(Image source: Image by rawpixel from Pixabay)

(Image source: Image by rawpixel from Pixabay)

Taking courage from benign CPI inflation and lower 'core inflation' readings, the Reserve Bank of India (RBI), in a rare move, cut policy rates by another 35 bps (departing from the normal practice of 25 bps) with immediate effect in its 3rd bi-monthly monetary policy statement for 2019-20 (held on August 7, 2019). Thus, the policy repo rate is now at 5.40% to support growth amidst concerns of weak demand.

Table 1: Series of policy rate cuts in 2019 to address growth concerns

| Month |

Repo Policy Rate |

Policy rate cut (Basis points) |

Monetary Policy Stance |

| Feb-19 |

6.25% |

25 |

Neutral |

| Apr-19 |

6.00% |

25 |

Neutral |

| Jun-19 |

5.75% |

25 |

Accommodative |

| Aug-19 |

5.40% |

35 |

Accommodative |

| Total |

|

110 |

|

Data on Aug 7, 2019

(Source: RBI)

Perhaps, the six-member Monetary Policy Committee (MPC) heard the message from Finance Minister, Ms Nirmala Sitharaman loud and clear when she spoke to Economic Times earlier in July.

"I'll honestly wish (for a) rate cut ... and yes, a significant rate cut would do a lot of good for the country. I am conscious that the RBI has taken a very accommodative posture and done nearly... 75 bps (basis points rate cut). We will now have to look at that route with a lot more hope. The industry also feels there is space for it" - Ms Sitharaman, speaking to the Economic Times in an interview

Table 2: How did the MPC vote in the 3rd bi-monthly monetary policy statement 2019-20 resolution?

| MPC Members |

Voted to |

| Mr. Shaktikanta Das |

Reduce by 35 bps |

| Dr. Ravindra H. Dholakia |

Reduce by 35 bps |

| Dr. Michael Debabrata Patra |

Reduce by 35 bps |

| Mr. Bibhu Prasad Kanungo |

Reduce by 35 bps |

| Dr. Chetan Ghate |

Reduce by 25 bps |

| Dr. Pami Dua |

Reduce by 25 bps |

(Source: RBI's 3rd bi-monthly statement for 2019-20)

As exhibited by the table above, all six-members voted to reduce the policy repo rates. Further, the MPC decided to maintain the 'accommodative monetary policy stance'. These decisions were in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4.00% within a band of +/- 2.00% while supporting growth.

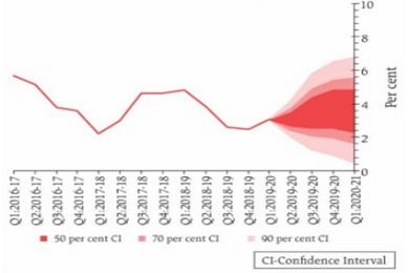

Graph 1: Where is CPI inflation headed according to the RBI?

(Source: RBI's 3rd bi-monthly monetary policy statement for 2019-20)

Taking into consideration several factors (namely: food inflation; spatial and temporal distribution of monsoon; lower core inflation; international crude oil prices; geopolitical tension in Middle-East; one year ahead inflation expectations of households; and impact of recent policy rate cuts), the RBI has projected CPI inflation at 3.1% for Q2:2019-20 and 3.5-3.7% for H2:2019-20 (a slight upward revision in the base range from earlier), with risks evenly balanced. For Q1:2020-21, CPI inflation is projected at 3.6%.

The MPC has noted that inflation is currently projected to remain within the target over a 12-month ahead horizon.

Path to interest rates...

The benign inflation outlook according to the RBI provides further headroom for policy action (rate cut and accommodative stance) to close the negative output gap while past rate cuts are being gradually transmitted to the real economy. Thus, the 'accommodative stance' is maintained.

How to approach debt mutual funds now?

(Images source: pixabay.com; photo credits rubylia)

Although my views have not changed much since the last time I wrote to you on July 29, 2019, here are a few more points to devise a sensible investment strategy...

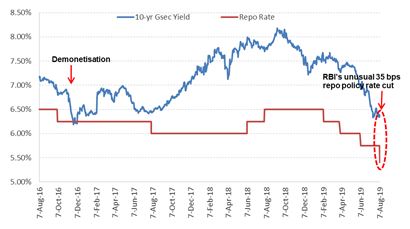

You see, even as the RBI's policy statement makes it quite clear that rates may reduce further, in my view, we are almost in the last leg of a rate cut cycle. Most of the rally at the longer end of the yield curve has already come about since the time RBI started reducing rates.

Graph: 2 The 10-year benchmark yield has softened since September 2018

Data as on August 7, 2019

(Source: RBI, PersonalFN Research)

Thus, debt mutual funds with exposure to the longer end of the yield curve, i.e. medium-to-long duration funds, long-duration funds, Gilt Funds, and Dynamic Bond Funds already delivered double-digit returns in the last one year. Going forward, the gains in these categories may be rather limited or less rewarding.

In addition, investing aggressively at the longer end may entail high volatility in the foreseeable future. Contrary to RBI's expectations, if CPI inflation moves up beyond its comfort zone or medium-term inflation target of 4.00%, the scope for a further policy rate cut from RBI reduces.

Nevertheless, still, if you wish to take the risk and exposure at the longer end of the yield curve, consider dynamic style funds that have the flexibility to move across maturities of debt papers as per the interest rate scenario.

Ideally, you'll be better off if you deploy your hard-earned money in shorter duration debt mutual funds. But ensure you approach even short-term debt funds with your eyes wide open and pay attention to the portfolio characteristics and quality of the scheme.

A fact is, many debt funds across maturity profiles already have exposure to downgraded and toxic debt papers which heightens the investment risk.

So, prefer the safety of principal over return. Stick to mutual funds where the fund manager doesn't chase returns by taking higher credit risk. Further, asses your risk appetite and investment time horizon while investing in debt funds.

While investing in short-term debt funds, consider keeping an investment horizon of at least 2-3 years.

If you have an investment horizon of 6 to 12 months, ultra-short duration or low duration funds may be suitable.

And if you have an extreme short-term time horizon (of 3 to 6 months), consider liquid funds with high-quality debt papers, which do not have high exposure to Commercial Papers (issued by private entities). Alternatively, if you wish to park in a much safer category, you would be better off investing in overnight funds.

Remember, investing in debt funds is not risk-free.

If you prefer to keep your capital safe, opt for fixed deposits.

[Read: Factors To Look At While Investing In Bank FDs]

Editor's Note: If you wish to select the worthy mutual fund schemes --both, equity and debt mutual fund schemes -- to address your future financial needs, I recommend that you subscribe to PersonalFN's unbiased premium research service, FundSelect.

With FundSelect, you get access to high quality and reliable funds picked by our research team using their comprehensive S.M.A.R.T. score fund selection matrix.

Each fund recommended under FundSelect goes through our stringent process, where they are assessed on both quantitative as well as qualitative parameters.

Every month, PersonalFN's FundSelect service will provide you with insightful and practical guidance on equity mutual funds and debt mutual fund scheme --- the ones to Buy, Hold, or Sell.

If you are serious about investing in rewarding mutual fund schemes, subscribe to PersonalFN's flagship mutual fund research service FundSelect today!

Happy Investing!

Add Comments