Uncertainties have caught fund managers off guard yet again.

The default by a subsidiary of IL&FS has created a huge redemption pressure on debt mutual funds.

[Read: How IL&FS Rating Downgrade Will Impact Your Mutual Funds]

Restless investors, especially the large institutional investors, have pressed the panic button. They are ready to exit the market until the situation improves to curtail their losses on account of another potential default.

The AMFI (Association of Mutual Funds in India) has been trying to persuade the SEBI (Securities and Exchange Board of India) to permit mutual fund houses to elevate this problem by ‘side pocketing’ as a way to safeguard small investors.

What is side-pocketing?

In layman terms, side pocketing is an accounting method of calculating two Net Asset Values (NAVs) of a scheme by demarcating good assets from troubled assets. Redemptions and purchases are allowed only through the bucket of good assets.

As and when the issues of troubled assets are resolved, investors can liquidate their holdings in that bucket as well.

Does the AMFI have the interest of investors at heart?

It doesn't look like it does.

In fact, this isn’t the first time the mutual fund industry body has projected side-pocketing as “a pragmatic and a practical way to minimize stress.” However, this time around it’s a proposal "with a positive approach".

When malpractices are the white elephant in the room, the approach of side-pocketing can’t hide it under a table.

If you remember, the mutual fund industry faced a risk of deteriorating credit quality in the past as well. The episodes of Amtek Auto and Jindal Steel and Power Limited (JSPL) gave mutual fund houses sleepless nights. Hoping to curb the reoccurrence of such cases, mutual fund houses approached the SEBI with a request to permit the creation of a ‘side pocket’.

Back then, the capital market regulator had declined the practice of side-pocketing, because it believed such practices would encourage fund managers to take unwarranted risks.

[Read: SEBI Discourages Mutual Funds From ‘Side-pocketing']

Have mutual fund houses learned from their past mistakes?

Unfortunately, the current scenario proves that they haven’t.

The last time the question of side-pocketing was in the limelight, mutual fund houses were chasing higher returns. Their exposure to “A” rated bonds had risen sharply and there was a gradual decline in their exposure to “AAA” bonds.

(Image source: pixabay.com)

Now they seem to have taken the whole ecosystem for granted, which is even worse.

Although it’s true that IL&FS enjoyed ‘AAA’ rating until recently and this was a comforting factor for many fund houses to invest in its subsidiaries, couldn’t they have conducted intensive research independently?

When subsidiaries of IL&FS ventured into unchartered business verticals, their prospect suffered due to regulatory delays, and their balance sheets weren’t strong enough to justify their borrowings. Yet the mutual fund house loaned them money.

The only plausible explanation for this could be the strong shareholding profile of IL&FS.

So were fund managers taking the promoters of IL&FS for granted?

The deeper you dig, more startling facts surface...

When there was ample liquidity in the market post demonetisation, many fund houses mopped up a large chunk of it through debt funds.

In the quest for good returns, they invested aggressively in credit instruments issued by Non-Banking Financial Companies (NBFCs).

SEBI had also hiked the additional exposure limit in the financial services sector from 10% to 15%, over and above the sectoral threshold of 25%, post demonetisation.

Since NBFCs were growing at a brisk pace, thanks to higher growth in the retail segment, mutual funds found a haven in most of the NBFCs and companies engaged in the financial services.

Assumption of mutual funds (looking at their investment decisions) that went wrong:

- The tsunami of liquidity the banking system experienced post-demonetisation was durable.

- Interest rates would stay low for a longer duration.

- Retail loan growth was permanent without many hassles on the asset quality firms.

- Credit rating agencies were efficient enough to spot any trouble in a timely manner, hence were highly (and perhaps entirely) reliable.

- There wouldn’t be redemption pressures since investors of fixed income assets won’t have many alternatives to park their money.

For all the reasons given above, mutual funds aggressively pushed debt funds in the post demonetisation phase.

It isn’t unreasonable to say that the fund houses are taking half-measures while managing the investors’ hard-earned money.

When a liquid fund losses more than 7-8% in couple of weeks, all allegations seem warranted.

[Read: Why Your Money In Liquid Funds Is At Risk]

On this background, side-pocketing appears to be an escape route for mutual funds.

What might possibly go wrong with side-pocketing if it was made official?

- First and foremost, the practice of side-pocketing is followed by hedged funds (in the western countries) and not by mutual funds. There’s no reason to believe that the Indian mutual fund industry needs any such special treatment.

- SEBI has created 16 categories of debt funds and has directed mutual funds to classify all their products accordingly. The categories are comprehensive enough to segregate mutual fund schemes on the parameters of duration and credit quality. Thus, any inconsistency in the portfolio of a debt scheme is unwarranted.

- The practice of side-pocketing could create moral hazards. Let’s suppose, a mutual fund scheme was to use the side-pocketing approach in the near future, and this news leaked out to only a handful investors; wouldn’t it be unfair to small-time investors? Can a mutual fund give in underwriting that none of its investors were privy to this information beforehand? That would indeed be very difficult.

What’s the real problem and how can they address it?

Some mutual fund houses with a good reach and a fairly big fund management team will curb their appetite to growth their Assets Under Management (AUM) during good times.

The IL&FS episode, often termed as the Lehman Brothers crisis of India, wouldn’t have happened if mutual funds had taken prudent risk management measures.

Lack of common sense or overconfidence in one’s abilities?

Do you need credit rating agencies to tell you that a cash-strapped and ill-capitalised entity such an IL&FS, which has an outstanding debt of over Rs 93,000 crore, would face a trouble someday?

To avoid the situation that mutual funds are in today, they need to develop a strong credit evaluation system, independent of credit rating agencies. Many of them might claim that they already have one in place, but the reoccurrence of such fiascos make it hard to trust their claims.

What can investors learn from the recent IL&FS episode?

- Never chase returns; always consider risks associated with them.

- Never invest in a debt fund that has generated higher returns in the past, ignoring risks.

- Always consider your time horizon and risk appetite before investing in a debt fund.

- All your investment decisions must align with your financial goals and personalised asset allocation based on them.

- Be selective about mutual fund schemes and invest in them only after evaluating all the available options.

Choosing a right mutual fund scheme isn’t easy, but that’s not impossible for you either. You should evaluate mutual fund schemes on various

quantitative and qualitative parameters. And invest only in the ones with bright prospects.

Editor’s note:

Want to add SOLID mutual funds to your portfolio that could help you create wealth in the long run but don’t have time and skills to select worthy mutual fund schemes? Don’t lose heart.

PersonalFN's unbiased premium research service—FundSelect is meant to assist investors in selecting worthy mutual fund schemes.

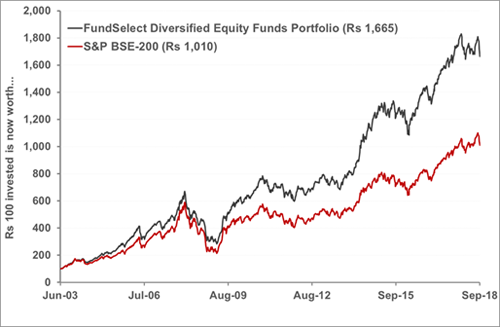

Performance as on September 28, 2018; Past performance is no guarantee of future results

(Source: ACE MF; PersonalFN Research)

With FundSelect, you get access to high quality and reliable funds picked by our research team using their comprehensive S.M.A.R.T. score fund selection matrix.

S – Systems and Processes

M – Market Cycle Performance

A - Asset Management Style

R - Risk-Reward Ratios

T - Performance Track Record

So if you are serious about investing in a rewarding fund, try PersonalFN’s flagship mutual fund research service FundSelect.

Every month, PersonalFN’s FundSelect service will provide you with an insightful and practical guidance on equity funds and debt schemes – the ones to buy, hold, or sell, therefore assisting you in creating the ultimate portfolio that has the potential to top the market. Subscribe to FundSelect today!

Happy Investing!

Add Comments