The exuberant phase of the equity markets, are often sunny times for several manufacturers of financial products and investors. While some smart investors prefer to book profits during such times, there are several who elevate their confidence during euphoric times. And interestingly banking on the upbeat investor mood, manufacturers of financial products too, launch new financial products. Have you wondered why such financial products aren’t launched when sentiments in the markets are low? Well, the answer in our view is simple. They (manufacturers of financial products) want to make hay when the sun shines, by garnering more Assets Under Management (AUM) during euphoric times, when investor sentiments are upbeat.

Take for instance the recent past; there have been number of New Fund Offerings (NFOs) from various mutual fund houses as the Indian equity markets have scaled up by nearly 13.3% in the last 2 ½ months. While many get wooed by the Rs 10 investment proposition, in our opinion it may not always be prudent investment decision. In fact with 870 equity mutual fund schemes already in existence (including the options therein), addition of new schemes, in our view creates a dilemma in the minds of the investors, as to how they should rightly select and invest in winning mutual funds. While there is galore information to address to this issue, we think that "information overload" could actually confuse investors and make the task of selecting winning mutual funds tougher rather than easier.

While many may argue that you can simply go with star rated funds, the question which arises to our mind is can these star rated funds be like real rock stars in your mutual fund portfolio. Today, interestingly the media - both print as well as the electronic media, also sermon about star rated funds so often, that it has an influencing impact on the minds of many investors. Banking on this environment, mutual fund distributors / agents / relationship managers too are busy persuading their clients to invest in star rated mutual funds. But question still remains unsolved, "are you buying rock stars or winning mutual fund schemes to your portfolio?"

It is vital to recognise that just having blind faith and following the norm that more "stars" there are on the scorecard, better is the fund's performance; sounded good or logical during our school days when a 5 star for our homework, connoted that we were good students.

But it is vital to recognise that evaluating a mutual fund's performance is far different!

It is noteworthy that most star ratings take into account only quantitative methodology considering the past performance (returns), expense ratio, risk (Standard Deviation) and risk-adjusted returns (Sharpe Ratio) of the respective fund. But they ignore the qualitative factors such as the fund house history, its credentials, the investment systems and processes followed by the fund house, portfolio characteristics, adherence to the stated investment objectives etc; which drives the performance of the fund in future. Remember, forecasting the fund’s future performance is no cakewalk. It is not a simple function of "sorting" on excel - as used in most of the rating methodology.

Moreover ratings subscribe to the "one size fits all" approach. They seem to suggest that if a fund has earned a top-notch position, investors across categories can invest in the same. But remember investing and financial planning are personalised activities. Hence, a fund could be right for one investor and (despite its sterling performance) be completely unsuitable for another. Yes, they could perhaps serve as starting points for identifying a broader set of investment-worthy funds; but investing in a fund, based solely on number of stars against its name may not be the right move.

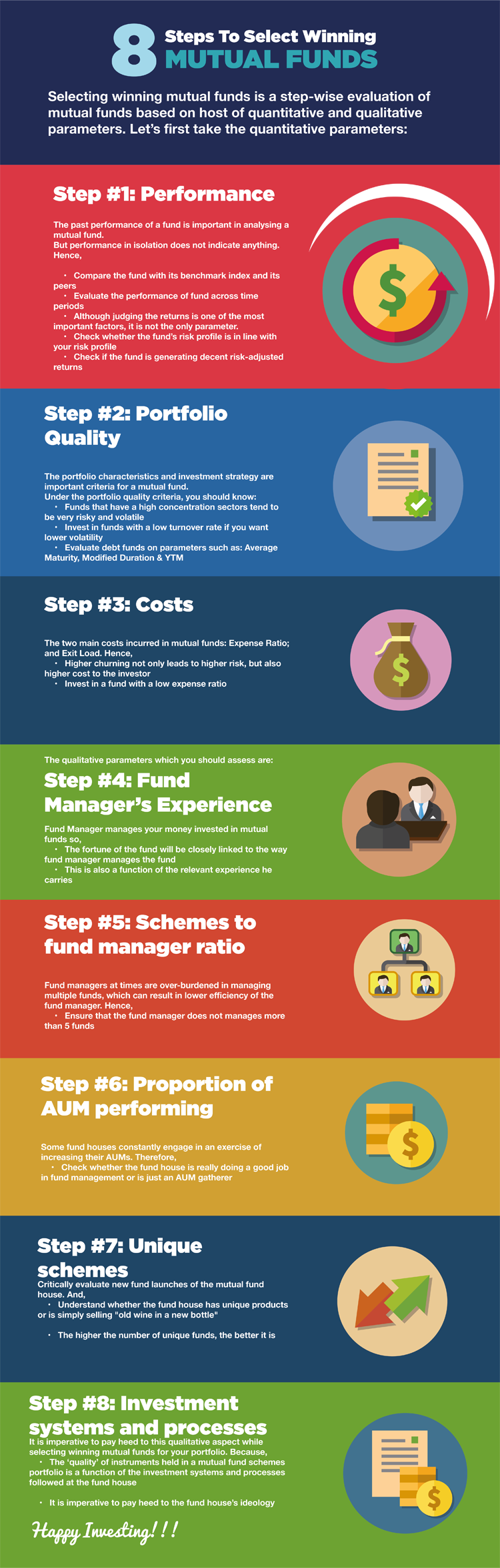

The fact is, not all mutual funds are same. There are various aspects within a mutual fund scheme, which are vital for investors to study carefully before investing; which are:

- Performance: The past performance of a fund is important in analysing a mutual fund. But, remember that past performance is not everything, as it may or may not be sustained in future and therefore should not be used as a basis for comparison with other investments.

It just indicates the fund’s ability to clock returns across market conditions. And, if the fund has a well-established track record, the likelihood of it performing well in the future is higher than a fund which has not performed well.

Under the performance criteria, we must make a note of the following:

- Comparison: A fund’s performance in isolation does not indicate anything. Hence, it becomes crucial to compare the fund with its benchmark index and its peers, so as to deduce a meaningful inference. Again, one must be careful while selecting the peers for comparison. For instance, it doesn’t make sense comparing the performance of a mid-cap fund to that of a large-cap. Remember: Don’t compare apples with oranges.

- Time period: It’s very important that investors have a long-term horizon (of at least 3-5 years) if they wish to invest in equity oriented funds. So, it becomes important for them to evaluate the long-term performance of the funds. However this does not imply that the short term performance should be ignored. Besides, it is equally important to evaluate how a fund has performed over different market cycles (especially during the downturn). During a rally it is easy for a fund to deliver above-average returns; but the true measure of its performance is when it posts higher returns than its benchmark and peers during the downturn. Remember: Choose a fund like you choose a spouse - one that will stand by you in sickness and in health.

- Returns: Returns are obviously one of the important parameters that one must look at while evaluating a fund. But remember, although it is one of the most important, it is not the only parameter. Many investors simply invest in a fund because it has given higher returns. In our opinion, such an approach for making investments is incomplete. In addition to the returns, one also needs to look at the risk parameters, which explain how much risk the fund has undertaken to clock higher returns.

- Risk: To put it simply, risk is a result or outcome which is other than what is / was expected. The outcome, when different from the expected outcome is referred to as a deviation. When we talk about expected outcome, we are referring to the average or what is technically called the mean of the multiple outcomes. Further filtering it, the term risk simply means deviation from average or mean return.

Risk is normally measured by Standard Deviation (SD or STDEV) and signifies the degree of risk the fund has exposed its investors to. From an investor’s perspective, evaluating a fund on risk parameters is important because it will help to check whether the fund’s risk profile is in line with their risk profile or not. For example, if two funds have delivered similar returns, then a prudent investor will invest in the fund which has taken less risk i.e. the fund that has a lower SD.

- Risk-adjusted return: This is normally measured by Sharpe Ratio (SR). It signifies how much return a fund has delivered vis-à-vis the risk taken. Higher the Sharpe Ratio better is the fund’s performance. As investors, it is important to know the same because they should choose a fund which has delivered higher risk-adjusted returns. In fact, this ratio tells us whether the high returns of a fund are attributed to good investment decisions, or to higher risk.

- Portfolio Concentration: Funds that have a high concentration in particular stocks or sectors tend to be very risky and volatile. Hence, investors should invest in these funds only if they have a high risk appetite. Ideally, a well-diversified fund should hold no more than 50% of its assets in its top-10 stock holdings. Remember: Make sure your fund does not put all its eggs in one basket.

- Portfolio Turnover: The portfolio turnover rate refers to the frequency with which stocks are bought and sold in a fund’s portfolio. Higher the turnover rate, higher the volatility. The fund might not be able to compensate the investors adequately for the higher risk taken. Remember: Invest in funds with a low turnover rate if you want lower volatility.

- Fund Management: The performance of a mutual fund scheme is largely linked to the fund manager and his team. Hence, it’s important that the team managing the fund should have considerable experience in dealing with market ups and downs. As mentioned earlier, investors should avoid fund’s that owe their performance to a ‘star’ fund manager. Simply because if the fund manager is present today, he might quit tomorrow, and hence the fund will be unable to deliver its ‘star’ performance without its ‘star’ fund manager. Therefore, the focus should be on the fund houses that are strong in their systems and processes. Remember: Fund houses should be process-driven and not 'star' fund-manager driven.

- Costs: If two funds are similar in most contexts, it might not be worth buying mutual fund scheme which has a high costs associated with it, only for a marginally better performance than the other. Simply put, there is no reason for an AMC to incur higher costs, other than its desire to have higher margins.

The two main costs incurred are:

- Expense Ratio: Annual expenses involved in running the mutual fund include administrative costs, management salary, overheads etc. Expense Ratio is the percentage of assets that go towards these expenses. Every time the fund manager churns his portfolio, he pays a brokerage fee, which is ultimately borne by investors in the form of an expense ratio. Remember: Higher churning not only leads to higher risk, but also higher cost to the investor.

- Exit Load: Due to SEBI’s recent ban on entry loads, investors now have only exit loads to worry about. An exit load is charged to investors when they sell units of a mutual fund within a particular tenure; most funds charge if the units are sold within a year from date of purchase. As exit load is a fraction of the NAV, it eats into your investment value. Remember: Invest in a fund with a low expense ratio and stay invested in it for a longer duration.

Among the factors listed above, while few can be easily gauged by investors, there are others on which information is not widely available in public domain. This makes analysis of a fund difficult for investors and this is where the importance of a prudent and unbiased mutual fund advisor comes into play. At Personal FN, we spend a lot of time and effort in short-listing funds which are best for investors, by using various qualitative and quantitative techniques.

This article was written exclusively for Equitymaster, India's leading Independent research initiative. Trusted by over a million members all over the world, Equitymaster is known for its well-researched, unbiased and honest opinions on the Indian Stock Market.

Add Comments

| Comments |

rad_iyn@yahoo.co.in

Mar 29, 2012

Great writeup. Gives a clear idea about the terms which mutual fund investors come across but know little about.

However I am a little skeptical about the so called Risk related Std Deviation.

The Std Deviation generally gives the shift from the average in absolute terms.

To call it as an indicator of risk is conjectural to an extent.

If I understand right, one presumes that the better performance of a Fund is due to it not taking the path taken by the average Fund House. This non average

behavior adopted is classified as Risk

The return on risk or the Sharpe Ratio also becomes a little suspect in the light of what is stated above.

All the same the article is very good.

R V Iyengar |

mp762003@gmail.com

Mar 30, 2012

Very nice article...I must appreciate for putting this stuff with such superior details.

While I seriously liked the content (especially, the way every factor ends with "Remember" tag - the details on what is Sharpe Ratio, Expense Ratio, Standard Deviation), I feel this could have created more impact with its formatting. i.e. Instead of putting down a lot of text and just a text, it could have improvised with a tabular format or using some picture or even putting down the formulas for Sharpe Ratio, Standard Deviation,...etc. Meaning, the article could have been made more interesting to grab more eyeballs.

|

biuro@artbettona.pl

May 10, 2012

A stock index is a number of companions that track the largest 500 companions in the NYSE, American or NASDAQ such as the S P 500 or the Dow tracking the most widely well known companions in the United States or NASDAQ index which is a composite of mostly high tech companions.If you think about it an index can be a mutual fund such as the S P 500 index however an index should have a higher overall value in tracking since the mutual fund will charge a small expense ratio. For tracking purposes it's good to compare a benchmark average for instance the Russell 2000 if your comparing a small company stock or small cap mutual fund the NASDAQ if your tracking your high tech stock or high tech mutual fund. Most mutual fund companions compare to the S P 500 since it has a good mixture of industries and large and mid-cap stocks. In my opinion it's best to invest in the index funds or the total stock market fund since it's instant diversification and has a low expense ratio or invest in sector funds if your hot on certain sectors. Good luck! |

powalekar@gmail.com

Sep 05, 2018

Truely logical, unbiased and well presented thoughts on Investing in Indian scenario. |

1