|

| March 17, 2017 |

|

|

|

|

Impact

Mutual funds are cool.

This is the message AMFI (Association of the Mutual Funds in India) is trying to pass on to millions of Indians.

Recently, it launched a campaign “SahiHai”, the Hindi slang for “cool”, to create awareness among investors and bust the misconceptions about mutual fund investing.

Even after decades of being in existence, mutual funds fail to become a popular investment route.

Undoubtedly, they need a better promotion strategy.

Mutual funds are supposed to spend 0.02% of their total Assets Under Management (AUM) on investor education. In the past, it was observed that they spent money set aside for investor education inefficiently.

As a corrective step, SEBI (Securities and Exchange Board of India) directed mutual fund houses to transfer half the corpus maintained for investor education to AMFI. The latter now has the responsibility to promote mutual funds in a right way.

AMFI is likely to spend around Rs 160 crore to Rs 170 crore on promoting mutual funds. The campaign “SahiHai” is expected to cost Rs 40 crore approximately.

Now the question is, has AMFI chosen the correct way to communicate it?

At the launch of “SahiHai”, Mr A.Balasubramian,Chairman of AMFI said, "There is a need to encourage households to shift from physical savings to financial avenues, especially mutual funds. With this objective in mind, under SEBI's guidance, AMFI has launched this investor awareness outreach program. I am sure the public will find these simple but powerful messages very thought provoking and will be encouraged to start investing in mutual funds."

J. Walter Thompson (JWT) - one of the most renowned marketing and communication brand- handled the responsibility of the creative work for the campaign. Hanoz Mogrelia, VP & ECD, JWT shared his experience about the campaign.

He said, "SahiHai may seem like a very simple idea. But, to execute this idea, we had decided to stay in the space of warm, real conversations between friends. We shot eight commercials over a fortnight using absolute 'non-models', we shot at real locations, using live sound recording. The client team must be commended for the tremendous faith they have reposed in this idea; and backing it with such a massive ad campaign."

It seems AMFI has tried to make the investors’ awareness campaign as realistic and convincing as it could. Now it remains to be seen if this hard work pays off.

But, the even bigger question that comes to mind is—by allowing revisiting advertisement guidelines for mutual funds, has SEBI done the right thing? As a result of this, now celebrities can start endorsing mutual funds, though at an industry level.

More details about the development...

- Celebrities are not allowed to endorse any specific scheme.

- Advertisements featuring celebrities shall take the prior approval of the capital market regulator.

- For the investors’ better understanding, mutual funds will have to show simple returns generated by a scheme, along with CAGR (Compounded Annualised Growth Rate) of investments.

- An advertisement about a particular scheme must also show how the other schemes managed by the same fund manager are doing.

It seems, while revising the advertisement code, SEBI has taken due care. It remains to be seen how celebrity endorsements actually work.

The propaganda of fairness creams sparked off debates on whether celebrities should be held responsible for their endorsements or the responsibility shall be fixed only on the product manufacturer (in this case, on the mutual fund industry).

Probably it will depend on the profile of a celebrity and how the advertisement is presented. Hopefully, SEBI will turn down ads that may paint a wrong picture. Celebrity endorsements will help the industry attract investors’ attention—the primary objective of any ad campaign.

However, one can only hope that celebrity endorsements won’t be unrealistic. Ads for health drinks, pan masala, and fairness creams have tainted the image and role of celebrity endorsements.

Promoting financial products is far more a serious affair than a tangible product. After all, it's a matter of one's financial wellbeing. Who will be responsible, if the narrative or the script of these celebrity ads go wrong despite SEBI having its check points?

Hopefully, the mutual fund industry will refrain from making lofty claims.

|

Impact

How would you react when a rating agency steps into advisor’s shoes?

“Conflict of interest”, some of us might say.

But it may not be the case, always.

Recently, Morningstar—an independent mutual fund rating agency, approached SEBI, seeking approval for its latest initiative. It intends to offer a model portfolio service to financial advisors. It believes, advisors opting for this service have a good chance of deepening relationships with clients, providing more refined advice, and cutting research costs.

Many financial planners and mutual fund advisors have been relying primarily on ‘star ratings’ offered by independent rating agencies. In addition to that, if they need a model portfolio, then they must evaluate whether or not they are on the right track.

Independent rating agencies analyse the performance of mutual fund schemes, based on their preset parameters. It’s perfectly fine for an advisor or a planner to refer to such analysis, as it helps making an informed decision. However, if advisors start using model portfolios, then they might end up reducing their job to that of a relationship manager.

One might argue that financial planners could devote more time to the planning aspect. As they save on time otherwise spent on identifying the right mutual funds, they can acquire and service more clients.

But an advisor has to consider if relying on the model portfolio helps in creating fully customized portfolio of mutual fund schemes.

As far as the model portfolios are concerned, any company will try to capitalise on its brand. Nonetheless, it’s upto the advisors to decide whether they want to reduce their role merely to that of a relationship manager or a business development manager.

PersonalFN believes the model portfolio is an ideal product for retail investors since it offers value and provides them with lots of conveniences. But for an advisor, it’s a dose of laziness. Can a doctor rely on medicines shortlisted by pharmacists? Ideally, she/he is expected to use her/his judgment, though there’s nothing wrong with seeking information from a pharmacist and depending on his expertise.

PersonalFN is of the view that, finding a trustworthy financial advisor has become tough these days. Being an unbiased and research-driven platform, PersonalFN believes in empowering advisors and helping investors find out reliable advisors in their neighbourhood. A good advisor will spend a maximum time on selecting the right schemes for his/her clients and trying to customise the portfolio to suit their needs. In contrast, a money-driven advisor will try to save time (and cost) in customising advice.

PersonalFN tries to find a golden mean. It helps connect ethical and capable financial advisors with investors who understand the value of excellent advice. Certified Financial Guardian (CFG) is not just your advisor, but he’s truly your guardian in money matters.

|

Impact

The effects of demonetisation on consumer demand seem to have remarkably faded in February 2017.

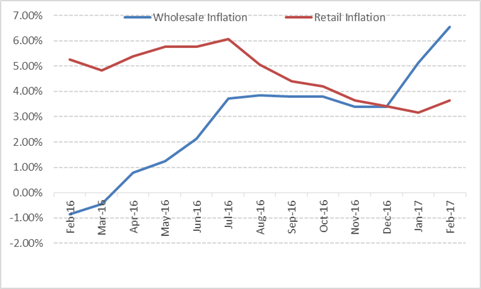

Retail inflation, measured by the movement of Consumer Price Index (CPI), increased from 3.17% in January to 3.65% in February. Food inflation jumped from 0.61% in January to 2.01% in February.

It's noteworthy that the core (non-food, non-energy) inflation quickened at a faster pace vis-à-vis CPI inflation.

What drove core inflation?

- Clothing and Footwear: 4.38%

- Housing: 4.90%

- Miscellaneous (includes personal care, healthcare, education, household goods and services and transportation): 4.79%

Interestingly, the Wholesale Price Index (WPI) too, an indicator of the industrial inflation, accelerated at a much faster pace in February. The WPI inflation for February came in at 6.55% (39-month high on cost of fuel and food items) vs. 5.22% in the previous month.

CPI Vs. WPI

(Source: MOSPI, PersonalFN Research)

The divergence between industrial inflation and the retail inflation can be attributed to several factors which include:

- The difference in the base year for both indices—CPI uses 2012 as the base year, while WPI is calculated using 2004-05 as the base year.

- Weights of the various items in CPI and WPI are different—for example, food articles account for a little over 14% in WPI, while constituting over 54% of CPI.

- A massive increase of 21.02% in fuel and power cost at the wholesale level and the lower base effect drove WPI higher.

- On the other hand, the impact of higher base effect on CPI has begun to wane.

To read more about this story and Personal FN's views over it, please click here.

|

Impact

Do you enjoy watching one-sided matches?

Nobody does.

But when it comes to equity markets, it seems they prefer unanimous victories in political battles.

In the recently concluded state assembly elections in 5 states, BJP is likely to form the Government in 4 states, while Congress will be in power in the remaining one.

BJP’s performance in Uttar Pradesh has been even better than the most optimistic estimates. A landslide victory in the India’s most populous state opens the floodgates for the Lok Sabha election 2019. Many political experts believed state election in Uttar Pradesh was the Semi Final match for the BJP—which it has won quite comfortably.

And, as a response to this triumph, investors splashed champagne and burst crackers on the Dalal Street. CNX Nifty touched an all-time high of 9,122 points when the markets opened for the first time after the results were announced.

Now the question is—is this optimism warranted?

Besides the improved chances of Mr Modi in 2019 elections, the ‘bulls’ believe that BJP’s tally in the Rajya Sabha is going to improve substantially in 2018. This will help the Modi Government pass significant legislative reform—a big positive for the Indian economy.

To read more about this story and Personal FN’s views over it, please click here.

|

|

Considering the growing use of mobile wallets, the Government expected e-wallet companies to offer insurance cover to its users. However, due to lack of ‘economic viability’ it seems, the companies have turned down such expectations. The Government believed, insurance cover would have shored up user’s confidence in digital wallets.

Nonetheless, the Ministry of Electronics and IT has released ‘The draft Information Technology (Security of Prepaid Payment Instruments) Rules 2017’ for public consultation. The rules are expected to strengthen the data privacy and improve the consumer protection policies.

|

Robo-Advisor : A robo-advisor (robo-adviser) is an online wealth management service that provides automated, algorithm-based portfolio management advice without the use of human financial planners. Robo-advisors (or robo-advisers) use the same software as traditional advisors, but usually only offer portfolio management and do not get involved in more personal aspects of wealth management, such as taxes and retirement or estate planning .

(Source: Investopedia)

|

Quote: "Those with the enterprise lack the money and those with the money lack the enterprise to buy stocks when they are cheap. "- Benjamin Graham

|

|

|

|

© Quantum Information Services Pvt. Ltd. All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 101 Raheja Chambers, 213, Free Press Journal Marg, Nariman Point, Mumbai 400021. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667

SEBI-registered Investment Adviser. Registration No. INA000000680, SEBI (Investment Advisers) Regulation, 2013

|