(Image source: freepik.com)

(Image source: freepik.com)

"Our lifestyle is far different from our forefathers; we live in an era where things change at a rapid pace. Some of us live in the moment, do not think of the future, and believe in instant gratification."

My friend, Priya, was giving me 'gyan' on leading life to the fullest and not worrying about tomorrow, as you lose out on so many precious moments of life.

As a counter argument, I quoted, Boniface Sagini

"We want instant lunch, instant cure, instant miracles, instant salary, instant success-instant everything. This instant civilization, we have obsessed with, has made us grow a tad too impatient in virtually everything, about life. And of course, that doesn't serve us so well."

And further added, if we do not think of retirement when we are young and only think about instant gratifying our present-day wants and desires, we will end up broke at retirement.

[Read: Worried Of Being Broke During Retirement? Here's What You Can Do to Prevent It...]

Priya asked pensively, "So then, what should we do?"

"Practice a little delayed gratification!", quick came my response.

"How?", Priya asked.

Here's what I explained...

Effective financial planning will not only help you enjoy the little moments of life, but it will also ensure that you continue to lead a rich blissful life during your retirement.

Retirement is an inescapable phase of life that one eventually encounters. A time when you no longer deal with the routine of waking-up and rushing to work; it's a time to take it easy and enjoy the fruits of decades of labour. A time that you do not want to worry about money and trivial issues, and instead pursue new passions or hobbies, spend time with family and friends, or travel to new destinations.

[Read: Want To Retire Rich And Travel The World? Read This!]

If you're still ruminating about: "Why is it important to plan for retirement?"

When you retire, you will no longer receive a salary/ earn a regular income, but the expenses continue. The years between your retirement to demise are unpredictable; however, financially preparing for this time of our lives is imperative for our survival.

The only difference in life after you retire is that life continues with its fair share of expenses and uncertainties, but you might not have a fixed flow of income. Our investments/savings act as a steady source of income during our retirement phase.

But let me remind you, mere savings in the bank will be exhausted within a short span of time; mainly because of the inflation bug. Inflation is the increase in price of goods and services. And hence, the value of your money declines because of inflation.

Plus, you can deal with medical emergencies, life's contingencies, achieve financial freedom, and be independent with effective planning.

And for this you need to save and invest for the future, now!

So, if you start early, to plan for your retirement, and follow the plan in a disciplined manner, you will be able to accumulate more wealth due to the power of compounding.

[Read: How 'Early Bird Gets The Worm' Strategy Works In Real Life]

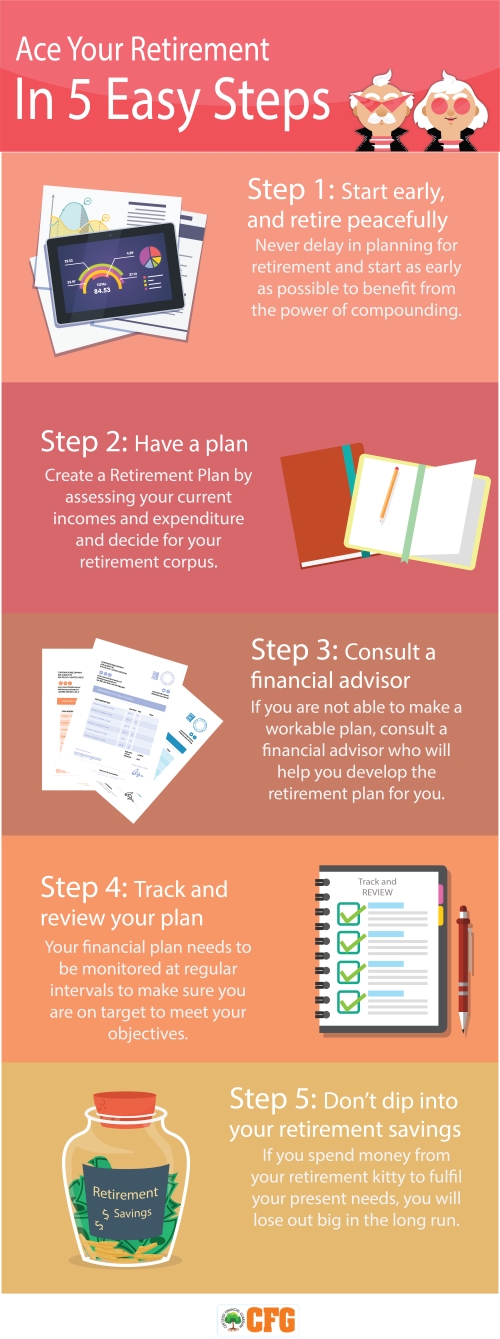

These five steps explain how to ace your retirement.

A point to note, wealth---its creation, utilisation, and accumulation---is a very subjective matter, and the truth is, no matter how much wealth we accumulate, it never ceases to be enough. The amount of wealth required for retirement should be huge such that you can continue to lead the lifestyle you dream of.

During your working years, if you follow these practices and live a little frugally, you can achieve your desired retirement corpus...

-

Controlled expenditure;

-

Avoiding any debt burden (loan or credit card);

-

Saving to invest mindfully;

-

Not following the herd/noise;

-

Not getting swayed by their emotions;

-

Seeking guidance; and

-

Do your own research to know the level of risk-adjusted inflationary returns you can earn by choosing an appropriate mix of various asset classes.

Coupled with right investment avenues and investing systematically, diligently for longer time horizon is sure to build wealth for you.

To estimate the amount you need for a blissful retirement, use PersonalFN's retirement calculator, an online tool that helps you to calculate your retirement corpus. Further, you can use this Retirement Calculator to find out the future value of your current expenses.

Where should one invest?

As mentioned, saving and investing for your retirement is imperative and choosing the right asset class mix will help in building your adequate retirement corpus. In fact, from a plethora of investment options available, understand that there's some level of risk associated with each one. Choosing an appropriate combination of various assets, equities, debt and gold will help.

Mutual funds are worthy to give you an opportunity to invest across asset classes and mitigate the risk with proper diversification to suit your risk profile. Here are two of the major ones:

-

Equities are extremely volatile in nature, although they do provide better returns in the long run. Allocating some portion of your investments to equity funds can help in wealth accumulation, albeit at high risk. To mitigate the risk, you could add debt investments and gold to the portfolio.

-

Debt as an asset class is safe as compared to equity and provides one's portfolio stability with emphasis on generating a regular income stream. Debt investment isn't risk-free, but the category of debt-oriented mutual funds can be of immense help because it diversifies the risk and provides regular income.

So, assess your risk profile before investing and only do so depending on your overall risk profile.

Table1: Various assets and their attributes

|

Equity Fund |

Debt Fund |

Gold Fund |

| Return |

High Capital Appreciation & Dividend Income |

Low Capital Appreciation |

Medium Capital Appreciation |

| Risk |

High |

Moderate to Low |

Moderate |

| Liquidity |

High |

Medium to high |

Medium |

| Suitability |

For investors having a long-term investment horizon and a high-risk appetite |

For investors having a short to medium term investment horizon and a moderate to low-risk appetite |

For investors having a medium to long term investment horizon and a moderate risk appetite (5 to 10% asset allocation) |

The above table is for illustration purpose only

Finally, I reminded Priya, "Most of us, especially millennials and Y gens, live in a world where anything we desire can be allayed, slaked, and gratified almost instantly. For generations, corporations and advertising/marketing agencies have been consistently endorsing these sentiments to grow businesses. In attempts to keep up with trends and fads, become socially acceptable, and fulfil emotional lacunas, people erode their earnings and assets. Extreme materialism and consumerism are fuelled by catch phrases and hashtags like "Live-In-The-Moment", "Buy-Now-Pay-Later", "You-Only-Live-Once", "Say-Yes-To-Happiness", etc.

But this trend is changing, with movements like FIRE catching on, early retirement plans and retirement plans in general calls for a 180-degree shift in our attitude towards spending and personal finance."

Priya thanked me and decided to get in touch with PersonalfN financial planners to begin investing for her blissful retirement.

I hope you too are on the ball with your retirement planning. Remember, the early bird gets a bigger worm. If you haven't started yet, begin today. Better late than never. So, start Now!

Editor's Note:

If you too want to retire blissfully and rich, don't miss out on PersonalFN's Retire Rich service. This is a new exclusive service designed with the sole intent of securing your retirement fund.

You will even gain the benefit of investing in Top 5 funds along with a DIY (Do It Yourself) retirement solution, where you can start planning for your retirement and potentially build a substantial corpus that could sustain you in the golden years of your life.

Add Comments