Company Overview

Manappuram Finance Limited (MFL) is a listed non-deposit taking Non Banking Finance Corporation. (NBFC). MFL is a flagship company of Manappuram group, established in Thrissur (Kerala) in 1992. MFL has been in the business of gold loan financing since 1999 and today, it is the second largest gold loan provider in the country with a gold loan portfolio of more than 2.63 million gold loan accounts with 1.546 million customers aggregating to Rs 85,181.12 million of gold loans in principal amount as on December 31, 2013. The loan amount advanced by the company generally ranges from Rs 1,000 to Rs 1.00 million per loan transaction and typically remains outstanding for an average tenure of 6 months, in the usual gold loan term of 12 months.

As of 31st of March 2013, 99.9% of the Assets under Management (AUM) of MFL comprises of gold loans. With a strong network of 3,295 branches and staff strength of 18,210, MFL is one of the strongest lenders in the gold loan market.

Business Analysis

Apart from providing cash loans against gold pledge, the business of MFL also includes money transfers and foreign exchange services.

The profit after tax of the company declined to Rs 208.4 crores in FY 2012-13 from Rs 591.5 crores in the FY 2011-12. The average ticket size of loans sanctioned is Rs 37,462 as on March 31, 2013). The net Non Performing Assets (NPA) ratio stood at 0.78% (a rise from the March 31, 2012 figure, 0.37%) of the net loans provided as on March 31, 2013. The company is adequately capitalised which is reflected through its capital adequacy ratio of 22.67% (against the 15% prescribed by RBI) as on March 31st 2013.

In order to meet its capital expenditure and working capital requirements, MFL is currently offering Secured Redeemable Non-Convertible bonds of face value of Rs 1,000 each at par having a base issue size of Rs 100 crore, with an option to retain oversubscription of Rs 100 crore, aggregating to a total of Rs 200 crore .

The details of the offering (NCD) are as follows:

| Issuer |

Manappuram Finance Limited |

| Offering |

Public issue of secured, redeemable, non-convertible bonds of face value of Rs 1,000 each, in the nature of debentures by the Issuer, up to Rs 100 crore with an option to retain over subscription up to Rs 100 crore, aggregating to a total of Rs 200 crore |

| Rating |

'ICRA A+' by ICRA |

| Security/ Security cover |

The Bonds shall be secured by mortgage over the immovable property of the Company measuring 2250.64 sq. ft. being the corporate office annex building of the Company, bearing door no. 501, 5th Floor, Aishwarya Business Plaza and two car parking areas, situated in Sy. No. 5589-E, Kolekalyan Village, Santacruz (East), Andheri Taluk, Mumbai Suburban District and a charge in favour of the Debenture Trustee, on all current assets, book debts, receivables (both present and future) as fully described in the Debenture Trust Deed, except those receivables specifically and exclusively charged, on a first ranking pari passu basis with all other lenders to our Company holding pari passu charge over the security such that a asset cover of 100% of the outstanding amounts of the Bonds |

| Face Value |

Rs 1,000 per bond |

| Issue Price |

At par (Rs 1,000 per bond) |

| Minimum Subscription |

10 Bonds and in multiples of 1 Bond thereafter |

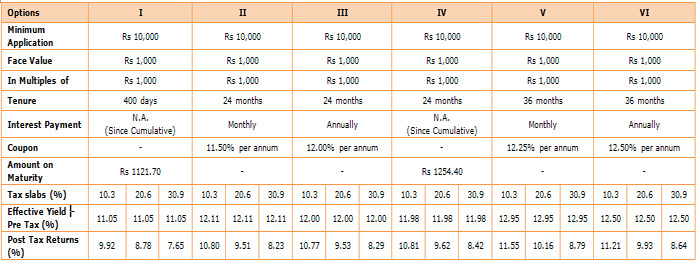

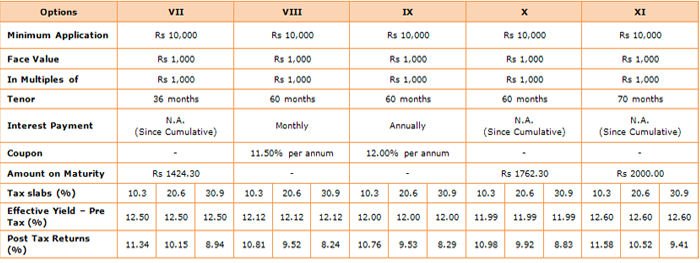

| Tenure |

- Option I: 400 months

- Option II: 24 months

- Option III: 24 months

- Option IV: 24 months

- Option V: 36 months

- Option VI: 36 months

- Option VII: 36 days

- Option VIII: 60 months

- Option IX: 60 months

- Option X: 60 months

- Option XI: 70 months

|

| Coupon rate (For all categories of Investors i.e. Category I, Category II, Category III) |

- Option I: N.A. (Since Cumulative)

- Option II: 11.50% p.a.

- Option III: 12.00% p.a.

- Option IV: N.A. (Since Cumulative)

- Option V: 12.25% p.a.

- Option VI: 12.50% p.a.

- Option VII: N.A. (Since Cumulative)

- Option VIII: 11.50% p.a.

- Option IX: 12.00% p.a.

- Option X: N.A. (Since Cumulative)

- Option XI: N.A. (Since Cumulative)

|

| Trustee |

IL&FS Trust Company Limited |

| Listing |

BSE |

| Depository |

National Securities Depository Limited (NSDL) and Central Depository Services Limited (CDSL) |

| Registrar |

Link Intime India Private Limited |

| Issuance |

Bonds will be issued in both dematerialised and physical form, at the option of the applicant. Trading in the bonds will however take place compulsorily in dematerialised form |

| Issue Open Date |

March 05, 2014 |

| Issue Close Date |

March 25, 2014 |

| Deemed Date of Allotment |

The Deemed Date of Allotment of the Bonds will be the date on which the Board of Directors is deemed to have approved the Allotment of Bonds or any such date as may be determined by the Debenture Committee and notified to the Designated Stock Exchanges. All benefits under the Bonds including payment of interest will accrue to the Bondholders from the Deemed Date of Allotment. Actual Allotment may occur on a date other than the Deemed Date of Allotment. |

| Quota |

Category III - Upto 20% of Overall Issue Size* and Category IV - Upto 50% of Overall Issue Size* |

| Category III (High Networth Individual Category) |

The following investors applying for an amount aggregating to more than Rs 5 lakhs across all Series of Bonds in the Issue:

- Resident Individuals, and

- HUFs Undivided Families applying through the Karta.

|

| Category IV (Retail Individual Category) |

The following investors applying for an amount aggregating up to and including Rs 5 lakhs across all Series of Bonds in the Issue:

- Resident Individuals, and

- HUFs Undivided Families applying through the Karta.

|

Note: (PAN card is mandatory for subscribing to these bonds. A self attested copy shall be enclosed along with the application form.) (*on first come first serve basis to be determined on the basis of the bid uploads made with the scheduled Stock Exchanges) (Source: Issue Prospectus, PersonalFN Research)

Investors will also have the following options available at the time of subscribing to the issue:

(Source: Draft prospectus & PersonalFN Research)

Well, after reading the details of the NCD (as provided above), there may be still some more questions popping up, which are answered hereunder:

- Will I get any tax benefit if I invest in these bonds?

No, these bonds do not entitle you to any tax benefit nor are these any "infrastructure bonds", which make you eligible for an additional tax deduction under section 80 CCF.

- Is interest on these bonds Tax Free?

No, the interest on these bonds is not tax free - it is chargeable to tax. The interest income will be taxed under "income from other sources", and will be brought to tax at the respective income tax rates you fall under. However no tax will be deducted at source as these bonds are issued in demat form and are listed on the exchange.

- What is the Tax Treatment on Capital Gains for these bonds?

If you happen to sell these bonds before 365 days, you will have to pay short term capital gain tax (@ applicable to you as per your tax slab) arising on the profit. Provisions of long term capital gain tax will be applicable for any sale of securities after 365 days. Any long term capital gain on these securities will be taxable @ 10% without indexation benefits or 20% with indexation benefits.

- Can a minor apply to these bonds?

Yes, a minor can apply for these bonds, but only and only through a guardian.

- Can one apply in joint names?

Yes, one may apply in a joint name. However, the demat accounts will also be required to be held in joint name and the order of applicant shall be the same as appearing in the demat account. Moreover, all payments will be made out in favour of the first applicant as well as all communications will be addressed to the first named applicant whose name appears in the application form and at the address mentioned therein.

- Who will get the interest in case of joint application?

In case of joint application, interest will be accounted to the first holder only.

- My demat account is in joint name, but I want to apply is a single name?

In case of a single application, demat account of the same single applicant would be necessary. Joint demat account would not do.

- If I'm an NRI can I invest in these bonds?

No, NRIs are not eligible to invest in these bonds.

- Is there a lock-in period while investing?

No. There is no lock-in period for these bonds. In terms of providing liquidity, these NCDs are proposed to be listed on the Bombay Stock Exchange.

- In whose favour the cheque is to be made?

Cheques /Drafts have to be made in the favour of "MAFIL NCD Escrow" and crossed "A/C PAYEE ONLY". Applicants must write the number of their application form on the reverse of the cheque or bank draft.

OUR VIEW:

PersonalFN is of the view that the yields on investment offered by MFL are attractive. The credit rating too, allotted to the issue is stable ('ICRA A+' by ICRA). Minimum ticket size (minimum investment amount) has purposefully been kept low at Rs 10,000 to encourage the retail participation. Capital adequacy ratio also looks robust at 22.67% as on March 31, 2013.

However, in the recent times the Government has been apprehensive of large gold imports by the country and as such to impede the import of gold, the import duty has been raised to 10% from the earlier 2% at the beginning of the year 2013. But after prescribing a loan-to-value ratio at 60%, the RBI has recently increased the same to 75% vide a notification; which in our view would thrust the business of gold loan NBFCs such as MFL.

NBFCs primarily engaged in lending against gold jewellery (such loans comprising 50% or more of their financial assets) will be required to maintain a minimum Tier l capital of 12% by April 01, 2014. And since, NBFCs do not have restrictions like liquidity reserves and cash reserves; they (NBFC) are exposed to risk arising from depreciation in gold prices or liquidity risks. Thus, investors in NCDs issued by such NBFCs too, are exposed to such risks. Moreover, MFL might suffer from funding constraints due to the regulatory restrictions placed by the central bank on private placement of NCDs by NBFCs. Additional funding might also grow at a sluggish pace owing to the risks in this sector. Although the company has presence in 22 states of the country, approximately 70 per cent of its branches and AUM comes from the southern states. This makes it vulnerable to the risk of concentration.

Thus taking into consideration a holistic view, we believe that investors who wish to invest in these NCDs can opt for a relatively shorter tenure of 12 months - 24 months rather than investing for tenure above 24 months, depending upon their investment holding capacity.

In case you wish to invest in the above instrument, you can email us at info@personalfn.com or contact us on 022-6136 1200

Add Comments