Indian asset classes hold wealth creating potential for NRIs

In our last article, we took our NRI friends through host of domestic socio-economic fundamental factors which still makes India a promising investment destination despite overcast of debt-overhang in the developed economies. Today, in context to those factors, let us see whether the important asset classes in India are indeed enticing for NRIs to invest.

Equity:

Equity as an asset class is often found to be quite tantalising and thrilling by many individuals during euphoric times. But times are different now, and identifying promising investment destination isn’t easy.

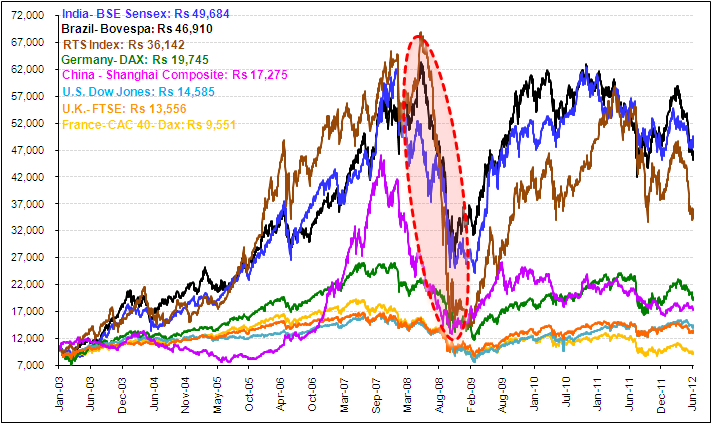

India equity markets Vs. other BRIC markets and Developed markets

Base: Rs 10,000

Data as on June 8, 2012

(Source: ACE MF, PersonalFN Research) With gloomy clouds surrounding the global economy, there’s enough turbulence which could kill the thrill and therefore you as NRIs need to be vigilant and wary about which economies you park your hard earned money while taking exposure to equity.

The chart above reveals that even during the euphoric phase from 2003 until the U.S. subprime mortgage crisis broke out, only Brazil, Russia and India managed to provide magnanimous returns for investors. China showed a sharp impulse only a couple of years prior until the U.S. subprime mortgage crisis. As far as equity markets in developed economies are concerned, although they too exhibited an uptrend, the returns weren’t very luring (due to possible focus of investments on other asset classes or even other emerging market such as ours). While the U.S. subprime mortgage crisis and Lehman Brothers bankruptcy had a rippling and crippling effect on both developed and emerging economies, and also led to the violent fall in the equity markets, a noteworthy point is, India especially amongst the BRIC nations displayed a smart and robust recovery. And even now, while we are feeling the shivers of the debt-overhang situation in the Euro zone, India is still relatively resilient due to favourable underlying fundamentals. All those who had invested nearly a decade back after the occurrence of tech-bubble, but stayed invested for the long-term have still made whopping absolute returns of 396.8%. Thus, your investment of Rs 10,000 in the Indian equity markets on January 2, 2003 would have fetched you a sum of Rs 49,684 as on June 8, 2012.

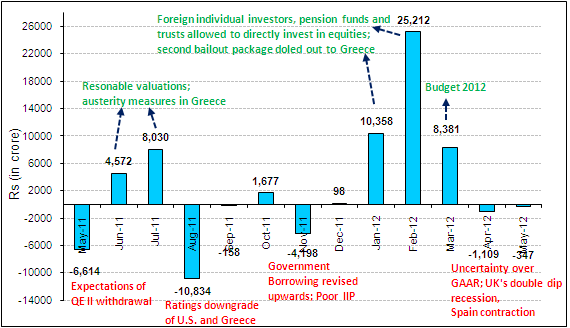

FII flows

(Source: ACE MF, PersonalFN Research) Yes, the Indian equity markets have been vulnerable to FII flows and have depicted a see-saw movement in the last couple of years (due to host of domestic and global economic factors), but a noteworthy point is that FIIs are keeping India on the radar of promising investment destinations given the luring economic growth which is well supported by demographic advantage and strong consumption theme.

We approve of the fact that, in the recent times the Indian Government’s stance on tax policies has been unpredictable and has depressed the investment mood; but if intent to bring down fiscal deficit is present, it would do more good than harm to India in the long-term. The Government in order to create a favourable investment climate is already pushing for infrastructure development to provide an impetus to economic growth. Likewise, the finance ministry is busy preparing a new policy road map for the banking sector, which is intended to provide clear roadmap for small banks such as Regional Rural Banks (RRBs), cooperative banks and other regional banks. Thus rays of reform measures are evident although the Government has been tarnished for policy paralysis. We are of the view that myopic oppositions should be refrained, so that reforms can be put on fast-track and Indian equity markets can benefit therefrom.

But, the global economic headwinds...

We recognise that with downbeat sentiments looming around (led by debt-overhang situation in the Euro zone) putting downward pressure on the Indian equity markets, you may prefer to hold cash, rather than invest in equities. But in our view, the valuations of the Indian equity markets are very luring to invest, provided you adopt a staggered approach of investing in the backdrop of current gloomy clouds.

The Euro zone at present is witnessing contraction in economic growth and Spain (4th largest economy in Euro zone) hasn’t been spared from a rating downgrade (by three notches to "BBB") from Fitch due to banking crisis. Likewise "Grexit" could also rattle global markets. But, we ought to recognise that the monetary policy actions thus far taken by India are far more prudent when compared to developed economies, which has kept our economy post luring economic growth than that clocked by developed economies. While at present Standard & Poor’s (S&P) has issued warnings that India’s ratings could be placed to junk due to slump in economic growth, widening fiscal deficit, Government expenses and political vacuum; it is important to note that our Government borrows only in local currency and not the U.S. dollar, and thus the risk is less and may not have much impact. Moreover, we are of the view that in times such as these, the Reserve Bank of India (RBI), may show consideration towards economic growth, and thus cut rates marginally to revive economic growth rate (although inflation risk still remains).

So, what should be your investment strategy during such turbulent times?

We think that, we all are aware of the fact that nothing in this world is linear. And the equity markets too, aren’t any different to that rationale. In the short-term, there would always be impulse as well as corrective moves for the equity markets in the backdrop of several economic events. But if one stays invested for the long-term (with timely portfolio re-balancing), the sweet fruits of investment can be obtained. The line chart displayed above, is an example of this, where nearly in a decade’s time the equity markets have undergone several events - both positive as well as negative, but has created wealth for investors.

In the backdrop of the present global as well as economic events, it would be wise for you as an NRI to stagger your investments by adopting a gradual approach of investing. But you must adopt caution and look at value buying opportunities, which can help you create wealth. Thus while directly investing in the Indian equity markets through stocks, care should be taken to buy fundamental strong companies which have great managements to drive the company on the growth path. However as NRIs, if you aren’t conversant about Indian equity markets or do not possess good stock picking abilities, we suggest that you opt for diversified equity mutual funds in India which follow strong investment processes and systems. But being in coherence to the staggered approach of investing, it would be wise to opt for the SIP (Systematic Investment Plan) mode of investing (as against the lump sum mode) as this well enable you to mitigate the volatility through rupee-cost averaging and power your portfolio with the benefit of compounding. However, don’t forget to stay invested for the long-term in order to reap fruitful benefits.

How should NRIs invest in the Indian equity markets?

In order to invest in the Indian equity markets, a PAN card would be required followed by opening bank accounts. While opening a bank account, as NRIs you need to ascertain whether the returns generated from your investments would be repatriated abroad or not and accordingly open an account. If you intend taking back the amount to the country you reside in, then an NRE (Non-Resident External Rupee) account would be the most appropriate. On the other hand, if you intend to keep the money in India, the NRO (Non-Resident Ordinary) account, will serve your purpose. Although, the initial paper work may be cumbersome, it is indeed required for NRIs to complete it and comply with regulations. However, if you were an NRI earlier but now returned to India for good, you would experience less cumbersome procedures. While investing in the Indian equity markets, ask your bank for a Portfolio Investment Scheme (PIS) approval, for which the bank may charge you a nominal fee; and once you have the approval you would be allowed to invest in the Indian markets. It is noteworthy that PIS is regulated by RBI, who monitors the investments made by non-residents so that it can keep a tab on money flowing into India from outside the country.

Today for buying shares in the Indian equity markets, you may be aware that opening a Demat and trading account is a must to buy shares in an online form. However, it is noteworthy that for NRIs "day trading" (i.e. buying and selling on the same day) is not permitted, thus allowing you to "invest" on a delivery basis in the Indian equity markets. While there are no specific rules in place for the holding period, we are of the view that Indian equities in the long-term can create wealth, thereby refuting the detrimental newsflashes in the short-term, and therefore the investment horizon should be long enough. Moreover, we affirm that a trader is only good till his last trade, as you won’t be aware what the future has in store for you - good, bad or ugly. Thus while your stock broker may tempt you trade more often, it is better that you refrain from trading in Indian equities. Here, it is also imperative that you select your stock broker wisely. While selecting a stock broker, prefer the SEBI-registered one’s and scrutinise onto their net worth, balance sheet, the technology they are using, etc. and all such aspects to ensure safety about with whom you are transacting. In stocks, NRIs are not allowed to invest beyond 10% of the paid-up capital of a company.

As far as investing in mutual funds is concerned, although there are mutual funds registered abroad focusing on India as an investment destination, in our view it would be prudent to invest directly in India registered mutual funds which are investing in India. This is because the significance and undercurrents of the economy are well understood by the fund managers of the home country. For investing in an Indian mutual fund scheme(s) you can transact directly. But in case if you are transacting through a broker / mutual fund distributor, care should be taken to select them wisely, for you to obtain the right wealth creating advice. Your investment can be made from the NRE or NRO account (depending whether you need to repatriate the amount in the future) and needs to made in Indian rupees. You can hold your mutual fund investments either in a physical form (i.e. paper form) or simply own them in your demat account. Care should be taken to have only wealth creating mutual funds in your portfolio, and to do so either enough research should be undertaken by you, or seek help from a reputed mutual fund research house.

Debt:

Apart from the Indian equities which has the required synergy to create wealth for you in the long-term (provided you are willing to take risk and identify right stocks), the Indian debt markets too, offer an excellent investment opportunity for risk averse investors, who are looking forward to safeguard their portfolio by investing in debt instruments. It is noteworthy that, this asset class can provide the much needed stability to your portfolio, and thus it is imperative that even though you have the appetite to take risk, you as NRIs must have a part of their your portfolio invested in Indian debt instruments. But before we assess the different types of debt instruments which NRIs can invest, let us have a look at the current debt market environment in India.

At present, the interest rates in India remain elevated. But are expected to gradually cool down in an attempt to revive economic growth rate (India’s GDP growth rate for FY12 is at 6.5%). It is noteworthy that the anti-inflationary stance adopted by RBI, made way for the high interest regime, which made investors expect high yields on debt instruments held by them. But in turn, the high interest regime had an effect of slumping economic growth as borrowing cost increased, and global economic headwinds also had negative role to play. And now with gloomy clouds of debt-overhang sending negative ripples to the Indian economy, the central bank is likely to show consideration towards economic growth. Moreover, if moderation in headline inflation occurs, it is likely to provide an elbow room for policy rates to fall, and therefore the yields as well (due to positive co-relationship between interest rates and yields).

Policy rates across nations

| Country | Policy rates (%) | Unchanged since |

| Japan | 0.10 | 5-Oct-2010 |

| United States | 0.25 | 16-Dec-2008 |

| United Kingdom | 0.50 | 5-Mar-2009 |

| Eurozone | 1.00 | 8-Dec-2011 |

| South Africa | 5.50 | 18-Nov-2010 |

| China | 6.31 | 7-Jun-2012 |

| India | 8.00 | 17-Apr-2012 |

| Russia | 8.00 | 23-Dec-2011 |

| Brazil | 8.50 | 30-May-2012 |

(Source: Central banks of respective nations, PersonalFN Research) Having said that, interest rates in India still look very attractive for one to invest in India when seen in comparison to the developed economies, and this has made India, a darling of many investors who want to build a high yielding debt portfolio. Also, prudent policy measure adopted by India during times of global economic crisis has reflected ability to weather the shivers sent from debt-overhang situation of the Euro zone crisis.

So, which are the debt investment avenues available for NRI?

There are a number of debt investment avenues available for you to invest; but you ought to be clear whether you would like to invest on a repatriation basis or a non-repatriation basis, as this will help you choose the right investment instrument. The following investment instruments allow you to invest without any limit on a repatriation basis and non-repatriation basis:

- Dated Government securities (other than bearer securities)

- Treasury bills

- Bonds issued by Public Sector Undertakings (PSUs) in India

- Units of domestic debt mutual funds

However, units of money market mutual funds in India and National Savings Certificates are strictly allowed to be held on a non-repatriation basis. For investment purpose one can also maintain their NRE account or NRO account (as the case may be) in a term deposit form. But in case of NRO deposits interest income would be liable to income tax, while for NRE account, the accrued interest income as well as balance held would be exempt from income tax and wealth tax.

It is noteworthy that securities purchased and held by you, can be sold only through the recognised stock exchange (via a recognised stock broker) or tender them back to the issuer for re-purchase or at maturity. Moreover, transfer of securities to other NRI is also not barred by Foreign Exchange Management Act, 1999 (FEMA), provided the purchase of such securities / units was made on a repatriation basis.

But apart from being cognisant about investing in NRE or NRO term deposits, if you aren’t well-versed about other debt investment instruments, routing your investment in the Indian debt market via debt mutual funds would be a prudent decision to take.

At present there are various categories of Indian debt mutual funds, in which you may invest. They are:

| Type of Fund | Invests in... |

| Liquid Funds | Mainly invest in very short term money market instruments with maturity upto 90 days. Also invest in call money

|

| Liquid Plus or Ultra Short Term Debt Funds | Portfolio is comprised of a mix of certificate of deposits, commercial paper, call money and other money market instrument with slightly higher maturity than the instruments held in liquid funds

|

| Floating Rate Funds | Typically invests in short-term instruments offering flexible interest rates i.e. whose interest rate reflects the prevailing interest rate in the country

|

| Short Term Income Funds | Have exposure to short-term bonds, deposits and NCDs. May also invest in T-bills and Government securities with maturity of less than 3 years

|

| Dynamic Bond / Flexi-Debt Funds | Such funds invest in short term as well as in medium-term bonds, NCDs and G-secs

|

| Long Term Income Funds | Invest in corporate bonds, debentures and G-secs with maturity of more than 5 years

|

| Gilt Funds or G-sec Funds | Invests only in securities issued by the Central and State Government.

|

| Fixed Maturity Plans of 3 months to 36 months | Have exposure to bonds and NCDs having maturity profile in line with the horizon of the Fixed Maturity Plan (FMP).

|

But before you decide on which one of them to invest in, you need to be sure of your investment time horizon and liquidity preference. Also, you need to be well-versed with the prevailing interest rate scenario, so that you can make a correct investment decision which can optimise your returns.

So, what should be your investment strategy in the current interest rate scenario?

With markets expecting the central bank to cut rates to provide an impetus to economic growth, and fall in Brent crude oil prices making it conducive to do so; the sentiments are expected to remain positive for some time in bond markets. However, the weakness in Indian rupee and CPI and WPI inflation being above the comfort range (6.0% to 7.0%) of RBI may be a hurdle for any market friendly move by the central bank. Moreover, with monsoon being delayed and risk of "El-Nino" phenomenon persisting may fuel food inflation which would diminish the chance of an aggressive rate cut.

Hence at present while taking exposure to debt mutual funds and fixed income instruments, you should clearly know your investment time horizon. Since short-term rates may still be high in the near term and then ease due to liquidity infusion; you can benefit from being invested in debt mutual funds having exposure to shorter maturity instruments.

If you have an extreme short-term time horizon (of less than 3 months) you would be better-off investing in liquid funds for the next 1 month or liquid plus funds for next 3 to 6 months horizon. However, if the investment time horizon is short to medium term (of 1 to 2 years) you may allocate a part of your investments to short-term income funds which should be held strictly with at least 1 year time horizon.

The present scenario also seems comfortable to look at longer horizon debt mutual funds. Thus, if you have a longer time horizon then you can now hold some exposure to pure income funds. Since longer tenor papers will become attractive, longer duration funds (preferably through dynamic bond / flexi-debt funds) can be considered, if one has an investment horizon of say 2 to 3 years. However, one may witness some volatility in the near term as there is always an interest rate risk associated with longer maturity instruments.

Fixed Maturity Plans (FMPs) of upto 1 year would continue to yield appealing returns and can also be considered as an option to bank FDs only if you are willing to hold it till maturity. Since NRIs aren’t refrained from investing in FDs, they can also be considered due to the luring rate of interest offered on them. Also if you have an invested in Public Provident Fund (PPF), before you became an NRI, you can continue investing in it too till maturity on a non-repatriation basis.

Gold:

During turbulent times such as the one engulfing the global economy at present, gold could be a good hedge for your portfolio. While many of you may express dissent, looking at the elevated prices of gold, the gloomy global economic outlook, situation of debt-overhang in Euro zone, slash in sovereign ratings and high fiscal deficit in the domestic market makes a case for investing in the precious yellow metal, and thus prices are expected to remain firm.

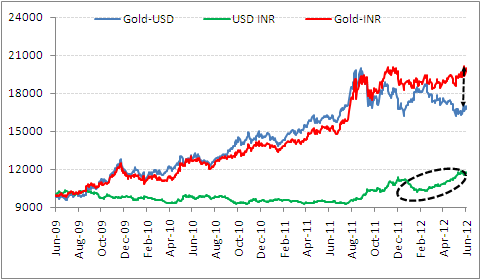

Gold movement in INR and USD term, along with INR movement

Base: Rs 10,000

Data as June 13, 2012

(Source: ACE MF, PersonalFN Research) Also, the persistent weakness in the Indian rupee is making a case for holding a portion of your investment in gold in India. The chart above depicts that 3 years ago, if one were to invest in gold in rupee terms, one would have yielded a whopping returns of 100% (in absolute terms), as against 70% (in absolute terms) for investment in U.S. dollar terms. This is because, the whopping return for investing in gold in rupee terms was well supported by 17% depreciation in the Indian rupee in the last three years. However, the sharp depreciation in the value of the Indian rupee in the last 5 months (by 13%) helped to accentuate gains in gold in rupee terms.

Going forward although the Indian rupee is expected to gain against the U.S. dollar, the escalation in Euro zone crisis and possible quantitative easing could keep the secular uptrend intact for the precious yellow metal, as smart investors would take refuge under gold to safeguard their risk. It is noteworthy that with easy monetary policy adopted by central banks - especially in the developed economies, inflationary situation may occur, and thus investing in this asset class could be a good hedge against inflation.

Hence to sum-up, gold prices are expected to pave their path on mix of the following domestic and global factors:

- Indian rupee movement vis-a-vis the U.S. dollar

- Import of gold

- Inflationary situation

- Global macro-economic headwinds

- Consumption traits

So, how should NRIs invest in gold and what should be their investment strategy?

We think that one should have a minimum of 5%-10% allocation in gold, from an asset allocation point of view which can aid in reducing risk on the overall investment portfolio. Moreover, you need to invest in this asset class from a long-term perspective with a time horizon of 10 to 20 years.

As far as how to invest in gold is concerned, we recommend that you invest through Gold ETFs (GETFs), as against physical gold, due to the merits which GETFs imbibe in them.

India is an attractive investment wealth creating destination for NRIs:

Thus, as seen above the economic factors under each of the asset classes explained above, makes India an attractive investment destination for wealth creation. However while investing in these asset classes; we suggest that you as an NRI investor adopt a smart approach, whereby you consider the following aspects:

- Your investment objective

- Time horizon for which you are willing to stay invested

- Age,

- Income

- Number of dependents

- Expenses

- Risk appetite

And once you have done that prudently, you also got to review your portfolio and re-balance if required. Portfolio rebalancing refers to the action of bringing a portfolio of investments that has deviated away from target asset allocation. The goal of rebalancing is to move the current asset allocation back in line to the originally planned asset allocation. Rebalancing is primarily warranted under conditions where the returns have significantly deviated than expected or to stay in line with market conditions. For example, an equity heavy portfolio needs to be restructured in contraction phases where company profits are hit harder and interest rates move up. It could be done by moving a portion of equity holdings to debt instruments. Mutual funds probably allow the easiest window to rebalancing due to their diversity of offerings.

While many of our NRI friends would be surprised, not to see real estate as an asset class in this article; we would be coming up with a separate coverage in one of our ensuing articles. Until then Happy Investing!!

This NRI article has been authored by PersonalFN, exclusively for Quantum Mutual Fund. PersonalFN is a Mumbai based personal finance firm offering Financial Planning and Mutual Fund Research services.

Statutory Details, Disclaimers and Risk Factors:

This note / article is for information purposes and Quantum Information Services Limited (PersonalFN) is not providing any professional / investment advice through it. The facts mentioned in the note are believed to be true and from a reliable public source. The Service should not be construed to be an advertisement for solicitation for buying or selling of any scheme / financial product. PersonalFN disclaims warrants of any kind, whether express or implied, as to any matter/content contained in this note, including without limitation the implied warranties of merchantability and fitness for a particular purpose. PersonalFN and its subsidiaries / affiliates / sponsors / trustee or their officers, employees, personnel, directors will not be responsible for any direct/indirect loss or liability incurred by the user as a consequence of his or any other person on his behalf taking any investment decisions based on the contents of this note. Use of this note is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. PersonalFN does not warrant completeness or accuracy of any information published in this note. This note is for your personal use and you shall not resell, copy, or redistribute this note, or use it for any commercial purpose.

Add Comments