|

| November 18, 2016 |

| |

| |

Impact

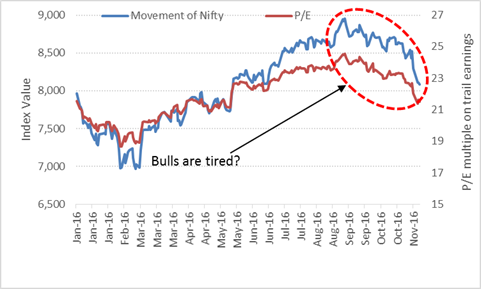

Mr. Donald Trump and Demonetisation are proving to be a double whammy for the Indian markets these days. The President-elect has bowled a bouncer that investors haven't managed to duck. On the other hand, ripple effects of Demonetisation have proved potent enough to create anxiety among investors. No wonder then, Indian stock markets. All of a sudden, have fallen off a cliff. Since their September highs, equity indices have lost approximately 10%. Individual names have seen even bigger cuts.

Dalal Street was expecting Indian corporates to report encouraging numbers in Q2, FY 2016-17. And the exit polls on U.S. Presidential elections were hinting at a comfortable victory for Mrs. Hilary Clinton.

Unfortunately, both these premises went wrong, and at 8,952 feet above ground, Nifty realised that it was running short of fuel for the next upmove. What's more, investors were left with an empty bag in place of a parachute. The result was evident—crash!

Bull phase correction or the beginning of a bear phase?

Data as on November 17, 2016

(Source: NSE,PersonalFN Research)

Emerging equity markets have been under pressure ever since Mr Trump has won the elections. US$ has been appreciating against emerging market currencies, and Foreign Institutional Investors (FIIs) have been taking out money from weaker markets. India has been one of them. The timing of Demonetisation couldn't have been worse than this. Indian markets seem to have entered a protracted lull phase.

Let's understand where we are heading from here onwards...

- As the cash is scarce at the moment, consumers are likely to postpone their buying decisions, and may pick up only things that are absolutely essential.

- Many small and medium scale enterprises that depend heavily on their cash sales to fuel their working capital requirements have been facing a severe cash crunch. Restrictions on withdrawals from the current account are making it difficult to run their business efficiently.

- In the pre-demonetisation phase, many industries were operating at sub-optimum production levels. Ongoing slack in demand has further delayed a much-awaited recovery in the capex cycle.

- As a result of above factors, companies depending on consumers' discretionary income have been hit hard. Along with them, those in real estate, and Non-Banking Financial Institutions (NBFCs) have performed terribly.

- Moreover, companies linked to consumer-focused companies would also face problems. For example, the demand for real estate may be stiffled, impacting the prospects of paint companies and those manufacturing tiles and faucets. As two-wheeler auto companies are losing ground, auto ancillary companies will face some troubles too. It's no brainer to realise that, the job market is going to get affected badly if these sectors are to sail through hot waters. This may further drag down the discretionary spending.

A culmination of these factors could be severe earnings downgrades across the board. Before demonetisation caught us unaware, markets appeared overvalued on their trail earnings. Post demonetisation, valuations have become even worse, if we factor in future growth prospects. So the current fall has fundamental reasons, and it's not just a sentimental impact of a disruptive action.

Another technical factor that may limit the upside of this market is the lack of leadership. Auto companies have tough days ahead, and banks are dealing with their own problems. NBFC space has been witnessing some panic selling, and consumer-focused companies are charmless too. Growth has been a big question mark for IT companies, although valuations in this space are reasonable and even attractive in some cases. This leaves only a handful sectors that may take a leadership position to lead the markets from the front.

The only ray of hope for the bounce back is—the flow of foreign capital resumes and investors take a slightly longer view on the markets ignoring the extraordinary circumstances that prevail now as one-offs.

Pullbacks are possible, but by and large markets are likely to remain lacklustre.

PersonalFN is of the view that, you shouldn't sell your equity holdings nor redeem your equity oriented mutual funds in panic. On the contrary, you might get some fantastic buying opportunities in the current market conditions. Smart investors aren't afraid of market volatility. This is not to say that, you should speculate on the direction of the markets and place your bets depending on their prospects.

Follow these 3 simple steps under current market conditions

Do you think it's a good time to invest in Indian equities and equity oriented mutual funds? Share your view here Facebook | Twitter

Stay connected with PersonalFN. Like us on Facebook , follow us on Twitter

|

Impact

If you are a borrower, good times might be knocking on your door. You can't expect macroeconomic conditions to get more favourable for you. In light of demonetisation, banks have been witnessing unprecedented inflows of deposits. This unexpected slosh of liquidity has allowed banks to lower the interest rates on deposits. SBI, Kotak Mahindra Bank, and HDFC Banks among others have slashed the deposit rates in the range of 15 basis points and 25 basis points. A basis point is 1/100th of a percent. It's just a matter of time now before they lower their lending rates too.

Inflation has been cooling off...

Retail inflation data for the month of October 2016 suggests that there have been fewer price pressures in the economy. As measured by the movement of Consumer Price Index (CPI), retail inflation stood at 4.20% in October. The food price inflation, denoted by Consumer Food Price Index (CFPI) came in much lower at 3.32%. The fall was mainly attributed to falling prices of pulses & products and vegetables. Sugar and confectionery products along with protein rich food items witnessed a sharp rise in the prices. Core inflation, i.e. inflation excluding food and fuel inflation also stayed within the comfort zone of RBI.

The RBI has set a target of 5.0% retail inflation by March 2017, while its medium-term target remains unchanged at 4.0% with a 2% margin of error on either sides.

Nose-diving inflation

Data as on November 15, 2016

(Source: MOSPI, PersonalFN Research)

On this backdrop, market expectations have started building around policy rate cuts. RBI is scheduled to announce fifth bi-monthly monetary policy review on December 07, 2016. At the fourth bi-monthly policy review meet held on October 03, 2016, a panel of 6 members (Monetary Policy Committee, MPC) reached a consensus, without any contrary view, to lower repo rates by 25bps.

The yield on India's 10 year-7.59%- 2026 sovereign bond has fallen by over 40 bps since the start of November. Besides, demonetisation which is assumed to be a positive for improving Government's financial position, expectations of a probable rate cut in the forthcoming monetary policy review have been driving the yields down. Comfortable liquidity position, thanks to high deposits over last one week, have pushed even short term yields down.

However, the choice may not be as simple as it looks this time for the MPC. At 6.42%, yield on 10-year benchmark bond may appear unattractive for Foreign Institutional Investors (FIIs). Especially considering that the Dollar Index recently touched a 13-year high. The yield on U.S. Benchmark 10-year notes has spiked up a little over 50 bps from October 21, 2016. Falling yields on Indian bonds, the rising US$, rising yields on US Treasury notes are likely to affect FII inflows in Indian debt. RBI may like to consider these "Trump-effects" before announcing fifth bi-monthly monetary policy review on December 07, 2016.

The ongoing demonetisation activities are likely to make a recovery in the capex cycle more challenging. On the contrary, banks will have to assess the effect of demonetisation on their bad loan position. Although, retail-centric businesses do not have a strikingly high share in stressed assets. Loans to small and medium businesses would have to be monitored carefully. Lower interest rates help reduce the interest burden on businesses. RBI must be watching these factors closely too.

What to expect?

As nearly 86% of Indian currency becomes redundant, consumption is bound to get affected. Trade activities in cash-driven India have almost come to a standstill. For the first time since the global financial crisis of 2008-09, India is facing a deflationary pressure. As a result, the RBI might find itself in an entirely different circumstances.

Until recently it maintained a hawkish stance on policy rates as the objective was to contain inflation. But if deflationary pressures kick in, the RBI may struggle to defend the inflation target on the downside. Let's not forget error of margin is 2%. In other words, if inflation falls below 3% by March 2017; it would be still considered a policy failure.

Odds against and in favour of policy rate cuts are evenly placed for now. The risk of deflation can't be underplayed.

Tough times… It remains to be seen what the 6-member expert committee decides on policy rates.

|

Impact

Problems plaguing the mutual fund industry in India appear to be far from over. Competition and cost escalations have caused many fund houses to shut shop in recent times. On the other hand, a majority of Indians are reluctant to invest in mutual funds and pose a threat to the growth prospects of the industry. Yes, Assets Under Management (AUM) of the mutual fund industry have been growing at a faster pace, but considering the true size of the market, mutual funds are still an unattractive option with the masses.

To add to the industry's worries, implementation of the Goods and Services Tax (GST) has opened up a new battlefront. Under the new regime, investing in mutual funds may cost investors more, as the cost of compliance for the fund houses is likely to shoot up substantially unless the Government provides some relief.

Industry players have teamed up to make their case. Last month, the Association of Mutual Funds in India (AMFI), along with PricewaterhouseCoopers (PwC) voiced the concerns of the industry and provided some valuable inputs to the GST Commissioner, Mr Upendra Gupta.

To read more about this story and Personal FN's views over it, please click here.

|

Impact

"We are going to do something so special. It will be so special. It will be an amazing day. It will be called Brexit plus plus plus," Mr Donald Trump told his supporters at a rally just before America went to vote. And as Trump predicted, his unexpected victory in the U.S. Presidential elections was nothing short of Brexit (when UK voted out of the European Union)—both of which sent international markets in a frenzy.

Trump's win surprised many in the U.S. and also came as a shock to the rest of the world. With Trump supporters celebrating the win, anti-trump factions took to the streets shouting slogans such as "Not My President". As America remains dazed on whether they have done the right thing, stock markets worldwide are in a state of flux.

Despite Trump's victory sparking panic in markets worldwide on the day of the election results, most global indices partially recovered. However, as traders evaluated the situation, Asian and European stocks took a beating the next day – in Friday's trade.

Performance Of Global Indices

| | 9-Nov-16 | 10-Nov-16 | 11-Nov-16 | | India - Sensex | -1.23% | 0.97% | -2.54% | | China - Shanghai | -0.62% | 1.37% | 0.78% | | Australia - ASX All Ord. | -1.94% | 3.26% | 0.70% | | Japan - Nikkei 225 | -5.36% | 6.72% | 0.18% | | Russia - RTSI | 1.82% | 0.35% | -2.38% | | Eurozone - Euro Stoxx 50 | 1.09% | -0.32% | -0.54% | | UK - FTSE 100 | 1.00% | -1.21% | -1.43% | | US - S&P 500 | 1.11% | 0.20% | -0.14% | (Source: ACE MF, PersonalFN Research)

Experts warn that the US and global economy faces a very uncertain future. There are still two-and-half months to go before the President-elect, Donald Trump (a Republican) finally enters the White House and takes over from Barack Obama (a Democrat) in January 2017. Global markets will be watching Trump closely to see if he goes ahead with the harsh policies outlined during his campaign.

Once he takes office, Trump's rejection of free trade and free markets could lead to raising tariffs on imports from China, Mexico and other countries. This will have a cascading effect on the global economy.

But there will be other policies which will be a part of his agenda, such as dealing with immigration, reducing taxes and Obamacare. This could lead to market volatility over the medium term, given the lack of clarity as to what Trump will prioritise in office.

Will Trump be a boon or a bane for the markets? And is now a good time to take exposure in offshore mutual funds (also known as global funds or foreign funds)? To help you decide, PersonalFN takes a deeper look at the performance of these schemes.

To read more about this story and Personal FN's views over it, please click here.

|

The cash crunch caused by the massive demonetisation is likely to become less severe in coming days. To make sure that the needy gets a chance to withdraw money, the Government has taken a slew of steps. They include, allowing the exchange of old notes for new only upto Rs 2,000 (earlier, per person limit was Rs 4,500). The others are as follows,

- The Government has allowed families are going into a wedding mode to withdraw Rs 2.5 lakh to look after expenses.

- Farmers will also receive a preferred status. The Government has allowed them to withdraw Rs 25,000 per week for buying fertilisers and seeds against their sanctioned loans.

Meanwhile, the Government sources have been briefing media that, printing of notes, and recalibration of ATMs is almost done and by the end of this month the situation is likely to get back to normalcy.

For now, it's just a hope. Let's wait and watch.

|

Demonetization: Demonetization is the act of stripping a currency unit of its status as legal tender. Demonetization is necessary whenever there is a change of national currency. The old unit of currency must be retired and replaced with a new currency unit.

(Source: Investopedia)

|

Quote: "If you want to have a better performance than the crowd, you must do things differently from the crowd."- Sir John Templeton

|

| |

| © Quantum Information Services Pvt. Ltd. All rights reserved.

Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 101 Raheja Chambers, 213, Free Press Journal Marg, Nariman Point, Mumbai 400021. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667 |