India’s GDP growth for Q1FY18 fell to a dismal 5.7% (a 3-year low) as against 6.1% in the previous quarter. The Gross Value Added (GVA)––—a refined parameter which excludes taxes and subsidies–– too dwindled to 5.6% from 6.6% in the last quarter, significantly lower than 7.6% a year ago. And now to revitalise economic growth, the Government is batting for a policy rate cut.

But will the Reserve Bank of India (RBI) budge; is there real scope for monetary easing?

Well, let’s take stock of the macroeconomic situation to get the answer…

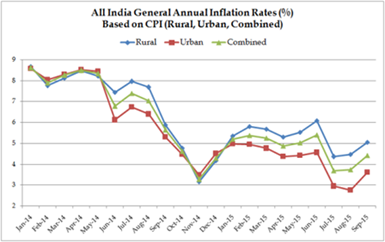

- Retail inflation (as measured by the Consumer Price Index (CPI)) has inched-up for the second consecutive month in August 2017 to 3.36% from 2.36% a month ago, as the Consumer Food Price Index (CFPI) reported a positive reading (of 1.52%) after three months of contraction.

CPI Inflation Treading Up

(Source: Ministry of Statistics and Programme Implementation)

The price revision post-GST, the disentangling of the structural and transitory factors shaping food inflation, and the favourable base effect waning; appear to have shown bearing on headline inflation.

So, the assessment made by RBI in the 3rd bi-monthly monetary policy statement for 2017-18, stating that “while inflation has fallen to a historic low, a conclusive segregation of transitory and structural factors driving the disinflation is still elusive” seems to have been proven true. Plus, the central bank was right in noticing that price of inflation-sensitive vegetables are recording spikes. Thus, expecting the trajectory of inflation in the baseline projection to rise from current lows, the Monetary Policy Committee (MPC) maintained a ‘neutral’ stance and decided to watch the incoming data.

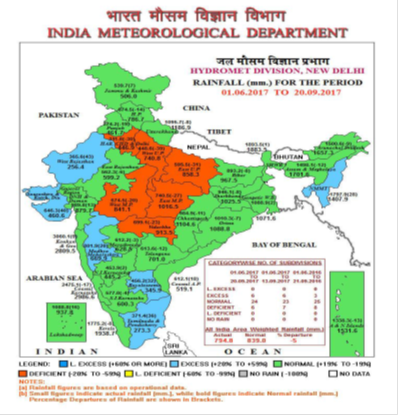

How Has 2017 Southwest Monsoon Been?

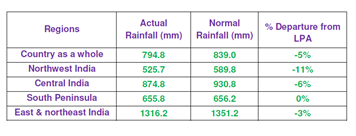

- The southwest monsoon this year so far is near-normal. As on September 20, 2017 the deficit was 5% for the country as a whole (All India Actual: 794.8 mm, Normal: 839.0 mm) and the rainfall distribution among the four broad homogenous regions of India as on September 20, 2017 is as under:

(Source: India Meteorological Department)

Out of the 36 subdivisions, rainfall has been large/excess in 6, normal in 24, and deficient/largely deficient in 6 according to the IMD. The Department is confident that rainfall this year will be 95%-96% of the Long-Period Average (LPA) before the withdrawal of southwest monsoon in a few days from now. Farmers who pin hopes for a good rainfall for kharif sowing, have witness their crops being wash away amid floods in some regions, while some have grieved on account of deficiency in respective regions.

| Crop |

Area sown in 2017-18

(in lakh hectare) |

Area sown in 2016-17

(in lakh hectare |

| Rice |

371.46 |

376.89 |

| Pulses |

139.17 |

144.84 |

| Coarse Cereals |

183.43 |

186.06 |

| Oilseeds |

169.20 |

187.16 |

| Sugarcane |

49.88 |

45.64 |

| Jute & Mesta |

7.05 |

7.56 |

| Cotton |

120.98 |

101.72 |

| Total |

1041.17 |

1049.87 |

(Source: Ministry of Agriculture)

As per the data released by Ministry of Agriculture, the total sown area as on September 8, 2017 stands at 1041.17 lakh hectare as compared to 1049.87 lakh hectare at the same time last year.

- The fiscal deficit data from the Comptroller and General of Accounts (CGA) shows that during the first four months, i.e. April 2017 to July 2017, it had touched 92.4% (or Rs 5.05 trillion) of the budgeted estimate (of Rs 5.46 trillion) for the current fiscal year, as against 73.7% of the budgeted estimates during the same period last fiscal. The increase in Government expenditure was on account of early presentation of the budget and the subsequent front-loading.

Now, in order to reinvigorate economic growth, the Government is considering upto Rs 50,000 crore stimulus package. But if this is injected, in all likelihood the fiscal target of 3.2% for the current fiscal year could get derailed. In addition, the apex bank has mentioned that the implementation of farm loan waivers by States may result in possible fiscal slippages and undermine the quality of public spending, entailing inflationary spillovers.

Of the disinvestment target of Rs 72,500 crore, the Centre has raised only around Rs 8,800 crore so far. The disinvestment process of Air India has begun, and the Government is trying to sell a majority stake. But unless this big ticket strategic disinvestment isn’t completed by the end of the current financial year, achieving the said disinvestment target will be a herculean task, more so now, when economic growth is dwindling.

Besides, the current glitches in the implementation of GST could weigh down on indirect tax collections if these aren’t addressed soon.

- The Indian rupee has passed by the 65 mark against the US dollar, and appears vulnerable. The country’s Current Account Deficit (CAD) has widened to a four-year high of US$ 14.3 billion (or 2.4% of GDP) in Q1FY18 owing to higher imports than exports. But abetted by strong inflow of capital, the foreign exchange reserves are respectable (US$ $402.5 billion as on September 22, 2017). The World Bank observes India’s external dynamics to remain very favourable given the size of its economy and foreign reserve holdings. However, a prolonged period of unfavourable trade balance along with volatile international capital flows could lead to unpleasant macroeconomic situations. High levels of stress in twin balance sheets, banks and corporations, are likely to deter new investments.

How Have Government Bond Yields Reacted?

Data as on September 25, 2017

(Source: RBI, PersonalFN Research)

The 10-Year G-sec yield has hardened over the past few days. Since the start of September 2017, it has moved up 16 basis points (bps) and from the time of RBI’s 3rd bi-monthly monetary policy 2017-18, by 18 bps. The Gsec yield is currently hovering near the overnight rates seen before the August rate cut.

What will RBI do in the October Policy?

Based on this backdrop, in our view, it appears unlikely that the RBI will reduce policy rates in its 4th bi-monthly monetary policy statement for 2017-18 scheduled on October 4, 2017. At present, borrowing cost has come down as a result of transmission of policy rates. So, for now, the central bank may maintain a status quo on policy rates in its October 2017 policy, and only in the December 2017 policy (i.e. 5th bi-monthly monetary policy statement for 2017-18 scheduled on December 6, 2017) reduce policy rate looking at the inflation trajectory (along with macroeconomic variables). By then, the outcome of the southwest monsoon will also be clear.

The central bank, instead, will continue to take liquidity measures and focus on resolving the NPA problem. On their part, the Government and the Reserve Bank are working in close coordination to resolve large stressed corporate borrowers and recapitalise public sector banks within the fiscal deficit target.

To jumpstart the slump in economic growth, the MPC has expressed urgent need to reinvigorate private investment, remove infrastructure bottlenecks, and provide a major thrust to the

Pradhan Mantri Awas Yojana for housing needs of all. This hinges on speedier clearance of projects by the States. We believe, RBI in the 4th bi-monthly monetary policy statement for 2017-18, would lower its growth forecast for India from current 7.3%.

What should the investment strategy be to invest in Indian debt market currently?

Primarily, prudent selection of the category of debt mutual funds is crucial.

Currently, investing aggressively at the longer end of the yield curve could prove imprudent. To put it simply, investing in long-term debt funds (holding longer maturity debt papers) can be perilous, since most of the rally has been captured already at the longer end of the yield curve and there’s not much steam left.

So, preferably, invest vide dynamically managed bond funds (with an investment time horizon of 2-3 year). This would be a prudent approach.

You’ll also be better off if you deploy your hard-earned money in short-term debt funds; but ensure to give due importance to your investment time horizon, asset allocation, and diversification. Consider investing in short-term debt funds for an investment horizon of upto 2 years.

If you have an investment horizon of 3 to 6 months, ultra-short term funds (also known as liquid plus funds) would be the most suitable.

And if you have an extreme short-term time horizon (of less than 3 months), you would be better-off investing in

liquid funds.

Don’t forget that investing in debt funds is not risk-free.

Therefore consider the 5-facets while investing in debt funds.

Some other options to invest in debt instruments are tax-free bonds, especially if you are in the highest tax bracket and able to subscribe to the bonds in the primary market (as and when they are offered). Currently, there are no tax-free bonds available for subscription in the primary market, but as the financial year draw to a close, you may find quite a few.

A few highly rated corporate deposits and bonds may also

yield better returns than bank Fixed Deposits. But, make sure you study the company’s financials before investing, as the risk of default can’t be ignored. This will save you from the financial shocks.

A sensible and astute investment strategy paves the path to wealth creation. It is always

beneficial for your long-term financial wellbeing.

Add Comments