If they do it often, it isn’t a mistake; it’s just their behavior—Dr. Steve Maraboli

It seems mutual funds are proving Dr. Steve Maraboli right. They are displaying exactly the same trait—repeating mistakes too often. In the asset manager’s fraternity and even in investor’s community it is assumed that fixed income bearing instruments are safer than equities. Although there is a lot of merit in this argument, it’s not always true. Debt securities issued by a fallible borrower are as risky as equities issued by a half-baked promotor.

It would be impossible to find a person who has never committed any mistake. It’s perfectly fine to make mistakes; but not learning anything from them is not acceptable. Psychological studies suggest that people tend to do same mistakes time and again mainly because of factors mentioned below.

- Lack of ability to deal with stress

- Poor assessment of the situation

- Overconfidence and self-obsession

- Impulsiveness

Some mutual funds have a lot to answer. Are they impulsive, poor judge of the situation or simply over confident of their abilities? Investors invest in debt funds perceiving them safer than equity oriented funds but when even debt funds start giving them sleepless nights, they feel dismayed, disgusted and betrayed.

New Episode

Memories of Amtek Auto are still fresh. A responsible fund house such as JP Morgan apparently failed to recognise the weakness in Amtek’s ability to repay loans. Investors of two schemes of the fund house that had exposure to debt securities of the troubled companies made heavy losses. Eventually the fund house successfully recovered most of its money but what was lost (close to 15% of the total exposure) wasn’t acceptable either, especially for debt fund investors. It appeared that, at the time of investing, the fund house solely depended on the credit rating provided by the independent rating agencies which is why it flunked when credit rating agencies couldn’t provide updates on the creditworthiness of the company and changes therein.

Would you invest in debt securities of this company?

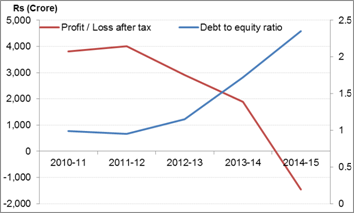

History seems to be repeating itself. Before, you learn about the better version of Amtek Episode; please relook at the chart above, in case you missed that out or simply felt you may ignore it.

The chart is based on the facts. It shows how company’s fundamentals have deteriorated. From a profit making it has turned into a loss making company. Debt pile has made the situation scarier. Debt to equity ratio of 2.35 suggests that company has borrowed Rs 2.35 against every Rupee of equity. Would you invest in this company’s debt? Very few of you might.

By the way the company in discussion is Jindal Steel and Power Ltd. And all figures quoted in the chart are taken from the annual reports of the company. Going by quarterly results for first 3 quarters so far, the company is unlikely to report profits even in the Financial Year (FY) 2015-16. In first 9 months of the current FY, the company has incurred a little over Rs 1,600 crore of losses.

The table given below tells you where the company has been borrowing from.

Crushed under debt?

| Sources of debt |

Rs in Crore |

| Bank loan facility |

32,638 |

| Non-Convertible Debentures |

3,212 |

| Commercial Papers |

4,150 |

| Total Debt |

40,000 |

(Source: CRISIL report dated February 12, 2016)

As reported by Business Standard dated February 17, 2016; mutual funds collectively have the exposure of Rs 2,500 crore to JSPL’s 40,000 crore debt. Reputed fund houses such as Franklin Templeton Mutual Fund, ICICI Prudential Mutual Fund and Reliance Mutual Fund have dabbled in JSPL. They have exposure of Rs 1,600 crore, Rs 500 crore and Rs 49 crore respectively as reported by Business Standard dated February 17, 2016. Franklin Templeton is exposed to the highest risk as it holds papers with the residual maturity of 4 to 5 years.

Recently CRISIL downgraded the rating on JSPL from 'CRISIL BBB+/CRISIL A3+' to CRISIL BB+/CRISIL A4+. As per the report rationales behind the rating downgrade are;

- Possibility of a severe cash crunch in the near term

- The performance of the company is expected to remain under pressure across business segments

- The initiatives taken by the Government recently to improve the overall health of sectors in which company operates, may take longer to contribute positively in company’s profits

The CRISIL report also has mentions about healthy market position of JSPL in the steel industry, its value-added and superior product profile and proximity to raw material sources. However, all these positives, as claimed in the report, are challenged by the poor financial position of the company and unlikeliness of improvement in business prospects in foreseeable future.

Recently, Securities and Exchange Board of India (SEBI) issued new exposure guidelines for mutual funds. In case of JSPL, mutual funds are unlikely to have violated any of those norms yet it remains to be seen how long would it take for them to understand investor’s anxiety? Whenever such news comes forth, Net Asset Values (NAVs) of schemes having exposure to troubled companies go down resulting in losses to investors. SEBI has also advised mutual funds on carrying out their own assessment instead of solely depending on independent rating agencies. Investors can only hope SEBI won’t tolerate such behaviour of mutual funds.

Learn from the mistakes of others…you can’t live long enough to make them all yourselves—Chankanya

Like PersonalFN you can only expect that mutual funds will learn from the mistakes of others and avoid investing in deb laden and loss making companies.

Add Comments

| Comments |

vasantshukla@gmail.com

Apr 04, 2016

The investment in these kind of instruments can be attributed only by two reasons:

One is to outperform the returns of other mutual funds and the other one is to ever greening the bonds as the issuer is unable to repay the issue amount. what we can see can be seen by the Fund Mangers as well but in the race to be better everyone compromises. |

1