diagnosis), daily hospitalization, and surgery payout as well.

And here, there's a benefit involved: You can make what they call a 'dual claim'.

This is a part of any critical illness policy, not just Aegon Religare's iHealth Plan.

If you have an existing Mediclaim policy which you make a claim on, upon being hospitalized, you can also claim a fixed amount from this policy. They will pay the full fixed amount, regardless of what you are paid from your other insurance company.

6. What diseases are covered?

The Critical Illness rider under this policy covers 10 critical diseases. If you opt for this rider and are diagnosed with any of the critical disease (Mentioned in below table) then you will receive a lump sum amount of Rs. 3 lakhs under Gold Plan and Rs. 5 lakhs under Platinum Plan.

| Diseases covered under Critical Illness Rider: |

| 1 |

Alzheimer's disease |

| 2 |

Muscular dystrophy |

| 3 |

Cancer |

| 4 |

Paralysis |

| 5 |

Aplastic anaemia |

| 6 |

Blindness |

| 7 |

Cardiomypathy |

| 8 |

Stroke |

| 9 |

Coma |

| 10 |

Kidney Failure |

So what's the conclusion?

As a backup plan, the policy is a good one. It has its restrictions, as do all policies, and as with all policies, you need to read the document very carefully and ask questions to get the information you really need. Before taking this or any other policy, speak with your

financial planner, and also go through the list of diseases / illnesses covered to see if this is what runs in your heredity.

Add Comments

| Comments |

kotrappa06@gmail.com

Aug 07, 2012

How is this policy is different from ICICI Health Saver both in terms of premiums and health risks covers |

pravin_1506@rediffmail.com

Aug 10, 2012

what is premium |

gourisankar.padhi@larsentoubro.com

Aug 10, 2012

What is the premium for Gold Plan |

1