NRI TAXATION - FREQUENTLY ASKED QUESTIONS, ANSWERED

The first thing one might ask as an NRI is ‘Tell me more about my taxation’.

By definition, tax can be tricky.

This tutorial aims to clear up some of the confusion regarding NRI Taxation.

Ahead, we will take you through some frequently asked queries for NRI investors, with regard to their taxation.

Please Note: All of this applies to individual tax payers, and not corporates.

Lets start at the beginning.

Frequently Asked Questions

(Click on the question to go to the answer)

- I have recently come abroad for work / I work on an Indian ship / I am an Indian Citizen, visiting or living abroad temporarily. Do I qualify as an NRI?

- What is the tax incidence on income earned in India, or income earned abroad, for NRIs?

- As an NRI, what is the tax implication if I gift something like cash, property or other assets to a relative who is a Resident Indian?

- I have investments in mutual funds and shares in India and I receive dividend income from them. What is the taxation of my dividend income?

- I have shares which I will be selling soon. How will I be taxed on the sale of my equity shares?

- What about the sale of my mutual funds?

- What is indexation?

- What benefits are available to NRIs under the Act?

- What are the Income Tax Concessions available to NRIs?

- Is there any exemption available to NRIs from long term capital gains? If yes, what are the conditions?

- What are the benefits of Double Taxation Avoidance Agreement for NRIs?

- Are NRIs required to file income tax returns in India?

- What are the procedures and issues involved in filing Return of Income by NRIs in India?

- I am not present in India to file my returns, what are my options?

- What are the consequences of not filing Return of Income by NRI?

- What are the Practical issues faced by a NRI in preparation and filing of Return of Income in India?

- Are NRIs liable to pay Wealth Tax?

- I have recently come abroad for work / I work on an Indian ship / I am an Indian Citizen, visiting or living abroad temporarily. Do I qualify as an NRI?

(Back to top)

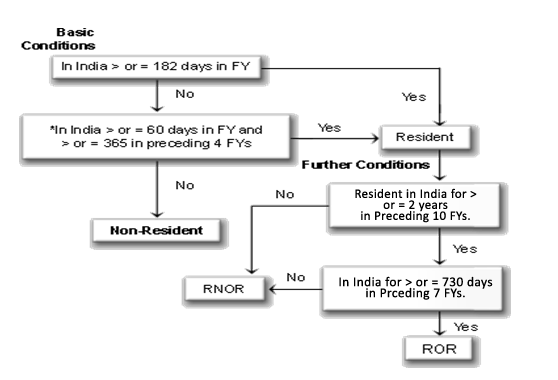

The answer is very simple, and depends on how many days you spend out of India.

From a taxation point of view, you can either be a Resident or a Non Resident.

Further, as a Resident, you can either be Resident and Ordinarily Resident or Resident Not Ordinarily Resident.

To be Resident, you need to fulfill any 1 of the following 2 basic conditions, regarding your time spent in India during the previous Financial Year (01 April to 31 March):

- If you were in India in that year for a single period or multiple periods amounting in all to 182 days or more; or

- If you were in India in that year for a single period or multiple periods amounting in all to 60 days or more AND if you have, within the 4 years preceding that year, been in India for a single period or multiple periods amounting in all to 365 days or more.

If you can’t remember, check your past flight tickets.

There are a couple of exceptions to the rule given above.

Exceptions:

The period of 60 days mentioned above becomes 182 days in case of a Citizen of India who:

- Leaves India in any previous year as a member of the crew of an Indian ship or

- Leaves for the purpose of employment outside India; or

- is a Citizen of India, or a person of Indian origin, and being outside India, comes on a visit to India in any previous year.

So, to be resident in India, you need to meet any one of the above two basic conditions. If you don’t satisfy any of these conditions; you qualify as a Non Resident Indian (NRI).

This tutorial is meant for NRIs, so we won’t go into Resident tax status too much, except to say one more thing:

To be Ordinarily Resident in India, you have to meet both of the following conditions regarding the previous financial year:

- You should have been ‘resident in India’ (as defined above) in 2 out of 10 years preceding that year, and

- You should have been in India for a single period or multiple periods amounting in all to 730 days or more during 7 years preceding that year.

We’re going to wrap up determination of status with an easy chart:

So now that you know whether you classify as an NRI or not, we can move forward to the next question.

- What is the tax incidence on income earned in India, or income earned abroad, for NRIs?

(Back to top)

As an NRI, a common question you may have is whether the income you earn abroad taxable in India. Your taxation for a particular year depends upon your residential status in that year.

The Incidence of tax for different tax payers is summarised as below:

| Residential Status |

Indian Income* |

Foreign Income** |

| Resident and ordinarily resident (ROR) |

Taxable |

Taxable |

| Resident but not ordinary resident (RNOR) |

Taxable |

Not Taxable |

| Non-Resident (NR) |

Taxable |

Not Taxable |

* Indian Income means income which is received in India OR accrues or arises in India.

** Foreign Income means income which is not received in India AND does not accrue or arise in India.

In the case of an ROR, his global income is taxed in India.

In the case of a Non-resident and RNOR, only the income earned or received in India is taxed in India. So, income earned outside India is not taxable in India.

- As an NRI, what is the tax implication if I gift something like cash, property or other assets to a relative who is a Resident Indian?

(Back to top)

There is no restriction on gifts given by Non Resident Indians to Resident Indians whether the gift is in a foreign currency, or Indian Rupees, or in the form of assets (including immovable property).

All gifts from relatives (as per the definition of ‘relatives’ under the Act) are tax free (but get counted as income / assets in the hands of the receiver i.e. the donee).

All that is required is for the giver of the gift (the donor) to offer the gift to the receiver (the done), and the receiver to accept (preferably in writing such as via a thank you note, giving the details of the gift received) in black and white.

To prevent any trouble, the donee can request the donor for the gift (in writing) and then the donor should remit the amount / transfer the asset to the donee. Alternatively, the donor can offer the gift.

In either case, it is necessary for the donee to accept the gift in writing.

To know who qualifies as a ‘relative’, see the chart given below.

- I have investments in mutual funds and shares in India and I receive dividend income from them. What is the taxation of my dividend income?

(Back to top)

Dividends declared by equity-oriented funds (i.e. mutual funds with more than 65% of assets in equities) as well as debt-oriented mutual funds (i.e. mutual funds with less than 65% of assets in equities) are tax-free in the hands of NRI investor.

However, a dividend distribution tax aka DDT (which varies for individual and corporate investors) is to be paid by the mutual fund on the dividends declared by them.

When it comes to shares, dividends distributed by all domestic companies are exempt from tax in the hands of shareholder as the same are taxed as DDT.

But note, dividends received from foreign companies are taxable in the hands of shareholder as the foreign companies are not liable to DDT

- I have shares which I will be selling soon. How will I be taxed on the sale of my equity shares?

(Back to top)

The tax on the income from sale or transfer of shares depends on whether they are a capital asset or stock (business asset). If your investments are business assets (i.e. if you are a trader) then different rules than the ones given here will apply to you. If you are an investor, then the rules that apply to you are as follows:

Equity shares are treated as short-term capital assets if they have been held for less than 365 days. The shares held for more than 365 days then they qualify as long-term capital assets.

Short Term Capital Gain:

If STT (Securities Transaction Tax) has been paid on your short term equity transactions, then they will attract 15% capital gains tax, and if STT has not been paid, they will be taxed as income at the normal tax slabs applicable to you.

Long Term Capital Gain:

If STT has been paid, then capital gains are tax free.

If STT has not been paid, then long term capital gains will attract 20% tax.

- What about the sale of my mutual funds?

(Back to top)

Your mutual fund holdings are treated as short-term capital assets if they have been held for less than 365 days. If the units have been held for more than 365 days, they are treated as long-term capital assets.

Short Term Capital Gain:

When the units in Equity Oriented Mutual Fund are sold (redeemed) within one year of being held by the investor, it becomes short term gains or loss.

The Short term gains are taxed at 15% on gain

When the units in Debt Oriented Mutual Fund are sold (redeemed) within one year of being held by the investor, it is taxed under slab rates applicable to Individual.

Long Term Capital Gain:

When the units in Equity Mutual Fund are sold after holding for more than a year, gains on such units redemption is tax free

When the units in Debt Mutual Fund are sold after holding for more than a year, gains on such units redemption is taxable as Long term Capital Gains. Long-term capital gains on debt-oriented funds are subject to tax @20% of capital gains after allowing indexation benefit, or at 10% flat without indexation benefit, whichever is less.

- What is indexation?

(Back to top)

Indexation benefit is when the cost of the investment is raised to account for inflation for the period the investment is held. This is done by using a Cost Inflation Index (CII) number released by the tax authorities every year.

Let's say that you have invested Rs 1 lakh in a mutual fund on March 30, 2005 and redeemed these units at Rs 1.5 lakh on April 1, 2010.

As per indexation benefit, according to the Cost Inflation Index levels announced by the government every year the cost of acquisition would be deemed to be Rs 148,125 lakh. Your long-term capital gain on this transaction with indexation benefit is just Rs 1,875. The tax liability thus would be 20% on the gain, i.e. Rs 375.

Without indexation benefit, long term capital gain will be Rs. 50,000 and tax liability would be 10%, i.e. Rs. 5,000.

- What benefits are available to NRIs under the Act?

(Back to top)

The following income is exempt from taxation for NRIs:

- Interest on notified securities or bonds and premium on redemption of such securities

- Interest on Non Resident External rupee account (NRE account) / Foreign Currency Non Resident (FCNR) Accounts

- Interest on notified saving certificates subscribed in foreign currency by an Indian citizen/person of Indian origin

- Income from units of Unit Trust of India (‘UTI’) acquired in foreign exchange by Indian citizen/person of Indian origin.

- Interest on non resident non repatriable (‘NRNR’) Deposits and other securities, bonds, savings certificates notified

- Interest from notified bonds (7 year dollar bonds issued by the state Bank of India notified) purchased in foreign exchange, exemption continues even after person becomes resident

- Interest paid by scheduled banks on RBI approved foreign currency deposits

- What are the Income Tax Concessions available to NRIs?

(Back to top)

NRIs are granted a special benefit by way of an option of being taxed at concessional tax rate of 20% as regards investment income and 10% as regards long term capital gains arising from specified assets.

| Particulars |

Flat Tax Rate |

Income from Foreign Exchange Asset (Investment Income).

Long Term Capital Gain other than specified Assets i.e. Immovable Property gain. |

20% |

| Long Term Capital Gain of any specified asset i.e. Foreign Exchange Assets i.e. equity/Debentures. |

10% |

Further, as an NRI you are given a choice, and if you so decides, then only provisions of the above Sections are applicable to you. Otherwise, you will be taxed at par with Residents.

Investment income from specified assets include:

- Interest on debentures of an Indian Public Company

- Interest on deposits with an Indian Public Company

- Income from Securities of Central Government

- Is there any exemption available to NRIs from long term capital gains? If yes, what are the conditions?

(Back to top)

Yes, long term capital gains from transfer of foreign exchange assets (i.e. specified assets referred to above, acquired in convertible foreign exchange) are exempt proportionately, provided the net consideration (net of expenses) is entirely or partly invested in specified assets (as stated above) within a period of six months from the date of such transfer. However, the amount so exempted becomes again chargeable to tax if the new asset is transferred or converted within a period of three years from the date of its acquisition.

So, for example, if you make long term capital gains on the sale of a property, and are therefore liable to pay tax, you can instead invest the net gain proceeds into a notified government security (such as NHAI or REC bonds) with a minimum lock in of 3 years, and save yourself from paying the tax.

- What are the benefits of Double Taxation Avoidance Agreement for NRIs?

(Back to top)

An excellent factor for NRIs is the DTAA.

India has entered into Double Tax Avoidance Agreements (DTAAs) with various countries. Taxability of Indian income for non residents is decided as per the provisions of these DTAAs or as per the Indian Income Tax Act, whichever is more favourable to you.

Most of these DTAAs contain provisions for lower rates of tax in case of dividend, royalties, fees for technical services etc. But your taxability under the DTAA must be ascertained with 100% certainty, because it can sometimes be tricky. We will touch upon this in Question 16 ahead.

- Are NRIs required to file income tax returns in India?

(Back to top)

If you have a tax obligation in India, the domestic tax laws of India requires that you file your IT Return. You may need to file your Returns in India under the following circumstances:

- The India-sourced income exceeds the maximum amount chargeable to tax for the relevant previous year thus resulting in liability to pay taxes in India;

- Claiming refund of taxes where taxes withheld are in excess of tax liability;

- To enable you to claim DTAA benefits in the country of your residence i.e. the country in which your global income is consolidated and taxed

- To become tax compliant under the IT Act.

- What are the procedures and issues involved in filing Return of Income by NRIs in India?

(Back to top)

- The first step to filing the Return would be making an application for allotment of Permanent Account Number (“PAN’) in a prescribed Form (No. 49A). Earlier the application for PAN was required to be made only in physical form but now PAN can be applied online through website from anywhere in the world. The PAN is to be quoted in all correspondences relating to Indian Income Tax including your IT Returns.

- Remember to choose the appropriate form based on the source of income. The available forms are:

| ITR1 |

For Individuals having Income from Salary/ Pension/ family pension & Interest |

| ITR2 |

For Individuals and HUFs not having Income from Business or Profession |

| ITR3 |

For Individuals/HUFs being partners in firms and not carrying out business or profession under any proprietorship |

| ITR4 |

For individuals & HUFs having income from a proprietary business or profession |

- I am not present in India to file my returns, what are my options?

(Back to top)

Presently there are two options available to you as an NRI to file your tax return viz. Electronic filing or Physical filing.

Under Electronic filing, you will have to get the tax return uploaded on the Income Tax website with a Digital Signature

(NB: Digital signature is required to be separately obtained from specified Digital Signature Issuing Authorities).

However if the file is uploaded without a digital signature, you will have to print Form ITR-V and submit the same with the Return physically.

In such cases, the process of filing return will be completed only on physical filing of ITR-V.

Under Physical filing, you will have to file the respective ITR form along with the Acknowledgment form with the Income Tax Officer.

The return needs to be signed and verified by you personally or if you are absent from India, then by a person duly authorized by you in this behalf. In this case, the person signing the return should hold a valid PoA (power of attorney) from you, which should be attached to your IT return.

- What are the consequences of not filing Return of Income by NRI?

(Back to top)

If you file your returns after the last date of filing Return of Income, you will be charged interest at the rate of 1% of the tax payable per month of delay. Also, if such a return is filed after one year from the end of the tax year concerned, apart from the interest, you will also be liable for a penalty of Rs 5,000.

The due date of filing the return of income by a NRI is July 31. However, if you are a working partner of a firm whose accounts are required to be audited, then the due date is September 30.

- What are the Practical issues faced by a NRI in preparation and filing of Return of Income in India?

(Back to top)

- Examining the DTAA applicability

The first practical issue that can be faced is if you are earning in a country that comes under DTAA Benefit – The financial tax years of these other countries are usually different from the financial year of India (See illustrative table below).

| Country |

Tax Year |

| India |

April 1 to March 31 |

| United Kingdom |

April 6 to April 5 |

| Australia |

July 1 to June 30 |

| Germany, Switzerland, Denmark |

January 1 to December 31 |

Your residential status needs to be examined very carefully to ascertain whether DTAA benefit applies or not. Peculiar situations could arise as you could be a resident of both countries or a non resident of both countries as per the DTAA (this is possible in case of highly mobile employees) for a particular period of the tax year.

Where you are a resident of both countries, the residential status for the purposes of the tax treaty is determined by applying the ‘tie breaker’ test in the DTAA. This is essential, since the country of residence relieves the burden of double taxation by giving either the credit for taxes paid in the source country or the country in which the individual is not a resident.

On the other hand, if you are considered to be a non resident of both countries, you are not entitled to the DTAA benefits and thus you will be governed by the respective domestic tax laws of those countries relating to residence and taxability.

- Ascertaining Jurisdiction

If you are outside India, for you to ascertain the right jurisdiction where your return is required to be filed can sometimes pose a challenge. In most of the cities in India, dedicated international jurisdiction is available for filing of the Return of Income by NRIs. However, this may get smoothened with gaining popularity of online filing through websites.

- Address

A local Indian address is required to be provided in the Return of Income. This poses a problem since the NRIs who visit India for a short period find it difficult to find a local address to be given in the Return of Income. To overcome this problem, generally the address of the local office in which the NRI works can be mentioned in the Return of Income.

- Bank details

It is mandatory to provide Bank Account details in the Return of Income in case of claim for refunds. NRIs who are visiting India for a short period do not intend to open a Bank Account in India but are forced to open Bank account in India only for tax compliance

- Physical filing of Return of Income

If the return is intended to be filed physically and you are outside India, verification and signing of the Return of Income poses a problem as, in such circumstances, return needs to be signed and verified by you or by some person duly authorized by you in this behalf.

Where a person is duly authorized, such person signing the return should hold a valid power of attorney from you which should be attached to the Return of Income.

- Are NRIs liable to pay Wealth Tax?

(Back to top)

This depends mainly on your residential status. Let’s see why.

The Wealth Tax Act specifies that the residential status for the purpose of Wealth Tax will be same as the residential status for the purpose of the IT Act.

This also depends upon the Citizenship of a person. In order to be a citizen of India, you must have domicile in the territories of India and must fulfill any of the following conditions:

- You must have been born in India;

- Either of your parents must have been born in India;

- Before the formation of Republic i.e. 26th January 1950, you must have been ordinarily resident in India, for a period of 5 years.

While the third condition might not apply to you, you must fulfill one of the first 2 conditions stated above to be qualified as an Indian citizen.

A person ceases to be a citizen of India if he voluntarily acquires the citizenship of a foreign nation.

How does this apply to Wealth Tax?

Like this:

| Citizen of India |

Non-Citizen |

If you are "resident & ordinarily resident", your assets and liabilities located anywhere in the world are chargeable to wealth tax in India.

In any other case, only those of your assets and liabilities that are located in India are chargeable to wealth tax in India. |

In this case all your assets and debts located in India are taxable, irrespective of whether you are a resident, a non-resident, or not ordinarily a resident. The value of all assets and debts located outside India are exempt here. |

There’s a point to note here. If you are a returning NRI / PIO, (an NRI / PIO returning for permanent residence to India), then you are exempt from wealth tax on your monies and the value of those assets that you bring to India, and also the value of assets that you acquire out of these monies, within 1 year immediately preceding the date of your return and at any time thereafter. These monies and assets are totally exempt from wealth tax for a period of 7 years after your return to India. After 7 years post your return, they become taxable under Wealth Tax

Conclusion :

So now you are aware of the answers to most frequently asked questions regarding taxation, such as how to know if you are an NRI, what is the taxation of your investments, what are the benefits, concessions & exemptions available to you as an NRI, what are the practical issues you might face as an NRI filing your taxes, and are you liable to pay Wealth Tax.

Please keep in mind that taxation is a tricky subject and is best done by a professional such as your CA. Also note that tax rules change from time to time, the above tutorial has been written taking into account tax rules as on December, 2010.

Want to do a financial plan for yourself, or

Want to know more about or invest in mutual funds, insurance, fixed income instruments

Our Investment Consultant will be glad to help you.

Contact Us NOW!

Mumbai

+91 - 22 - 6136 1221 / 22 |

Chennai / Bangalore

+91 - 44 - 6526 2621 / 22 |

Pune

+91 - 922 - 325 4864 |

Or Simply write in to us : info@personalfn.com

*Please note: Quantum Information Services Pvt. Ltd (PersonalFN) does not serve US / Canada based NRIs, and persons holding US citizenship.

Add Comments

| Comments |

ruchibansal1190@gmail.com

Aug 24, 2012

excellent guidance on this matter as i was about to file NRI return |

girishjjain@hotmail.com

Dec 31, 2010

Excellent tutorial and very helpful for a lot of people and not just NRIs. For example, in my case, I came to know that my residential status as per IT Act is ROR and my global income is taxable in India. This tutorial mainly targeted NRI taxation related queries. Since a large number of Indian people go abroad for working, it would be highly appreciated to have another article on taxation related queries for such Indian workers who work abroad and how DTAA plays a part in their tax liability. |

vanita.badugu@gmail.com

Feb 24, 2014

Very useful information helped me for giving presentation in my college!!!! |

varuntejindia@gmail.com

Jul 13, 2015

great article about Nri taxation thanks to shared this informative article. |

carakhecha@yahoo.com

Jun 29, 2011

Wow ! It is wonderful sharing on NRI Taxation. Thanks and Congratulations to the Author. |

1