(Image source:Image by rawpixel from Pixabay)

(Image source:Image by rawpixel from Pixabay)

If you want complete safety of your capital, don't look beyond government-backed Small Savings Schemes (SSS) and government treasuries.

That said, no Public Sector Bank (PSB) has defaulted so far. Therefore, you may consider a deposit with a PSB equally safe, at least until the government remains the largest shareholder.

Beyond this, everything else under the fixed income category comes with risk.

Have no confusion there.

In other words, all your investments in debt funds, corporate deposits, and Non-Convertible Debentures (NCDs) are subject to credit risks. It's just that the level of risk varies.

But greed never lets investors recognise a risk unless it knocks off their investments.

In search of better returns, investors often chase debt funds, corporate fixed deposits and Non-Convertible Debentures (NCDs). More so when RBI is slashing policy rates and banks lower the interest rates on fixed deposits.

Until recently, investors considered debt funds as an alternative to bank FDs. Many investors were under the impression that debt funds are relatively safe, although sophisticated investors always knew these could never be entirely safe.

However, the recent fiascos such as IL&FS, Reliance ADAG, Essel Group, and DHFL exposed irresponsible mutual funds. IL&FS has a debt pile of approximately Rs 93, 000 crore. Thus, it has affected almost all big institutional investors/lenders to a varying extent.

Now that Fixed Maturity Plans (FMPs) holding back maturity proceeds or rolling them over by meeting investors privately, there're uncertainties about the prospects for debt funds.

There is a view that investors might go back to company fixed deposits and NCDs. Some feel that mutual fund houses may continue to make unpardonable mistakes and are likely to continue to get away with it --- thanks to an important disclaimer: Mutual fund investments are subject to market risks.

At a time when institutional investors are struggling to evaluate credit risk, how likely are individual investors to do an accurate assessment before investing in corporate FDs and NCDs?

If you think you can rely solely on credit rating agencies and invest in NCDs, think twice.

[Read: Approach Debt Funds With Your Eyes Wide Open]

Even "AAA" rated NCDs can make you look like a loser if you trust credit ratings blindly. Never take credit ratings for granted, especially when the market sentiment is terrible and downgrades are a commonplace.

Like equity shares, NCDs are traded in the secondary market; and like equity shares, they too can give you sleepless nights with unpredictable dynamic price fluctuations.

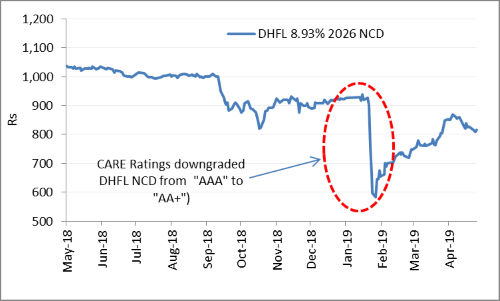

For instance, DHFL 8.93% 2026 NCD.

Chart1: DHFL NCD nosedived...

(Source: NSE)

(Source: NSE)

Above chart explains how wildly bond prices react to credit events and all other news concerning the company's debt servicing ability, fundraising ability, and cost of funds. Besides rating downgrade, DHFL's NCD also reacted to rising spreads and the media reports that accused DHFL promoters of syphoning funds.

Later, bond prices recovered after the auditors gave DHFL and its promoters a clean chit, but highlighted several deficiencies in the lending processes to certain firms. In other words, the auditors' findings suggest how fragile the "AAA" rating was.

No wonder, despite RBI slashing policy rates twice in 2019 so far, DHFL bond prices have failed to recover to their pre-crisis level. Those who don't remember, DHFL episode started with DSP Mutual Fund selling some of its commercial papers at a steep discount in September 2018.

But did you notice, under the panic market situation, the aforementioned NCD of DHFL NCD slipped to Rs 584 (against the face value of Rs 1,000). Whoever bought it at this price would have not only made quick capital gains, but might have also locked a very high yield of 15%, considering recovery in prices. But buying an NCD at over 40% discount requires guts and thorough understanding company's business.

You might want to fancy your courage by buying NCDs available at steep discounts, but do you think you are well equipped and experienced to take such calls?

If "no" is your answer, drop the idea of buying NCDs in the secondary market.

Buying NCDs in the secondary market isn't a child's play.

As remains the question of investing in NCDs when companies issue them in the primary market, be prepared to stay invested until maturity. Again, that's a big call. Nobody could identify and document the trouble IL&FS faced until it defaulted. How would one evaluate the company's ability to pay regular interest for longer duration say, 5,7,10 years?

Risks are real, aren't they?

The same holds true for company fixed-deposits.

Before the Companies Act 2013 made it mandatory for deposit-taking companies to obtain credit ratings, defaults were prevalent. The instances of defaults on corporate FDs have become less frequent since then. But default risk is still a real risk.

In the last 10 years, well-known companies such as Unitech, Elder Pharma, Ansal Properties, DSK Group, Birla Shloka EduTech, Jaiprakash Associates, Bilcare, Plethico Remedies, and Helios and Matheson among others have defaulted.

It's noteworthy that most of them had offered as high as 12% interest for deposits having a maturity of 1-3 years.

What's common among defaulting companies?

-

Most of them are often buried under a debt pile

-

They don't generate adequate profits to sustain debt

-

Naturally, they borrow to repay old loans

-

Struggle to sell their assets and raise money

-

Offer little defence to FD investors since corporate fixed deposits are often unsecured in nature

How can you avoid falling in the trap?

Learn to ignore the lure of higher interest rates. If a listed company offers you a rate of 12% when an equivalent company can secure a bank credit facility at a much lower rate say 10%; be sure there's some stress on its balance sheet.

Debt funds, corporate fixed deposits, and NCDs all might generate superior returns as compared to government-backed deposits and securities. However, the additional return is simply the compensation for taking additional risk.

Like a mirage in a desert, superior returns are illusionary in the financial parlance. But professionals call it a skill until the real risks decide to make a mockery of their claims.

All professional money managers and advisers alike use disclaimers as a refuge.

The financial market is a jungle. Here nobody else can care about the safety of your capital, as you would. Learn to balance out your greed and fear.

PS : If you are looking for funds that carry a Potential to Beat the market by as much as 70%! Subscribe to PersonalFN's 'FundSelect' service. It is a credible mutual fund research service with a track record of more than 15 years.

Once you subscribe to FundSelect, you will get instant access to potentially the best equity and debt mutual fund to invest and even recommendations on the ones to 'Hold' and 'Sell'.

Click here to know more

Click here to know more

Add Comments

| Comments |

rcheenu@gmail.com

May 10, 2019

Very informative and thought provoking. |

1