(Image source: Unsplash.com)

(Image source: Unsplash.com)

The Reserve Bank of India (RBI) has reduced repo rates by 25bps at the first bi-monthly monetary policy of FY 2019-20. As you know, bond prices and interest rates are inversely proportional.

Experts expect the RBI to cut policy rates further this financial year. At this juncture, the BIG question is: Is it a right time to invest in dynamic bond funds?

[Read: Will RBI Cut Rates In Its April Policy And How To Invest In Debt Funds Now?]

Let's understand if dynamic bond funds are suitable for your portfolio...

If you want to benefit from the movement of interest rate without speculating its timing, a dynamic bond fund might be a worthy category to consider right now.

A dynamic bond fund, according to SEBI categorisation norms, is an open-ended dynamic debt scheme that invests across durations.

Duration, or Macaulay Duration, as applicable in this case, is the current value of all future cash flows, which includes interest payments and the maturity value. While the maturity profile of securities held in a portfolio affect the Macaulay Duration, don't confuse it with the average maturity of the bond portfolio.

Yield to Maturity (YTM), coupon payments, coupon rate, current price, and time to maturity affect the calculation of the Macaulay Duration.

In layman's language, higher the Macaulay Duration, greater the risk involved in the investment proposition.

Since dynamic bond funds invest across durations, the risk profile can be quite different from one another, as well as the returns they generate. For example, a dynamic bond fund that anticipates an escalating interest rate scenario will have a low duration and vice-a-versa.

Although dynamic bond funds can invest across duration and have a flexibility that churns the portfolio to change their stance, they are only suitable for investors whose financial goals have a time horizon of over three years.

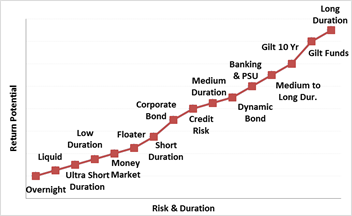

Graph: - Risk-return trade off: debt funds

(Source: PersonalFN Research)

Dynamic bond funds are riskier than credit risk funds and medium duration funds. Only sector specific debt funds and long duration funds carry more risk as compared to dynamic bond funds. Hence, you should stay away from them unless you actually have a high-risk appetite.

Where dynamic funds invest?

Dynamic bond schemes have flexibility to move across short-term instruments, such as commercial paper (CP) and certificates of deposit (CDs), or long-term instruments, such as corporate bonds and gilt securities, depending on their outlook on interest rates.

They decide on which type of short-term or long-term debt instrument to invest in-depending on where interest rates are heading.

Dynamic bond funds bet on the interest rate movement and prefer to churn the portfolio accordingly, rather than investing in a debt instrument and holding it up to maturity for coupon payments.

Investing in dynamic bond funds at this juncture

Investing aggressively at the longer end of the yield curve could prove imprudent, although the RBI has taken an accommodative stance already and may honour it with another rate cut of 25 bps.

Investing in long-term debt funds (holding longer maturity debt papers) can be risky in the foreseeable future. If inflation moves up or down, it will then limit the RBI's scope of reducing policy rates further. Currently, shorter maturity papers are more attractive.

[Read: Are Debt-Fund Investors Getting Wiser?]

So ideally, you'll be better off if you deploy your hard-earned money in short-term debt funds. Just ensure you're giving due importance to your investment time horizon, asset allocation, and diversification.

Consider investing in short-term debt funds for an investment horizon of up to two years.

If you, as an investor, have an investment horizon of 3 to 6 months, ultra-short duration funds would be the most suitable.

Here are a couple of benefits dynamic bond funds can offer...

Dynamic bond funds have the flexibility to change the portfolio duration according to changes in the interest rate scenario.

Since the fund manager of dynamic bond funds chiefly banks on the interest rate movement and doesn't prefer to hold bonds up to maturity, dynamic bond funds can generate attractive returns when the interest rates are expected to fall.

Benefit of investing at this juncture in dynamic bond funds is...

If RBI continues to reduce rates, dynamic bond funds many have a good run going forward.

Be wary of these risks...

If you think investing in debt funds isn't risky, think again. Though the volatility may not be as high as in the equity market, there are still chances of you losing money. No investor wishes to experience this dreaded situation. With dynamic bond funds, if interest rates move in the direction opposite to the expectations of the fund manager's, it can lead to serious losses for the investor.

At the same time, if liquidity issues crop up and the fund manager fails to sell a bond at a desired price, the losses can be substantial. Moreover, frequent churning can push the expense ratio of dynamic bond funds higher.

Going by the recent instances, the credit risk has been rising across debt fund categories. So far, dynamic bond funds have been affected less by the deterioration in the credit quality. Nonetheless, credit quality, in general deteriorates further, the risk profile of a dynamic bond fund might go up significantly as is in addition to interest rate risks, credit risks could unexpectedly become more relevant for the dynamic bond funds.

Hence, as an investor, you need to pick the right debt fund for your risk appetite and financial goals.

How have they performed?

As a category, dynamic bond funds have managed to beat Crisil Composite Bond Fund Index across time frames, except for that one, 6-month period.

Table: Performance of dynamic bond funds across timeframes...

Data as on 12th April 2019

(Source ACE MF)

*Please note, this table only represents the best performing dynamic bond funds based solely on past returns and is NOT a recommendation.

Mutual Fund investments are subject to market risks. Read all scheme related documents carefully. Past performance is not an indicator for future returns.

The percentage returns shown are only for an indicative purpose. Speak to your investment advisor for further assistance before investing.

What investors shall do?

If you prefer to invest in dynamic bond funds right now, you should only stay with schemes offered by process-driven fund houses. This means, don't rely on the returns dynamic bond funds have generated in the recent past. You should analyse them on all quantitative and qualitative parameters.

Editor's note: We have a ready solution if you are looking at high rewards with moderate risk: PersonalFN's Premium Report, "The Strategic Funds Portfolio For 2025(2019 Edition)".

In the 2019 Edition of PersonalFN's Premium Report, "The Strategic Funds Portfolio For 2025", you will get access to a ready-made portfolio of top recommended equity mutual funds for 2025 based on the core & satellite approach to investing. These mutual fund schemes have the ability to generate lucrative returns over the next 7-8 years. Subscribe now!

Add Comments