It was a tough two years for the bond market.

While one expects bond markets to be stable, the past two years have been nothing like it.

Easing inflation, rate cuts, demonetisation, excess liquidity, India rating upgrade, rising crude oil prices, volatile rupee, uptick in inflation, broadening fiscal deficit and now fears of an interest rate hike summarise a few of the major events that have influenced the bond market over the past 24 months.

Let us take a brief look at how interest rates and bond yields fared over this period.

Two years ago, in February 2016, the 10-year G-Sec yield stood around 7.8%. Bond traders were expecting interest rates to moderate further, giving the Reserve Bank of India (RBI) more room to cut interest rates.

In 2015, the RBI had already reduced interest rates by 125 basis points on easing inflation and stagnant growth. For corporate bonds, the deterioration in credit quality was a growing concern.

As expected, over the course of the year, the monetary policy committee of the RBI cut the benchmark repo rate twice, totalling 50 bps to 6.25% as in October 2016. The bond market reacted positively and bond yields dropped. The yield of the 10-year G-Sec , which was hovering around the 7.8% at the start of the year, eased by 100 bps to around 6.8% in October 2016.

10-year Benchmark G-Sec Yield – On a Decline

Data as on January 31, 2017

(Source: investing.com, PersonalFN Research)

But the market was not prepared for demonetisation that was announced on November 8, 2016. The ban on the old Rs 500 and Rs 1,000 notes led to a deluge of liquidity in the system, as Indian citizens rushed to deposit their defunct currency notes in banks. This led the 10-year G-Sec benchmark yield to drop to their lowest point of 6.19% in the past seven years.

The RBI then jumped in to squeeze out the liquidity by selling bonds under the Market Stabilisation Scheme (MSS) to banks on behalf of the government. Although the MSS is an existing programme, the limit was earlier only Rs 30,000 crore, which was hiked to Rs 6 lakh crore to deal with the deluge of cash with banks.

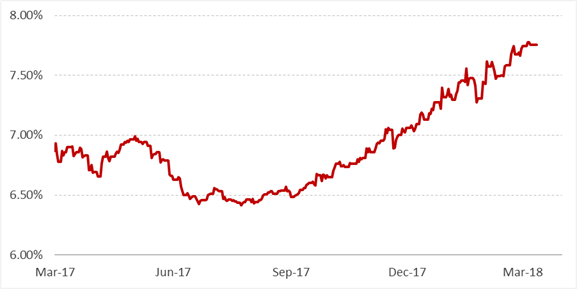

A Steep Rise In The Benchmark Yield Over Past Few Months

Data as on March 9, 2018

(Source: investing.com, PersonalFN Research)

Given this move of the RBI, the benchmark yield jumped to near 7% by the end of February 2017.

From the March 2017 onwards, easing inflation brought a cheer to bond investors. Retail inflation as measured by the combined Consumer Price Index (CPI) had dropped to under 4%. Inflation eased further to 1.46% in June 2017. This increased the hopes of a rate cut. The benchmark yield dropped to around 6.5% in July 2017.

As expected, in August 2017, the RBI reduced the repo rate to 6%. The market had already factored in this rate cut, hence, the bond traders were reactionless when the decision was announced. The benchmark yield continued to hover near the 6.5%.

Bond traders were focussed on something more threatening that was brewing in the global markets. Crude oil price was steadily inching up from its lows of $45/barrel in June 2017. This would not only lead to higher inflation, but the cash bonanza the government was enjoying over the past couple of years, was shrinking. This feared the risk that the government will breach its fiscal deficit target.

By the end of October 2017, crude oil price was at its highest in two years. In retaliation, the 10-year G-Sec yield shot up from 6.5% to 7% by mid-November 2017.

By the end of January 2018, crude oil price breached the $60 mark to its highest in 39 months. Inflation was back over the 5% mark in December 2017 and January 2018. Not surprisingly, the 10-year benchmark yield soon breached the 7.5% mark.

With the risks refusing to abate, as on March 2018, the benchmark yield breached the 7.8% mark, back to the level it started at in February 2016.

To deal with debt market volatility, fund houses and distributors often promote Dynamic Bond Funds.

If you are new to debt funds, watch this short video to know more—

What are Debt Funds?

What are Dynamic Bond Funds?

Dynamic Bond Funds are a category of debt funds that offer the flexibility to invest in papers with various maturity profiles. These funds will have a flexibility to adjust the duration of the portfolio to benefit from the possible change in the interest rate structure.

Such funds can invest in a mix of short-term as well as long-term debt instruments. They emphasize on generating attractive returns in the long term by riding the entire interest rate cycle.

Dynamic bond schemes move into short-term instruments, such as commercial paper (CP) and certificates of deposit (CDs), or long-term instruments, such as corporate bonds and gilt securities, depending on their outlook on interest rates. They decide on which type of short-term or long-term debt instrument to invest—depending on their view of where the interest rates are headed.

However, predicting the direction for interest rates is extremely difficult even for the most trained investor.

[Also read: 5 Facets To Look Into While Investing In Debt Mutual Funds]

Did the flexibility given to Dynamic Bond fund managers result in superior returns for investors? Let’s take a look.

How Dynamic Bond Funds fared over the past two years

The results are mixed. A handful of schemes were able to deliver a return in the range of 9%-10% compounded over the 2-year period ended March 9, 2018. Over the same period, the CRISIL Composite Bond Fund Index generated a return of 7.89%, while the CRISIL Short Term Index delivered 7.64%. Astonishingly, the bottom set of dynamic bond schemes delivered a return under 7%.

Point-to-point Return of Dynamic Bond Schemes Over Past Two Years

| Scheme Name |

9/Mar/16 To 9/Mar/18 |

| ICICI Pru Long Term Plan |

10.80 |

| Franklin India Dynamic Accrual Fund |

9.92 |

| Quantum Dynamic Bond Fund-Direct Plan |

9.56 |

| UTI Dynamic Bond Fund |

9.04 |

| Kotak Flexi Debt Fund |

9.03 |

| SBI Dynamic Bond |

8.62 |

| DHFL Pramerica Dynamic Bond Fund |

8.55 |

| Baroda Pioneer Dynamic Bond Fund |

8.49 |

| ICICI Pru Dynamic Bond Fund |

8.24 |

| Canara Rob Dynamic Bond Fund |

8.16 |

| HDFC High Interest Fund-Dynamic Plan |

8.01 |

| Axis Dynamic Bond Fund |

8.00 |

| Principal Dynamic Bond Fund |

7.67 |

| Reliance Dynamic Bond |

7.57 |

| IDFC Dynamic Bond Fund |

7.54 |

| Tata Dynamic Bond Fund |

7.44 |

| Aditya Birla SL Dynamic Bond Fund |

7.08 |

| IIFL Dynamic Bond Fund |

6.97 |

| Union Dynamic Bond |

5.80 |

| Edelweiss Dynamic Bond Fund |

5.53 |

| IDBI Dynamic Bond |

4.40 |

| Taurus Dynamic Income Fund |

0.66 |

Data as on March 9, 2018

(Source: ACE MF, PersonalFN Research)

As seen in the table above, schemes such as ICICI Prudential Long Term Plan, Franklin India Dynamic Accrual Fund, Quantum Dynamic Bond Fund, UTI Dynamic Bond Fund and Kotak Flexi Debt Fund topped the list with returns like 10.80%, 9.92%, 9.56%, 9.03%, and 9.02%.

At the bottom of the list were schemes such as IIFL Dynamic Bond Fund, Union Dynamic Bond, Edelweiss Dynamic Bond Fund, IDBI Dynamic Bond and Taurus Dynamic Income Fund.

In comparison to the benchmarks, the performance of the top schemes has been commendable. However, when compared to long-term income funds, there is not much difference in performance.

Had you invested in a top long-term income scheme, your returns would have been in line with the top dynamic funds.

This is mainly because dynamic bond funds picked securities with a longer maturity with the expectations that interest rates would decline. While this worked in initially when yields were declining, they were unprepared when the direction of the bond market moved the other way.

Breaking Up the Performance Of Dynamic Bond Funds Over The Past Two Years

| Scheme Name |

When Yields Declined -

9/Mar/16 To 9/Dec/16 |

When Yields Moved Up -

9/Dec/16 To 9/Mar/18 |

| ICICI Pru Long Term Plan |

16.66 |

4.14 |

| HDFC High Interest Fund-Dynamic Plan |

15.73 |

0.61 |

| Aditya Birla SL Dynamic Bond Fund |

15.32 |

-0.49 |

| Quantum Dynamic Bond Fund-Direct Plan |

15.18 |

3.33 |

| Canara Rob Dynamic Bond Fund |

14.83 |

1.48 |

| SBI Dynamic Bond |

14.70 |

2.25 |

| UTI Dynamic Bond Fund |

14.68 |

2.90 |

| Reliance Dynamic Bond |

14.08 |

1.12 |

| DHFL Pramerica Dynamic Bond Fund |

13.53 |

2.99 |

| Axis Dynamic Bond Fund |

13.40 |

2.25 |

| ICICI Pru Dynamic Bond Fund |

12.70 |

3.13 |

| Baroda Pioneer Dynamic Bond Fund |

12.65 |

3.54 |

| Principal Dynamic Bond Fund |

12.57 |

2.36 |

| IDFC Dynamic Bond Fund |

12.55 |

2.16 |

| Kotak Flexi Debt Fund |

12.46 |

4.51 |

| Union Dynamic Bond |

11.92 |

-0.01 |

| Tata Dynamic Bond Fund |

11.85 |

2.53 |

| IDBI Dynamic Bond |

11.17 |

-1.59 |

| Franklin India Dynamic Accrual Fund |

9.55 |

8.14 |

| Edelweiss Dynamic Bond Fund |

8.91 |

1.79 |

| IIFL Dynamic Bond Fund |

5.78 |

6.48 |

| Taurus Dynamic Income Fund |

5.20 |

-2.97 |

Data as on March 9, 2018

(Source: ACE MF, PersonalFN Research)

When interest rates were lowered and yields declined between March 2016 to December 2016, top dynamic funds generated a return in excess of 15% absolute. However, when the debt market turned on its head, the same bond funds were caught struggling between December 2016 and March 2018. Most of the funds delivered a return under 5% compounded. Some dynamic schemes even delivered negative returns.

Similar was the case with long-term income funds. However, schemes that maintained a low maturity profile were able to do better than other funds.

Additional Reads:

Bank FDs vs. Debt Mutual Funds: Which is better?

How You Should Structure Your Debt Fund Portfolio

How Will 2018 Be For Investors In Debt Mutual Funds And Fixed Deposits

To conclude…

If you thought investing in debt funds was not risky, think again. Though the volatility may not be as high as in the equity market, there are still chances of you losing money. This is a dreaded situation, no investor wishes to experience. In dynamic bond funds, if interest rates move in the direction opposite to the expectations of the fund manager’s , it can lead to serious losses for the investor.

Hence, as an investor, you need to pick the right debt fund in-line with your financial goals.

Going forward, if RBI increases policy rates by any chance and if inflation continues to trend up, it could be perilous for your investments in debt funds with a long maturity profile.

Hence, it would be better if you deploy your hard earned money in short-term debt funds if you’re risk averse, but ensure you’re giving due consideration to your investment time horizon.

For an investment horizon of around 2-3 years, consider investing in short-term debt funds.

If you have an investment horizon of 3 to 6 months, ultra-short term funds (also known as liquid plus funds) would be the most suitable.

And if you have an extreme short-term time horizon (of less than 3 months) you would be better-off investing in liquid funds.

|

Editor’s Note:

Prudent investing and financial discipline are vital ingredients to long-term financial well-being.

If you need research-backed recommendations to select the best debt mutual fund schemes for your portfolio, you can access 7 high-performing, time-tested readymade portfolios with a decade-long market-beating track record. PersonalFN’s model mutual fund portfolio service ‘FundSelect Plus’ has completed a decade and we are offering subscriptions at a massive 75% discount!

Apart from four equity-oriented portfolios, you get access to three readymade debt mutual portfolios. The debt portfolios have been formulated using the investment tenure as the cornerstone. Depending on your investment horizon, which could be anywhere from less than 3 months, 3-12 months, or more than 12 months, you can choose the portfolio of your choice.

PersonalFN’s track record speaks for itself, as all three portfolio have comfortably overachieved their respective benchmarks. Don’t miss out on special offers. Subscribe now!

|

DISCLOSURE AS PER SECURITIES AND EXCHANGE BOARD OF INDIA (RESEARCH ANALYSTS) REGULATIONS, 2014

About the Company including business activity

Quantum Information Services Private Limited (QIS) was incorporated on December 19, 1989.

QIS was promoted by Mr. Ajit Dayal with an objective of providing value-based information / views on news related to equity markets, the economy in general, sector analysis, budget review and various personal products and investments options available to the Public. It was the first company to start equity research on an institutional level.

'PersonalFN' is a service brand of QIS and was started in the year 1999. In 1999, the Company registered the Domain name www.personalfn.com for providing information on mutual funds and personal financial planning, financial markets in general, etc and services related to financial planning and research in various financial instruments including mutual funds, insurance and fixed income products to customers. It offers asset allocation and researched investment recommendations through its financial planning services.

Quantum Information Services Private Limited (QIS) is registered as Investment Adviser under SEBI (Investment Adviser) Regulations, 2013 and having Registration No.: INA000000680. In terms of second proviso to Regulation 3 (1) of SEBI (Research Analysts) Regulations, 2014 the Company is not required to obtain Certificate of registration from SEBI.

Disciplinary history

There are no outstanding litigations against the Company, it subsidiaries and its Directors.

and condition on which its offer research report. For the terms and condition for research report click here.

Details of associates

- Money Simplified Services Private Limited;

- PersonalFN Insurance Services Private Limited ;

- Equitymaster Agora Research Private Limited;

- Common Sense Living Private Limited;

- Quantum Advisors Private Limited;

- Quantum Asset Management Company Private Limited;

- HelpYourNGO Private Limited;

- HelpYourNGO Foundation;

- Natural Streets for Performing Arts Foundation;

- Primary Real Estate Advisors Private Limited;

- Rahul Goel;

- I V Subramaniam.

Disclosure with regard to ownership and material conflicts of interest

- Neither QIS, it’s Associates, Research Analyst or his/her relative have any financial interest in the subject Company , except QIS receives fees for providing research to Quantum Equity Fund of Fund (QEFoF) which is Fund of Fund scheme managed by QMF.

- Neither QIS, it's Associates, Research Analyst or his/her relative have actual/beneficial ownership of one per cent or more securities of the subject Company, at the end of the month immediately preceding the date of publication of the research report.

- Neither QIS, it's Associates, Research Analyst or his/her relative has any other material conflict of interest at the time of publication of the research report except that QIS (PersonalFN) is, as per SEBI (Mutual Funds) Regulations 1996, an associate / group Company of Quantum Asset Management Company Private Limited and Trustees and Sponsor of Quantum Mutual Fund (QMF) and to that extent there may be conflict of interest while recommending any schemes of QMF. However any such recommendation or reference made is based on the standard evaluation and selection process, which applies uniformly for all Mutual Fund Schemes. The payment of commission (upfront /annualized & trail), if any, for any Schemes by QMF to QIS (PersonalFN) is also at arm's length and as per prevailing market practices

Disclosure with regard to receipt of Compensation

- Neither QIS nor it's Associates have any compensation from the subject Company in the past twelve months.

- Neither QIS nor it's Associates have managed or co-managed public offering of securities for the subject Company in the past twelve months.

- Neither QIS nor it's Associates have received any compensation for investment banking or merchant banking or brokerage services from the subject Company in the past twelve months.

- Neither QIS nor it’s Associates have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months except from Axis Bank Limited under a service agreement.

- Neither QIS nor it's Associates have received any compensation or other benefits from the subject Company or third party in connection with the research report

General disclosure

- The Research Analyst has not served as an officer, director or employee of the subject Company.

- QIS or the Research Analyst has not been engaged in market making activity for the subject Company.

Subject Company means Mutual Fund Schemes

Quantum Information Services Private Limited CIN: U65990MH1989PTC054667 Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222

SEBI-registered Investment Adviser. Registration No. INA000000680, SEBI (Investment Advisers) Regulation, 2013

Add Comments