From liquidity deficit, the Indian banking system has moved to relatively comfortable position-- thanks to the deposits post

demonetisation.

But in the absence of vibrant credit demand, the excess cash has now started to create a problem, disrupting the Indian bond market. Banks aggressively invested in sovereign bonds and even placed money into reverse repos — a window through which banks park their surplus liquidity with the Reserve Bank of India (RBI) and earn interest on it. Besides, they also

invest in liquid funds to fetch a tad higher returns vis-à-vis reverse repo

But the central bank recently asked banks to maintain an ‘incremental Cash Reserve Ratio’ (CRR) of 100% on increased Net Demand and Time Liabilities (NDTL) between September 16, 2016, and November 11, 2016. In other words, banks will be forced to hold a bulk of the fund flows they receive for the time being. The ‘incremental CRR’ is a short term arrangement which, RBI says, would be reversed soon after other options to absorb excess liquidity become exercisable. The normal CRR in the meanwhile remains unchanged at 4.00% of outstanding NDTL.

This has turned the tables for banks. Until recently, banks benefited immensely. Post demonetisation, people rushed to deposit scrapped notes, which helped banks grow their Current Account and Savings Account (CASA) deposits rapidly. But now, with the incremental CRR becoming applicable, the banks have lost their

low-cost source of funds.

The impact of RBI’s move:

- Banks can no longer generate any windfall. We are back to square one—from comfortable liquidity to a liquidity crunch. Nonetheless, RBI has provided some relief by conducting variable repo operations worth Rs 3.30 lakh crore. This will help banks borrow from RBI to tide over cash requirements.

- Sovereign bond yields have started inching up, denoting that liquidity-driven rally in G-secs might lose steam. Banks are no longer having a huge cash at their disposal to manage the treasuries astutely.

- Short-term bond yields might also witness hardening of yields going forward.

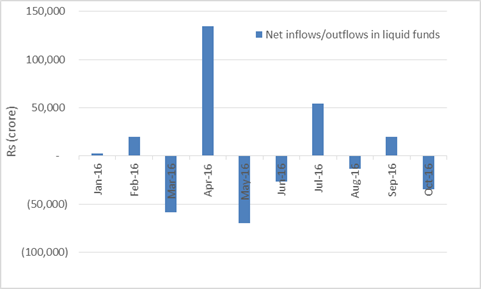

- Liquid funds are witnessing a redemption pressure which is likely to continue even in the future, as banks will be forced to liquidate their investments to fulfil cash requirements.

Will liquid funds fall out of favour?

(Source: AMFI, PersonalFN Research)

The Government has been mulling over issuing market stabilisation bonds to suck out excess liquidity from banks. As soon as these are issued to the market, the RBI may roll back the diktat of maintaining ‘incremental CRR’. Banks would then invest in those bonds and earn interest.

Further, the Government and RBI may collectively take some additional measures to iron out abnormalities in the banking system.

How should investors read this situation?

Debt funds have done extremely well in the recent past. The expectations of the RBI cutting policy rates at the fifth bi-monthly monetary policy review scheduled on December 7, 2016 has made many investors go bullish on bond funds.

But you need to recognise that most of the rally has already been captured at the longer end of the yield curve and additional steam seems to have reduced. Therefore, it would be imprudent to go overboard and take exposure at the longer end of the yield curve. Nevertheless, if you hold a high-risk appetite and have a long time horizon (of at least 3 years), not more than 20% of your entire debt portfolio may be allocated to long-term debt funds via dynamic bond funds (as they are enabled by their investment mandate to take positions across maturity profile of debt papers). But don’t merely speculate on interest rate movement; it’s pointless, dangerous, and unhealthy in uncertain times.

Instead, while you invest in debt market instruments, particularly debt mutual funds, gauge your risk profile and investment horizon, and then make smart moves. If you’re averse to risk and have a short-term investment horizon of 3 to 6 months, consider investing in ultra-short term funds (also known as liquid plus funds). And if you have an extreme short-term time horizon (of less than 3 months) you would be better-off investing in

liquid funds. Don’t forget that investing in debt funds is not risk-free.

If you are still willing to speculate, be ready for not-so-pleasant surprises.

Add Comments