|

| December 12, 2014 |

| |

| Weekly Facts | | | Close | Change | %Change | | BSE Sensex* | 27,350.68 | -1107.42 | -3.89% | | Re/US$ | 62.35 | -0.41 | -0.66% | | Gold Rs/10g | 27,100.00 | 700 | 2.65% | | Crude ($/barrel) | 63.73 | -5.99 | -8.59% | | FD Rates (1-Yr) | 7.75% - 8.90% | Weekly change as on on December 11, 2014

*BSE Sensex as on December 12, 2014 |

Impact

Recently, some of India's prominent banks such as SBI, Axis Bank and HDFC Bank reduced interest rates on deposits in the range of 0.25% to 0.75% for various tenures. The move was consequent to a dovish tone adopted by the Reserve Bank of India (RBI) in the guidance to 5th bi-monthly monetary policy statement, 2014-15. But this has left many risk-averse investors to wonder, as to where they should park their hard earned money in the endeavour to earn a fixed rate of interest.

Well, there is an alternative...

You see, corporates are actively borrowing from the open market, offering investment instruments such as Non-Convertible Debenture (NCD) and Fixed Deposits (FDs). And you may be surprised to know that the rate of interest offered on such instruments is even higher (of course, depending on the investment tenure one opts for). But on an average, the spread is in the range of 0.9% to 1.0%.

<>bSo, should you indulge in corporate FDs?

Before you get lured by higher interest rates offered by corporates, you must delve to know why a company is sourcing money from you as a debt as against seeking recourse from a bank, especially in a scenario where policy rates are likely to descend going forward. Having said this, there are a few strong companies that have sound fundamentals and they float public deposit schemes. Yes, there are some technical reasons why companies go directly to public, but that is not a case always.

It is noteworthy that many a time, companies paying higher rate of interest on your deposits find it difficult to secure bank loans. You see, banks have certain parameters of credit assessment which some companies do not comply with, and thus they try to raise money through other routes.

So, before you get enticed by high rate of interest offered by a company, you need to assess the following parameters as well.

- Purpose of raising money: It is not very uncommon to see financially weak companies accepting fixed deposits at higher rates to retire their old debts. Such companies may not be safe for you as money raised from you is unlikely to be used in any productive way. There’s no guarantee that retiring old debt will help in improving the balance sheet. Similarly the companies raising money to meet working capital requirements may also be under financial stress and thus not ideal for investment.

- Current debt on books and Credit history: It is important for you to carefully analyse the past track record of the company in servicing debt. You must assess how a company has used debt it raised in the past and how much value it has added to its business. Successful track record on this front would mean that the company has been efficient not only in servicing debt but also in making optimum use of resources.

- Predictability of future earnings: Under normal circumstances, the debt is served through profits earned through business activities. Hence it is imperative for you to know if the profits of the company are predictable. Sensitivity of the business to the performance of economy or cyclical nature of its business may make the company vulnerable in a cyclical downtrend and may put strain on its finances.

Although credit ratings given by independent rating agencies take all the above mentioned aspects into consideration before awarding any rating to the company; you should not depend only on credit ratings given by them. In case the scheme which you are considering for investments are rated by any independent rating agency, you must check the past record of the rater as well. Usually, it is the company which pays for the services offered by the agency.

PersonalFN is of the view that while corporate FDs are offering a higher rate of interest, you should invest in them only if you are having a little high risk appetite and after you have done a prudent assessment. These days, when even banks are finding it difficult to recover their dues from borrowers and have been restructuring loans worth thousands of crore; you, as an individual, may not be well place to handle any situation where the company has not paid interest or principal or both.

Remember, role of fixed income bearing instruments in your portfolio is not to maximise profit, but capital preservation along with generating a regular flow of income.

Do you think it is safe to invest in company fixed deposits for earning a little higher rate of interest? Share your views

|

Impact

Often retail clients or customers walk out of bank disgruntled and disgusted with the service offered... and sometimes even with the way they are treated. Partial treatment, lack of sound of sound knowledge on the part of the relationship manager, inadequate interpersonal skills, unethical practices and archaic administration practices often irks many of us as customers of banks. But now RBI seems to be taking cognisance of this, and soon customer service at a bank may turn to be 'customer delight’

RBI is thinking of launching a model code of conduct for banks in India. In consultation with Banking Codes and Standards Board of India and Indian Banks’ Association, banks would have to develop a model code keeping customers’ rights in mind. RBI would closely monitor the progress of banks in complying with the model code.

The model code is likely protect following rights of customers of banks

- Right to fair treatment

- Right to transparency

- Right to fair and honest dealing

- Right to suitability

- Right to privacy

- Right to grievance redressal and compensation

PersonalFN believes, the introduction of new model code would be a boon for clients or customers of banks, especially the retail or smaller ones who have often been partially treated. This would give them better defence for protection of their rights. The code would not only help keep check in unwarranted behaviour of bank employees towards customers (whenever such incidence take place in deed), but also work in interest of banks as well, if they indeed transform their service to 'customer delight’. You see, the model code may enforce banks to serve their customers with courtesy which may help them create brand loyalty.

|

Impact

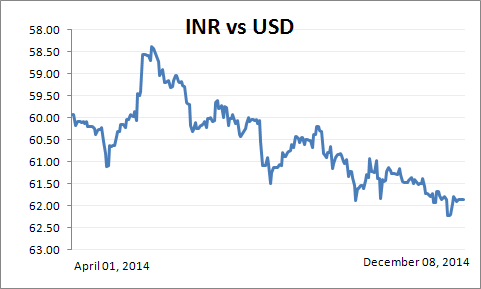

While patients suffering from diseases show symptoms, it is equally true that some of the symptoms emerge at a much later stage. In finance and economics the health of an economy is often gauged through resilience country’s currency depicts. But sometimes, strength or weakness of a currency can be disguising.

So while the Indian Rupee (INR) has shown resilience against the greenback, let us understand whether the value of rupee is disguising or there are genuine and fundamental reasons that support the rupee.

Rupee Domination

If Financial Year (FY) 2012-13 and FY 2013-14 were the years of debasement for the INR, the present fiscal has been a year of consolidation for INR. In the fiscal so far, INR has emerged as one of the strongest emerging market currencies against U.S. Dollar (USD).

How has the Indian rupee fared

| | Currency | Performance against USD | | | From 01-Apr-2014

To

08-Dec-2014 | | Indian Rupee | -3.2% | | Turkish Lira | -6.1% | | South African Rand | -8.4% | | Indonesian Rupiah | -9.5% | | Brazilian Real | -14.4% | | Russian Rouble | -49.3% | | Data as on December 08, 2014

(Source: Bloomberg.com, ACE MF)

So, let’s recognize that what has resulted in the Indian rupee to be moving in a narrow range...

The Federal Reserve (Fed) in the U.S. ended the bond-buying programme in October 2014 believing that U.S. economy was set to get back on track. It was also anticipated that, the labour market conditions may improve going forward. And as expected then, job market data for November 2014 has been robust, with the unemployment rate having reduced to 5.8% and jobless claims dropped to a 6-year low. The U.S. has not only seen improvement in hiring but has also witnessed wage hikes. Such signs of economic vigour depicted by the U.S. economy has pushed USD to a 5-year high.

To read more about this news and PersonalFN’s views on it, please click here.

|

Impact

These days, you must be busy buying New Year gifts for your friends, relatives and loved ones. After all, New Year brings a new ray of hope and the passing year leaves you with a lot of things to learn from. Although buying gifts for others gives you immense pleasure, it might put some strain on your finances if you are picking the expensive ones. Managing finances is a critical aspect of one's life nowadays. Most of people, especially, those leaving in bigger cities, are often burdened with sizeable loans taken for buying home. If rate of interest, under floating rate system goes down even by 0.5%, you may be able to save a hefty amount if size of your loan is high. Here's some good news for you if you are a borrower. Banks might cut borrowing rates soon.

To know more about this story and to read our views, please click here

|

Just Released: 10 Steps to Select Winning Mutual Funds

The latest issue of our extremely popular Money Simplified Guides - 10 Steps to Select Winning Mutual Funds offers you a step-by-step approach to select winning mutual funds...

... And thereby it helps you build a robust mutual fund portfolio that can help you achieve your life's goals.

Click here to claim your FREE copy now... | |

- Recently, the Government agreed on lowering its stake in Public Sector Banks (PSBs) to 52% in a phased manner.

This move is expected to fetch banks nearly Rs 1,60,000 crore which would be utilised to increase the capital base of banks. Basel III norms on capital adequacy would be applicable from March 31, 2019. It was found that PSBs may need roughly Rs 2,40,000 crore by 2018 to be able to comply with Basel III norms. This means, the Government will have to provide budgetary support of nearly Rs 80,000 crore. However, considering the fact that, the Government would receive dividend from PSBs, it would limit the total outgo to a much lower amount.

PersonalFN is of the view that, stake sell by the Government may attract huge buying interest considering the reach and penetration of PSBs. However, PersonalFN cautions investors that, speculating on the stock prices may be detrimental to their portfolio. PersonalFN is of the view that, investors shouldn’t invest in sector funds focused on a specific theme or a sector, instead it would wise to take advantage of such opportunities by investing in Opportunities style mutual fund schemes.

|

Credit Spread: The spread between Treasury securities and non-Treasury securities that are identical in all respects except for quality rating.

(Source: Investopedia)

|

Quote : "In stocks as in romance, ease of divorce is not a sound basis for commitment." - Peter Lynch

|

| |

| © Quantum Information Services Pvt. Ltd. All rights reserved.

Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Pvt. Ltd. 101, Raheja Chambers, 213, Nariman Point, Mumbai - 400021. Tel: +91 22 6136 1200

Website : www.personalfn.com CIN: U65990MH1989PTC054667 |