(Image source: freepik.com)

(Image source: freepik.com)

Last Sunday, in a last ditch effort to keep up with my New Year resolution of being fit, I decided to go for a morning walk with my father expecting a quiet and peaceful conversation on literature, movies, literally anything but Finance.

But as luck would have it, we bumped into his friends, Mr Sharma and Mr Agarwal and unintentionally we ended up discussing the latest 'sure-shot-retire-rich' scheme that Mr Agarwal had come across.

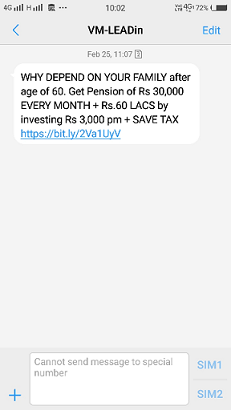

I was well aware of this scheme, because I get at least 2-3 messages every day from these 'well-wishers'. The message reads like this:

Now I must give credit where it's due. For a company whose objective is to target a simple salaried individual (with a lack of financial literacy) and ensure that he pays a meagre sum of Rs 3,000 monthly for the next 15-20 years, they are spot on with their marketing. Their sales strategy plays on the two most important psyche of a middleclass man, Fear and Greed.

First, by using the catchphrase like, 'Why depend on family?' they are activating his fear of loss of monetary freedom or independence. Then by assuring a decent pension plus a 60 Lakh corpus on retirement, they are feeding his greed.

[Read More: 8 Key Lessons On Financial Freedom From 'Rich Dad, Poor Dad]

These two powerful emotions can sway almost any individual, however financially literate and aware he/she might be.

Coming back to the morning walk, Mr Sharma excitedly exclaimed, 'This is an opportunity of a lifetime, imagine, paying Rs. 3000 per month for the next 31 years and getting a pay out of Rs 1.32 Crore! The money will grow 11 times! This simply cannot be missed'.

'I agree Sharma Ji, what do you think Mr. Khude, shall we invest in this scheme, after all its only Rs 3,000 per month?' Mr Agarwal enquired.

'I will ask my financial advisor' my father answered and turned to me.

'We know what Deepika will say, 'Papa, these schemes are bogus and are marketing traps for innocent investors like you, trust me, mutual funds are the best', said Mr Sharma mockingly.

I must admit, Mr Sharma correctly predicted my words and I couldn't help but laugh at his naivety.

But I had to show them the proof and out came by excel sheet (on my mobile phone) and the following calculation broke their hearts.

Let me show you the harsh truth behind a 'sure-shot-retire-rich-quickly' scheme.

Table 1: The hidden truth

| Age |

Years |

Cash Inflow |

Cash Outflow |

Net flow |

| 30 |

01/04/2019 |

- |

36,000 |

-36,000 |

| 31 |

01/04/2020 |

- |

36,000 |

-36,000 |

| 32 |

01/04/2021 |

- |

36,000 |

-36,000 |

| 33 |

01/04/2022 |

- |

36,000 |

-36,000 |

| 34 |

01/04/2023 |

- |

36,000 |

-36,000 |

| 35 |

01/04/2024 |

- |

36,000 |

-36,000 |

| 36 |

01/04/2025 |

- |

36,000 |

-36,000 |

| 37 |

01/04/2026 |

- |

36,000 |

-36,000 |

| 38 |

01/04/2027 |

- |

36,000 |

-36,000 |

| 39 |

01/04/2028 |

- |

36,000 |

-36,000 |

| 40 |

01/04/2029 |

- |

36,000 |

-36,000 |

| 41 |

01/04/2030 |

- |

36,000 |

-36,000 |

| 42 |

01/04/2031 |

- |

36,000 |

-36,000 |

| 43 |

01/04/2032 |

- |

36,000 |

-36,000 |

| 44 |

01/04/2033 |

- |

36,000 |

-36,000 |

| 45 |

01/04/2034 |

- |

36,000 |

-36,000 |

| 46 |

01/04/2035 |

- |

36,000 |

-36,000 |

| 47 |

01/04/2036 |

- |

36,000 |

-36,000 |

| 48 |

01/04/2037 |

- |

36,000 |

-36,000 |

| 49 |

01/04/2038 |

- |

36,000 |

-36,000 |

| 50 |

01/04/2039 |

- |

36,000 |

-36,000 |

| 51 |

01/04/2040 |

- |

36,000 |

-36,000 |

| 52 |

01/04/2041 |

- |

36,000 |

-36,000 |

| 53 |

01/04/2042 |

- |

36,000 |

-36,000 |

| 54 |

01/04/2043 |

- |

36,000 |

-36,000 |

| 55 |

01/04/2044 |

- |

36,000 |

-36,000 |

| 56 |

01/04/2045 |

- |

36,000 |

-36,000 |

| 57 |

01/04/2046 |

- |

36,000 |

-36,000 |

| 58 |

01/04/2047 |

- |

36,000 |

-36,000 |

| 59 |

01/04/2048 |

- |

36,000 |

-36,000 |

| 60 |

01/04/2049 |

- |

36,000 |

-36,000 |

| 61 |

01/04/2050 |

3,60,000 |

- |

3,60,000 |

| 62 |

01/04/2051 |

3,60,000 |

- |

3,60,000 |

| 63 |

01/04/2052 |

3,60,000 |

- |

3,60,000 |

| 64 |

01/04/2053 |

3,60,000 |

- |

3,60,000 |

| 65 |

01/04/2054 |

3,60,000 |

- |

3,60,000 |

| 66 |

01/04/2055 |

3,60,000 |

- |

3,60,000 |

| 67 |

01/04/2056 |

3,60,000 |

- |

3,60,000 |

| 68 |

01/04/2057 |

3,60,000 |

- |

3,60,000 |

| 69 |

01/04/2058 |

3,60,000 |

- |

3,60,000 |

| 70 |

01/04/2059 |

3,60,000 |

- |

3,60,000 |

| 71 |

01/04/2060 |

3,60,000 |

- |

3,60,000 |

| 72 |

01/04/2061 |

3,60,000 |

- |

3,60,000 |

| 73 |

01/04/2062 |

3,60,000 |

- |

3,60,000 |

| 74 |

01/04/2063 |

3,60,000 |

- |

3,60,000 |

| 75 |

01/04/2064 |

3,60,000 |

- |

3,60,000 |

| 76 |

01/04/2065 |

3,60,000 |

- |

3,60,000 |

| 77 |

01/04/2066 |

3,60,000 |

- |

3,60,000 |

| 78 |

01/04/2067 |

3,60,000 |

- |

3,60,000 |

| 79 |

01/04/2068 |

3,60,000 |

- |

3,60,000 |

| 80 |

01/04/2069 |

63,60,000 |

- |

63,60,000 |

| XIRR |

8.27% |

(For Illustration purpose only)

If an individual were to start investing Rs 3,000 per month from age 30 years till he is 60 years, as per the scheme he will start receiving a pension of Rs 30,000 per month till 80 years and at the end of 80 years, he will end up with an additional corpus of Rs 60 Lakhs. To a naive investor, this means a return of 11% every year, but in reality the return is 8.27%!

Needless to say, Mr Sharma and Mr Agarwal looked shocked and a bit betrayed. Their hopes for a return of 11% went down the drain.

'Only 8.27%?' enquired Mr Sharma, 'but I pay Rs 11 Lakh and get Rs 1.32 Crore!' are you saying that this is just 8.27% return?' he enquired.

'Yes', I replied.

'Wow, I'm glad we met, otherwise, I was going to subscribe to the scheme tomorrow morning. It was on my agenda', remarked Mr Sharma.

'Well, you should always be questioning each and every investment opportunity. Like if you would have looked closely at the message, you would have noticed that you can't call back on the number, the message itself says, that you cannot send message to special number! Did you not wonder why the special number? Also, if you open the link, it specifically states that only people within 30-45 years age group can invest. The linked website looks gimmicky at best. No details, no about us, no past, nothing. 'The website (if we can call it that) is superficial and a trap at best', I explained.

'So, we need to let go of our dream of creating wealth and a huge corpus?' enquired Mr Agarwal grimly.

[Read More: Step-By-Step Approach To Retirement Planning]

'No', I replied. 'You don't have to give up on your dreams of retiring rich, neither do you have to be a 100% invested in equities, if you aren't comfortable', I continued.

The returns that the scheme guaranteed can be achieved in reality without using equities also. Let me show you...

Table 2: Creating a corpus with 100% Debt

| Age |

Cash Inflow |

Cash Outflow |

Net flow |

Corpus |

Withdrawal |

Balance Corpus |

| 30 |

- |

36,000 |

-36,000 |

37,701 |

- |

37,701 |

| 31 |

- |

36,000 |

-36,000 |

78,735 |

- |

78,735 |

| 32 |

- |

36,000 |

-36,000 |

1,23,396 |

- |

1,23,396 |

| 33 |

- |

36,000 |

-36,000 |

1,72,004 |

- |

1,72,004 |

| 34 |

- |

36,000 |

-36,000 |

2,24,909 |

- |

2,24,909 |

| 35 |

- |

36,000 |

-36,000 |

2,82,490 |

- |

2,82,490 |

| 36 |

- |

36,000 |

-36,000 |

3,45,161 |

- |

3,45,161 |

| 37 |

- |

36,000 |

-36,000 |

4,13,372 |

- |

4,13,372 |

| 38 |

- |

36,000 |

-36,000 |

4,87,611 |

- |

4,87,611 |

| 39 |

- |

36,000 |

-36,000 |

5,68,413 |

- |

5,68,413 |

| 40 |

- |

36,000 |

-36,000 |

6,56,357 |

- |

6,56,357 |

| 41 |

- |

36,000 |

-36,000 |

7,52,074 |

- |

7,52,074 |

| 42 |

- |

36,000 |

-36,000 |

8,56,252 |

- |

8,56,252 |

| 43 |

- |

36,000 |

-36,000 |

9,69,638 |

- |

9,69,638 |

| 44 |

- |

36,000 |

-36,000 |

10,93,047 |

- |

10,93,047 |

| 45 |

- |

36,000 |

-36,000 |

12,27,364 |

- |

12,27,364 |

| 46 |

- |

36,000 |

-36,000 |

13,73,553 |

- |

13,73,553 |

| 47 |

- |

36,000 |

-36,000 |

15,32,664 |

- |

15,32,664 |

| 48 |

- |

36,000 |

-36,000 |

17,05,839 |

- |

17,05,839 |

| 49 |

- |

36,000 |

-36,000 |

18,94,321 |

- |

18,94,321 |

| 50 |

- |

36,000 |

-36,000 |

20,99,463 |

- |

20,99,463 |

| 51 |

- |

36,000 |

-36,000 |

23,22,737 |

- |

23,22,737 |

| 52 |

- |

36,000 |

-36,000 |

25,65,748 |

- |

25,65,748 |

| 53 |

- |

36,000 |

-36,000 |

28,30,238 |

- |

28,30,238 |

| 54 |

- |

36,000 |

-36,000 |

31,18,106 |

- |

31,18,106 |

| 55 |

- |

36,000 |

-36,000 |

34,31,420 |

- |

34,31,420 |

| 56 |

- |

36,000 |

-36,000 |

37,72,427 |

- |

37,72,427 |

| 57 |

- |

36,000 |

-36,000 |

41,43,577 |

- |

41,43,577 |

| 58 |

- |

36,000 |

-36,000 |

45,47,533 |

- |

45,47,533 |

| 59 |

- |

36,000 |

-36,000 |

49,87,195 |

- |

49,87,195 |

| 60 |

- |

36,000 |

-36,000 |

54,65,719 |

- |

54,65,719 |

| 61 |

3,60,000 |

- |

3,60,000 |

59,30,305 |

3,60,000 |

55,70,305 |

| 62 |

3,60,000 |

- |

3,60,000 |

60,43,781 |

3,60,000 |

56,83,781 |

| 63 |

3,60,000 |

- |

3,60,000 |

61,66,902 |

3,60,000 |

58,06,902 |

| 64 |

3,60,000 |

- |

3,60,000 |

63,00,489 |

3,60,000 |

59,40,489 |

| 65 |

3,60,000 |

- |

3,60,000 |

64,45,430 |

3,60,000 |

60,85,430 |

| 66 |

3,60,000 |

- |

3,60,000 |

66,02,692 |

3,60,000 |

62,42,692 |

| 67 |

3,60,000 |

- |

3,60,000 |

67,73,320 |

3,60,000 |

64,13,320 |

| 68 |

3,60,000 |

- |

3,60,000 |

69,58,453 |

3,60,000 |

65,98,453 |

| 69 |

3,60,000 |

- |

3,60,000 |

71,59,321 |

3,60,000 |

67,99,321 |

| 70 |

3,60,000 |

- |

3,60,000 |

73,77,264 |

3,60,000 |

70,17,264 |

| 71 |

3,60,000 |

- |

3,60,000 |

76,13,731 |

3,60,000 |

72,53,731 |

| 72 |

3,60,000 |

- |

3,60,000 |

78,70,298 |

3,60,000 |

75,10,298 |

| 73 |

3,60,000 |

- |

3,60,000 |

81,48,673 |

3,60,000 |

77,88,673 |

| 74 |

3,60,000 |

- |

3,60,000 |

84,50,711 |

3,60,000 |

80,90,711 |

| 75 |

3,60,000 |

- |

3,60,000 |

87,78,421 |

3,60,000 |

84,18,421 |

| 76 |

3,60,000 |

- |

3,60,000 |

91,33,987 |

3,60,000 |

87,73,987 |

| 77 |

3,60,000 |

- |

3,60,000 |

95,19,776 |

3,60,000 |

91,59,776 |

| 78 |

3,60,000 |

- |

3,60,000 |

99,38,357 |

3,60,000 |

95,78,357 |

| 79 |

3,60,000 |

- |

3,60,000 |

103,92,517 |

3,60,000 |

100,32,517 |

| 80 |

63,60,000 |

- |

63,60,000 |

108,85,281 |

63,60,000 |

45,25,281 |

(For Illustration purpose only)

'As you can see from the above table, if you invest in a PPF/EPF/VPF fetching you around 8.5% per annum, you can earn a corpus of Rs 1.08 crore on the same investment, without taking any market risk! This money will be kept with your government backed company (my father and his friends work in a government undertaking), so zero chance of fraud' I explained.

'What happens if we split this between equity and PPF?', my father asked with a twinkle of greed in his eyes.

'Well, then you become super-rich, here's how...

Table 3: Creating a corpus with 50% - Equity & 50% - Debt allocation

| Age |

Investment in MF |

Investment in PPF |

Total Corpus |

Withdrawal |

Balance Corpus |

Corpus - Equity |

Corpus - PPF |

| 30 |

18,000 |

18,000 |

38,013 |

- |

38,013 |

19,214 |

18,799 |

| 31 |

18,000 |

18,000 |

80,024 |

- |

80,024 |

40,865 |

39,159 |

| 32 |

18,000 |

18,000 |

1,26,470 |

- |

1,26,470 |

65,261 |

61,209 |

| 33 |

18,000 |

18,000 |

1,77,841 |

- |

1,77,841 |

92,752 |

85,088 |

| 34 |

18,000 |

18,000 |

2,34,680 |

- |

2,34,680 |

1,23,730 |

1,10,950 |

| 35 |

18,000 |

18,000 |

2,97,594 |

- |

2,97,594 |

1,58,636 |

1,38,958 |

| 36 |

18,000 |

18,000 |

3,67,260 |

- |

3,67,260 |

1,97,968 |

1,69,291 |

| 37 |

18,000 |

18,000 |

4,44,431 |

- |

4,44,431 |

2,42,290 |

2,02,142 |

| 38 |

18,000 |

18,000 |

5,29,951 |

- |

5,29,951 |

2,92,232 |

2,37,719 |

| 39 |

18,000 |

18,000 |

6,24,757 |

- |

6,24,757 |

3,48,509 |

2,76,249 |

| 40 |

18,000 |

18,000 |

7,29,899 |

- |

7,29,899 |

4,11,922 |

3,17,976 |

| 41 |

18,000 |

18,000 |

8,46,546 |

- |

8,46,546 |

4,83,378 |

3,63,168 |

| 42 |

18,000 |

18,000 |

9,76,007 |

- |

9,76,007 |

5,63,897 |

4,12,110 |

| 43 |

18,000 |

18,000 |

11,19,741 |

- |

11,19,741 |

6,54,627 |

4,65,114 |

| 44 |

18,000 |

18,000 |

12,79,382 |

- |

12,79,382 |

7,56,864 |

5,22,518 |

| 45 |

18,000 |

18,000 |

14,56,753 |

- |

14,56,753 |

8,72,067 |

5,84,686 |

| 46 |

18,000 |

18,000 |

16,53,895 |

- |

16,53,895 |

10,01,881 |

6,52,014 |

| 47 |

18,000 |

18,000 |

18,73,089 |

- |

18,73,089 |

11,48,159 |

7,24,930 |

| 48 |

18,000 |

18,000 |

21,16,886 |

- |

21,16,886 |

13,12,988 |

8,03,898 |

| 49 |

18,000 |

18,000 |

23,88,143 |

- |

23,88,143 |

14,98,722 |

8,89,421 |

| 50 |

18,000 |

18,000 |

26,90,053 |

- |

26,90,053 |

17,08,011 |

9,82,042 |

| 51 |

18,000 |

18,000 |

30,26,194 |

- |

30,26,194 |

19,43,844 |

10,82,350 |

| 52 |

18,000 |

18,000 |

34,00,570 |

- |

34,00,570 |

22,09,586 |

11,90,984 |

| 53 |

18,000 |

18,000 |

38,17,665 |

- |

38,17,665 |

25,09,031 |

13,08,634 |

| 54 |

18,000 |

18,000 |

42,82,502 |

- |

42,82,502 |

28,46,453 |

14,36,050 |

| 55 |

18,000 |

18,000 |

48,00,709 |

- |

48,00,709 |

32,26,668 |

15,74,041 |

| 56 |

18,000 |

18,000 |

53,78,589 |

- |

53,78,589 |

36,55,104 |

17,23,485 |

| 57 |

18,000 |

18,000 |

60,23,209 |

- |

60,23,209 |

41,37,877 |

18,85,332 |

| 58 |

18,000 |

18,000 |

67,42,491 |

- |

67,42,491 |

46,81,877 |

20,60,613 |

| 59 |

18,000 |

18,000 |

75,45,313 |

- |

75,45,313 |

52,94,871 |

22,50,443 |

| 60 |

18,000 |

18,000 |

84,41,635 |

- |

84,41,635 |

59,85,607 |

24,56,028 |

| 61 |

- |

- |

|

3,60,000 |

84,41,635 |

65,02,280 |

24,58,110 |

| 62 |

- |

- |

|

3,60,000 |

109,20,366 |

70,80,953 |

24,60,359 |

| 63 |

- |

- |

|

3,60,000 |

117,36,194 |

77,29,068 |

24,62,788 |

| 64 |

- |

- |

|

3,60,000 |

126,49,807 |

84,54,956 |

24,65,411 |

| 65 |

- |

- |

|

3,60,000 |

136,72,932 |

92,67,950 |

24,68,243 |

| 66 |

- |

- |

|

3,60,000 |

148,18,699 |

101,78,504 |

24,71,303 |

| 67 |

- |

- |

|

3,60,000 |

161,01,816 |

111,98,325 |

24,74,607 |

| 68 |

- |

- |

|

3,60,000 |

175,38,753 |

123,40,524 |

24,78,176 |

| 69 |

- |

- |

|

3,60,000 |

191,47,956 |

136,19,787 |

24,82,030 |

| 70 |

- |

- |

|

3,60,000 |

209,50,083 |

150,52,561 |

24,86,192 |

| 71 |

- |

- |

|

3,60,000 |

229,68,271 |

166,57,268 |

24,90,687 |

| 72 |

- |

- |

|

3,60,000 |

252,28,432 |

184,54,541 |

24,95,542 |

| 73 |

- |

- |

|

3,60,000 |

277,59,586 |

204,67,486 |

25,00,786 |

| 74 |

- |

- |

|

3,60,000 |

305,94,234 |

227,21,984 |

25,06,449 |

| 75 |

- |

- |

|

3,60,000 |

337,68,776 |

252,47,022 |

25,12,565 |

| 76 |

- |

- |

|

3,60,000 |

373,23,976 |

280,75,064 |

25,19,170 |

| 77 |

- |

- |

|

3,60,000 |

413,05,493 |

312,42,472 |

25,26,303 |

| 78 |

- |

- |

|

3,60,000 |

109,20,366 |

347,89,969 |

25,34,008 |

| 79 |

- |

- |

|

3,60,000 |

117,36,194 |

387,63,165 |

25,42,328 |

| 80 |

- |

- |

|

63,60,000 |

126,49,807 |

362,91,545 |

25,51,314 |

| Total Additional Corpus at 80 years |

388,42,859 |

|

|

(For Illustration purpose only)

'By following a conservative approach of 50% Equity and 50% debt, you can take home a pension of Rs 30,000 per month plus Rs 60 lakh as additional corpus plus a whopping Rs 3.88 Crore!' I explained to my father and his friends.

'So, it is possible for anyone to grow and retire rich?' Mr Sharma asked this time with no sarcasm and sans the usual mocking.

'Yes, all you need is a strategy and an honest financial planner. When it comes to creating a corpus of crores, honest advisors should be at the helm of the plan and strategy', I remarked.

As we concluded the discussion, we all simultaneously received a message which read, 'Why Depend on your family at the age of 60....', and we all broke out laughing loudly. As they say, 'Fool me once, shame on you, Fool me twice, shame on me'.

If you too are thinking about falling into such marketing mails and traps and wish to have an honest wealth manager that takes into account your ideology with wealth and shares your vision, look no further and connect with PersonalFN's Certified Financial Guardian on 022-61361200 or write to info@personalfn.com. You may also fill in this form, and soon our experienced financial planners will reach out to you.

PS: If you're unsure where to invest fresh investible surplus currently, and you're looking for "high investment gains at relatively moderate risk" this ready-made portfolio would be suitable for you.

In this 2019 Edition of PersonalFN's Premium Report, "The Strategic Funds Portfolio For 2025", you will get a ready-made portfolio of its top equity mutual funds schemes for 2025 that have the ability to generate lucrative returns over the long term.

PersonalFN's "The Strategic Funds Portfolio for 2025" is geared to potentially multiply your wealth in the years to come. Subscribe now!

Till then, Happy Investing!

Add Comments