When the easy money is gushing; it goes all over places creating asset bubbles but when the flow of liquidity dries up, these asset classes go belly-up. Emerging Markets (EMs) is one of the best examples. Not long ago, before the storm of US subprime crisis hit the global financial system; it was believed that the sun will never set in the Emerging markets. Rightly so. Favourable demographics, robust GDP growth, burgeoning middle class, ever increasing investments in building new capacities; all these factors were pointing towards the better tomorrow. India was no exception to this popular perception. Indian Equities was one of the most preferred places for global investors; and still is. However, now the only difference is smaller companies which were once perceived as dark horses; have been left in the dark. Small cap stocks are being butchered in every market downfall. We believe it is important to analyse, at this juncture, how investment in small cap stocks or small cap focused mutual funds has done so far and also expound on how the future looks like for small cap funds.

| BSE Small Cap Vs BSE 200 |

Are the Small Caps Bottoming Out? |

|

|

(Source: BSE India, PersonalFN Research)

Flash Back

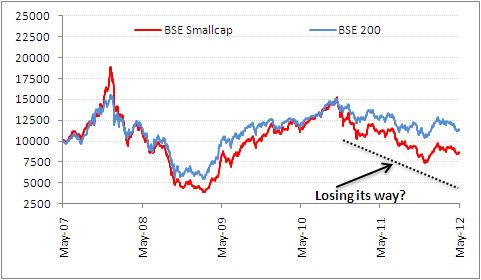

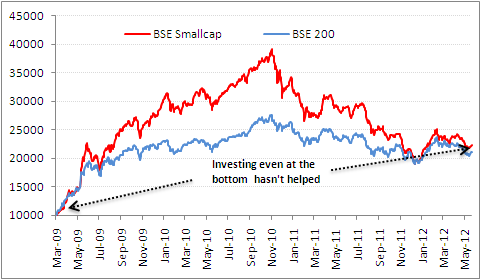

The small caps are more volatile than the bigger companies. BSE 200, which represents the broader market movement, has been a lot more stable in comparison with BSE Smallcap Index. The graph on the left hand side shows that if one had invested a sum of Rs. 10,000 in BSE Smallcap on May 29, 2007, five year later the investment would have returned just Rs. 8,641 - destruction of wealth. Similar investment in BSE 200 done on the same day would have fetched Rs. 11,472 on May 29, 2012. The graph on the right hand side again highlights the violent nature of the small caps. Investment done in BSE Smallcap even at the market bottom in March 2009, would have performed only at par with BSE 200 if one were to hold it till May 29, 2012. Those who could sell in November 2010 would have made huge profits; but which is very unlikely in the case of retail investors.

Investment in small caps through a Mutual Fund route

Mutual Fund houses went gung-ho on small and midcap funds during the euphoric bull market of 2003-2008 but many of them couldn’t time the market. The small cap funds were launched, in most of the cases, towards the end of the dream run of multi-year bull market. Small cap funds which were launched at the first leg of correction i.e. within first two months from the market peak of January 2008, received a nasty blow during the market downtrend. Let’s now look at their performance.

How the Small Cap Funds Have Fared?

* Since Inception

NAV Data as on May 23, 2012

(Source: ACE MF; PersonalFN Research)

The table above reveals that small cap funds have fared better than the BSE small cap Index on different time frames. This is mainly due to the asset allocation these funds have broadly followed. By and large, small cap focused funds invest minimum 65% of assets in small cap companies; however, they have a flexibility to invest about 35% of assets in stocks other than small caps. In other words, these funds can invest about 1/3rd of their portfolio in large caps or larger midcaps. This provides them some stability when the small caps are shunned by the market.

Where do they invest?

Small cap focused funds usually invest around 65%-90% of their assets in the constituents of BSE small cap index or the CNX Small cap index. On the other hand, those funds which are predominantly midcap oriented funds vary their exposure to small caps depending on the market conditions. Under normal circumstances their small cap exposure remains in the range of 20%- 30%. As per the latest portfolio disclosed on April 30, 2012, the top 10 stocks of small cap funds accounted for 35%-40% of their assets. The portfolios are not concentrated yet this doesn’t mean that the portfolios do not carry risk.

Small Cap Component of the Portfolio

(Portfolio details as on April 30, 2012 for all funds; AUM is disclosed on April 30, 2012 by all except Reliance Small Cap Fund IDFC Sterling Equity Fund and Religare Mid N Small Cap Fund which disclosed their AUM last on March 30, 2012) (Source: ACE MF; PersonalFN Research)

Risk Factors

In addition to the standard risk factors that all equity mutual fund investments are exposed to; small cap funds run some additional risks. More often, small cap funds invest in stocks that are not actively tracked by the analyst community. And even if tracked; the number of coverage reports is far lower than that for the blue chip or a popular mid cap stock. This is the reason why small cap stocks do not benefit upfront since the rally comes after a decent fall in these stocks. After all, investors wouldn’t prefer to invest in a company that is not widely tracked as it may or may not have a proven track record of good governance. Furthermore, smaller companies are more vulnerable to external shocks. Such companies may go under water if the crisis like situation persists for longer than anticipated. Small cap companies may not have the muscle to sustain losses for long or they may fall in total disarray if the revenue growth becomes flattish and they have a high debt to service ratio. Smaller companies often find it difficult to invest in research and development and they go completely out of flavour if the technology which made them successful becomes out dated. These risks are fundamental in nature and directly affect the return potential of your investments.

There are some technical factors too that make small caps riskier. If the liquidity is low, buying and selling small caps becomes difficult for the fund. For example, DSP BlackRock Micro Cap fund holds 2,12,666 shares of Kennametal India, a small cap company, as per the portfolio disclosed on April 30, 2012. It is listed only on Bombay Stock exchange. On an average 3,765 shares have been traded every day between April 30, 2012 and May 29, 2012. In other words, at the current average volume of traded shares, DSP BlackRock Micro Cap Fund will take about 56 days to offload Kennametal India completely. If it tries to sell its entire stake at one go, the price swings would be wild in case there’s no buyer at the current price or the fund will have to wait till the counter gains popularity and becomes liquid to absorb such heavy selling. Likewise, suppose if the fund was to buy 2,12,666 shares when the one month average volume is low; it would have to patiently wait and buy in small quantities or then would have to pay a lot higher price to buy 2,12,666 shares at one go. Kennametal India may or may not be a good investment but buying it in bulk would certainly cause price to move widely. If one tries to avoid stocks with low volumes, one may miss some really good stocks. Hence it becomes difficult for the fund manager to strike a balance between fundamental strengths of the company and technical difficulties in buying its common shares in large quantities.

Road Ahead

BSE Sensex has already fallen by more than 5% over last one month as the risk aversion has re-emerged in the market. European Sovereign debt crisis seems far from over and equity markets are moving back and forth with no real gains. No rally in Indian equities has sustained so far since the markets topped in November 2010. After the recent slide in the market, small caps may give you the feeling that they have become cheaper in valuation; they might have in deed, but that shouldn’t be the basis for investing in a pure small cap fund or a fund with a higher exposure to small caps.

Our view

Small caps and small cap mutual funds outperform the rest of the market when the economic outlook is robust and large caps and larger midcaps look expensive. At such a point if demand for risky assets such as equities is not quenched; small caps see sharp rallies as investors try to make quick bucks. Such furore often happens towards the end of a bull market. On the other hand, when the markets are nearing the bottom and small caps start looking cheap; chances are greater that they become even cheaper as the panic selling takes them to new lows. Small caps may remain completely out of flavour if markets fail to stabilize thereafter. At this juncture, when the extended bull rally in Indian equities looks difficult, it would be prudent to stay with large and multi cap funds.

Add Comments