Shriram Transport Finance Company Limited (STFCL) is the flagship company of the Shriram group which has significant presence in Consumer Finance, Life Insurance, General Insurance, Stock Broking and Distribution businesses. Established in 1979, Shriram Transport, at present is the largest asset financing NBFC (Non-Banking Finance Company) in the country and holistic finance provider for the commercial vehicle (CV) industry and seeks to partner small truck owners for every possible need related to their assets.

The business model

STFCL is a major player in the domestic CV finance segment, with assets under management worth Rs 36,182 crore as on March 31, 2011. It is the leader in the pre-owned CV finance segment, with a market share of around 25%. The company has also improved its market position in the new CV finance segment, with a market share of around 8%. The company lends predominantly to the single-road transport operator (SRTO) segment, which accounts for more than 95% of its outstanding portfolio. STFCL has its focus in catering to the needs of the Small Truck Owner (STO) and financing pre-owned trucks. It has PAN India presence with 488 branch offices. The company manages assets over Rs 36,000 crores and has a live customer base exceeding 7,50,000.

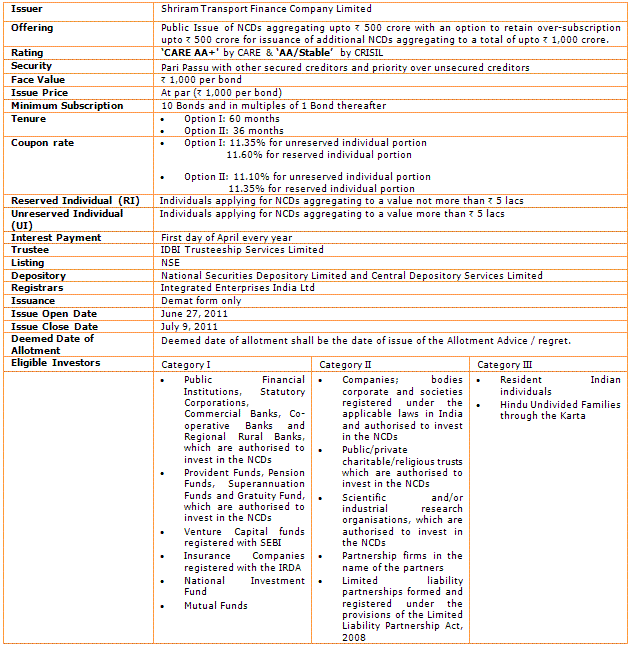

Thus, in order to augment the lending and investment needs of the company, STFC is currently offering secured Non Convertible Redeemable Debentures (NCD) of face value of Rs 1,000 each at par aggregating to Rs 500 crore along with an green shoe option to retain oversubscription upto Rs 500 crore.

The details of the offering (NCD) are as follows:

Note: PAN card is mandatory for subscribing to these bonds. A self attested copy shall be enclosed along with the application form.

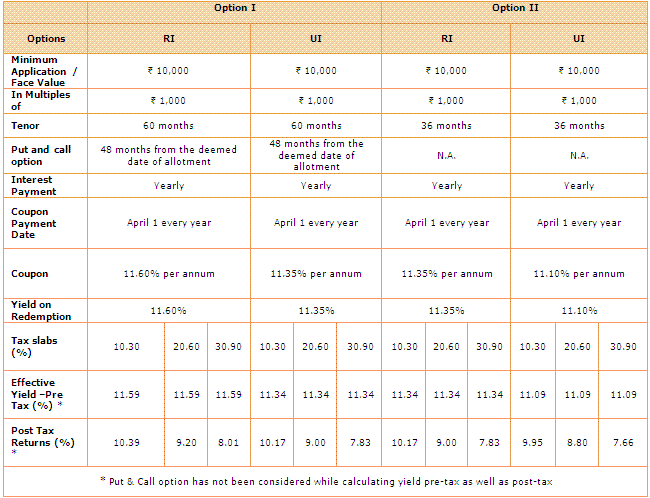

Investors’ will also have the following options available at the time of subscribing to the issue:

(Source: Shriram Transport Finance Co. Ltd. & PersonalFN Research)

Well, after reading the details of the NCD (as provided above), there may be still some more questions popping up, which are answered hereunder:

- Will I get any tax benefit if I invest in these bonds?

No, these bonds do not entitle you to any tax benefit nor are these any "infrastructure bonds", which make you eligible for an additional tax deduction under section 80 CCF.

- What is the Tax Treatment of interest on these Bonds? Are these Bonds Tax Free?

No, the interests on these bonds are not tax free – they are chargeable to tax. The interest income will be taxed under "income from other sources", and will be brought to tax at the respective income tax rates you fall under.

The Tax Deduction at Source (TDS) will not take place as these bonds are issued a demat form and are listed on the exchange.

- Can a minor apply to these bonds?

Yes, a minor can apply for these bonds, but only through a guardian.

- Can one apply in joint names?

Yes, one may apply in a joint name. However, the demat accounts will also be required to be held in joint name and the order of applicant shall be the same as appearing in the demat account. Moreover, all payments will be made out in favour of the first applicant as well as all communications will be addressed to the first named applicant whose name appears in the application form and at the address mentioned therein.

- Who will get the interest in case of joint application?

In case of joint application, interest will be accounted to the first holder only.

- My demat account is in joint name, but I want to apply is a single name?

In case of a single application, demat account of the same single applicant would be necessary. Joint demat account would not do.

- If I’m an NRI can I invest in these bonds?

No, NRIs are not eligible to invest in these bonds.

- Is there a lock-in period while investing?

No. There is no lock-in period for these bonds.

- In whose favour the cheque is to be made?

Cheques have to be made in the favour of "Escrow Account STFC NCD Public Issue" and crossed "A/C PAYEE ONLY".

OUR VIEW:

In our opinion the yields on investment offered by STFCL are quite appealing. Also, the credit rating allotted to the issue is stable (AA+ by CARE and AA/Stable by CRISIL) along with the ticket size (minimum investment amount) being kept low at Rs 10,000 (in order to encourage greater retail participation).

Moreover, the company has a Debt to Equity ratio of 4.16 (post NCD issue the D/E ratio will be 4.36) and an interest coverage ratio of 1.81 indicating that the company is comfortably leveraged and is well placed to service its debt for the kind of business model it follows.

However, while investing one may invest a small portion of the investible surplus in STFC, and not go too aggressive since going forward with the rising interest rate scenario (to tame inflation), one may see attractive coupon payments being offered with new offerings of NCDs. But one needs to check on the safety rating offered by such issues and the business model of the company before investing.

Add Comments

| Comments |

lutfiye@dorukfilm.com.tr

Jul 07, 2011

Hey, subtle must be your middle name. Great post! |

phnh@bigpond.com

Jul 09, 2011

You're the greatest! JMHO |

1