(Image source: Background vector created by dooder via www.freepik.com)

(Image source: Background vector created by dooder via www.freepik.com)

Graded exit load imposed on liquid funds might turn out to be a game changer. Moreover, as per the new rules, liquid funds now have to hold at least 20% of their assets in highly liquid assets such as cash, government securities, and repo.

The comments of the Mahendra Kumar Jajoo, Head of Fixed Income at Mirae India Asset Mutual Fund, suggested that the industry isn't ready for this shock. "The seven-day exit load will impair the competitive advantage of liquid funds against bank FDs", opined Mr Jajoo.

It's noteworthy that around 1/5th of industry's AUM lies with liquid funds; and according to media reports nearly 30% of money flowing into liquid funds moves out within the first seven days.

Is SEBI overregulating?

No! In fact, mutual funds have shot themselves in the foot.

[Read: How SEBI's New Norms For Debt Mutual Funds Make a High Impact ]

Here's the background...

The capital market regulator gave fund houses multiple opportunities to correct their modus operandi. It expected them to observe stricter self-regulatory processes. Unfortunately, mutual fund houses seem to have taken the market regulator for granted.

Post the IL&FS, DHFL, Reliance ADAG, and Essel Group debt episodes, SEBI moved swiftly in making the mutual fund industry more accountable for their actions. And left with no other choice, SEBI took a stern stance on the risk management processes followed by mutual funds, and rightly so. After all, protecting investors' interest is one of its topmost priorities.

Whether or not it's a wise idea isn't really the question.

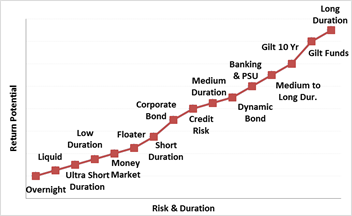

Graph: Risk-return trade off-debt schemes...

For illustration purpose only

Overnight funds is a category of debt scheme emerged after the SEBI's recategorization norms.

As per the SEBI's circular dated October 06, 2017, overnight funds are open-ended debt schemes investing in overnight securities with a maturity of one day. They are typically money market instruments, viz. Treasury bill (T-Bills) and Collateralised Borrowing and Lending Obligations (CBLOs).

In comparison, liquid funds, by the regulator's definition, are supposed to invest in debt and money market instrument papers with a maturity profile of up to 91 days. The investment basket of liquid funds is quite diverse. So they invest in a variety of instruments such as Certificate of Deposits (CDs) and Commercial Papers (CPs), which also carry higher risk as compared to other overnight instruments.

Hence, the primary difference is investment preferences based on the maturity profile of the type of credit instrument.

The return potential of an overnight fund is typically compared to the prevailing interest rates in the overnight markets. In other words, they might generate returns in line with the repo rates and inter-bank lending rates in the overnight market, under normal conditions.

Thus, even after SEBI's new rules were applicable for liquid funds, their return potential is still better than that of overnight funds, at least on the paper. If the future returns fail to increase 1.0% to 2.5% higher than those of overnight funds, liquid funds may soon become unpopular. Liquidity conditions and credit environment may dominate the investor preferences.

Nonetheless if money, which is otherwise parked in liquid funds, finds its way in FDs, capital cost of banks might go down because Current Account and Savings Account (CASA) is the cheapest source of funding for them. As a result, the Net Interest Margin (NIM) of banks may improve. In the past, banks have faced intense competition by Small Savings Schemes and mutual funds.

As you might be aware, Mutual Fund schemes are mandated to invest only in listed NCDs and this would be implemented in a phased manner. All fresh investments in Commercial Papers (CPs) shall be made only in listed CPs pursuant to issuance of SEBI's guidelines in this regard.

This rule might push corporates to switch to banks to satisfy their short-term credit requirements as listing of NCDs will involve additional costs, which may not be feasible for short-tenure credit instruments.

As far as retail investors are concerned, liquid funds might still remain popular with investors opting for Systematic Transfer Plan (STP); but with institutional investors they might have started falling out of favour already.

This article first appeared on Certified Financial Guardian.

Add Comments