It is very common to see losses in equity markets which lead to people losing their money in stocks and equity oriented mutual funds, many have even made losses in their investment in gold. Even income funds and gilt funds are subject to high volatility as they carry interest rate risk. But recently you may have read about or may have even come across someone making losses in an instrument where they parked their money thinking it to be really safe. Yes in the last fortnight people have seen negative returns in their safe investments i.e. money market mutual funds or commonly known as liquid funds. Now before we find out what may have gone wrong with these funds, let's get down to some basics first...

What are Money Market Mutual Funds?

Money Market Mutual Funds, also known as liquid and liquid plus funds, invest in debt instruments with very short residual maturity profile of say less than 180 days. They usually invest in Certificate of Deposits (CDs) issued by banks, Commercial Papers (CPs), Pass through Certificates, Bill of Discounting and sometimes even in term deposits of banks.

What are they meant for?

Liquid and liquid plus funds are ideal for parking short term surplus. Since they have a lower maturity profile; they are less sensitive to default risk and interest rate risk. In theory, longer the tenure of the paper, higher is the impact of change in the interest rate. These funds attract investors who want to park their money for a very short time period and seek safety of capital. They are known to provide immediate liquidity when the investor needs his money. While historically money market mutual funds have been known as a safe investment option, the sentiment might have changed in the past few weeks.

What went wrong this time?

The Indian rupee (INR) has been in news over the past few months; due to huge depreciation it has seen in its value, where it has crossed Rs 60 against per USD. Following the cracking of rupee, RBI intervened in the forex market to a great extent. In order to curb speculation in the currency market, RBI recently took measures to suck out excess liquidity in the system which was otherwise believed to be giving rise to speculative trades in the currency markets and driving the rupee further down. Although higher than acceptable, Current Account Deficit (CAD) has been perceived as the primary reason for depreciation in INR, speculation is also considered the other prominent reason for prevailing weakness in the INR.

As first round measures, RBI surprised the markets by raising the Bank Rate as well as the rate on Marginal Standing Facility (MSF) by 200bps (2%) on July 15, 2013 (from 8.25% to 10.25%). Bankers often use this window to borrow money from RBI to meet short term liquidity requirements and to bridge short term mismatches in their assets and liabilities. By hiking short term rates, RBI made short term borrowing costlier for banks. It also restricted borrowing by banks under Liquidity Adjustment Facility (LAF) to Rs 75,000 which was set as the limit for the whole banking system.

Despite such strict measures, rupee advanced only mildly (in the range of 1.5%-2%) over a week's time from the day of announcement. Not seeing desired results, the determined RBI tightened screws again. It restricted banks to borrow only upto 0.5% of their Net Demand and Time Liabilities (NDTL). Moreover, banks were asked to at least maintain Cash Reserve Ratio (CRR) of 99% (of 4% i.e. about 3.96%) on daily basis as against the minimum requirement of 70% (2.8%) which is currently in place. It is noteworthy that CRR requirement of average 4% on a fortnightly basis remains unchanged. The only difference has been that now there's no room for fluctuation within a reporting fortnight. The later change was made effective from July 27, 2013.

The impact on Liquid and Liquid Plus Mutual Funds

Rising short term rates and tighter liquidity position made money market mutual funds lose on marked to market valuation. When interest rates go up bond prices fall. Furthermore, when liquidity is tight, new papers quote higher rates and also push yields on existing papers upwards. It is mandatory on ultra-short term mutual funds to make accounting of returns on marked-to-market basis in case of all papers having residual maturity of 60 days and above. As the increase in interest rates leads to fall in value of the existing bond instruments, it leads to the loss of valuation in bond funds on a mark-to-market basis. As a result of the sharp increase in overnight rates and liquidity tightening, the NAV of even liquid and liquid funds dropped on marked to market basis.

What was the quantum of loss?

Let's understand this by the sensitivity of mutual fund to interest rate changes. Sensitivity of a mutual fund to change in the interest rate is measured by its modified duration. Modified duration calculates the rate at which the fund may move up or down with every 1% change in the interest rate. For example, a fund with a modified duration of say 84 days or 0.23 years would move +/- 0.23% for every 1% change in the interest rate. Hence the 2% rise in interest rate results in 0.46% expected drop in NAV on marked to market basis.

Similarly in case of liquid fund having Modified duration of say 40 days, would have calculated 0.219% expected drop in NAV; but this drop in NAV has to be adjusted against the daily accrued yield on the portfolio before arriving at the closing NAV and hence slightly lower impact on the days loss in the fund's NAV. Such a loss in liquid fund will take around 9 days to recover, if the fund has the net Yield to Maturity of say 9% p.a., as the daily accrued yield on the fund's portfolio will be then around 0.024%.

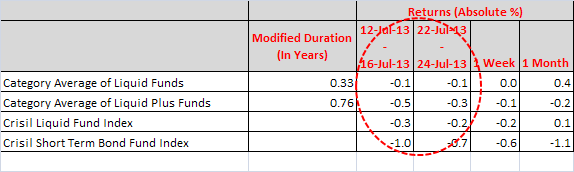

Performance of Liquid and Liquid Plus Funds

Modified Duration is as per portfolios disclosed on June 30, 2013

(Performance data as on July 26, 2013)

(Source: ACE MF, PersonalFN Research)

As per the portfolios disclosed on June 30, 2013, average of the modified duration of liquid funds was 0.33 years and that of liquid plus funds was 0.76 years. This indicates that sensitivity to interest rates was low in case of liquid funds as compared to that of liquid plus funds. Also, negative returns generated by liquid funds are lower than the negative returns generated by liquid plus funds. Returns calculated for the period between July 12, 2013 and July 16, 2013 measure the impact of first round of RBI moves while those between July 22, 2013 and July 24, 2013 measure the impact of the second move. Interestingly, liquid funds have outperformed Crisil Liquid Fund Index across reading periods. On the other hand liquid plus funds have failed to do so.

It is clear from the table above, that despite seeing a drop in their NAVs, liquid funds have been quick enough to recover from losses, as returns generated by them (as on July 26, 2013) over 1-week and 1-Months' time were positive. This suggests that marked to market losses are notional if you stay invested for longer duration. On the other hand, liquid plus funds may take a little longer to erase losses due to their higher modified duration.

However not to forget the quantum of loss was severe in the funds having investments in longer maturity instruments, like income funds and gilt funds usually hold portfolio with maturity of around 5 to 10 years, and they were the ones to see a loss of around 3% to 4% in a day.

PersonalFN's View

PersonalFN is of the view that loses made by investors in liquid and liquid plus funds have been a result of extra ordinary intervention of RBI to absorb excess liquidity. However, such situations are one-off events and may be reverted as soon as the specified objective is fulfilled. PersonalFN believes that investors shouldn't lose faith in liquid and liquid plus funds only because they have seen negative returns over a short time period.

Instead, while selecting a fund for your portfolio you should concentrate on risk-reward matrix which makes you aware about the risk profile of the fund and its reward potential. PersonalFN is of the view that money market mutual funds are still a better investment option to park your short term surpluses. However you should have clear time horizon in mind even before investing in a liquid or liquid plus funds.

Add Comments