Out of the many facilities available for mutual fund investors, Systematic Transfer Plan and Systematic Withdrawal Plan are at times used interchangeably. However, there are some striking differences between the two.

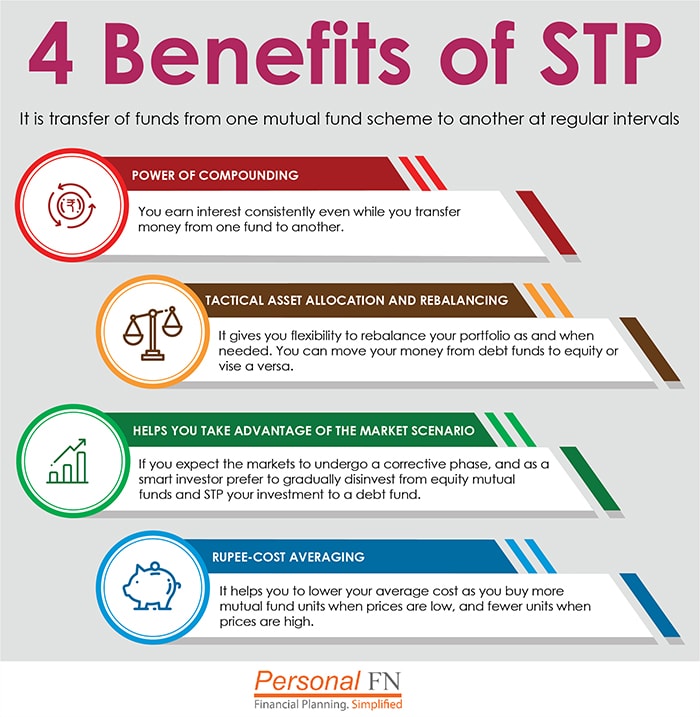

Systematic Transfer Plans: Under STP, the lump sum amount you invested in a fund earlier can be transferred in a piecemeal manner at regular intervals systematically into another mutual fund scheme (as per your preference) of the same mutual fund house.

Systematic Withdrawal Plan: Under SWP, you have the facility to withdraw a fixed sum of money from a mutual fund scheme regularly (say monthly, quarterly, half-yearly, and annually) and garner the potential to clock returns on the remaining investments over a period of time.

When to opt for STP and SWP?

Both the facilities help you reap the benefits of compounding and rupee cost averaging but, their functions are different.

Let’s take STP first…

Say you earned a promotion and received a hefty bonus of Rs 5 lakh, and you decide to invest this sum into equity mutual funds. But as the markets are currently at an all time high, you realise it wouldn’t be wise to invest all your winnings in one go. The entire sum can be initially invested in an ultra-short term debt fund and/or a liquid fund taking cognisance of the fact that markets are at a high. Then, systematically a certain sum of money lying in the liquid fund and/or ultra-short-term fund can be transferred –monthly or quarterly – to an equity-oriented fund of your choice (but which ideally can prove worthy for long-term wealth creation) over a period of time.

Coming to SWP…

The same Rs 5 lakh bonus earned can be used smartly under SWP as well. Instead of saving it in your savings account and withdrawing Rs 10,000 every month, you can withdraw smartly under SWP and reap the benefits of compounding.

For example, you invest Rs 5,00,000 in Fund A. If the net asset value (NAV) of the fund is Rs 100, then you will hold a total of 5,000 units.

| Month |

Cashflows |

NAV |

Fund Units |

Value |

| Jan |

5,00,000 |

100 |

5,000 |

5,00,000 |

| Feb |

-10,000 |

103 |

4,903 |

5,05,000 |

| Mar |

-10,000 |

102 |

4,805 |

4,90,097 |

| Apr |

-10,000 |

105 |

4,710 |

4,94,511 |

| May |

-10,000 |

108 |

4,617 |

4,98,641 |

| June |

-10,000 |

106 |

4,523 |

4,79,407 |

Note: The above table is for illustration purpose only

(Source: PersonalFN Research)

If you withdraw Rs 10,000 under SWP, your holdings will decline to 4900 units (i.e. Rs10000 / Rs100 NAV = 100 units are reduced from his initial holdings) in the first month.

In next month, NAV of the fund has appreciated to Rs 101 due to market dynamics. The number of units equivalent to Rs 10,000 i.e. only 99 units will be sold (i.e. Rs 10000/ Rs 101 NAV = 99 units).

In five months, when you withdraw a total of Rs 50,000, your effective portfolio would value at Rs 4,50,000. However, the total value is now Rs 4,79,407; effectively proving to be a better earning instrument due to the market dynamics vis-à-vis parking money in a savings account, and/or other traditional instruments such as fixed deposits.

But beware of the tax implications:

STP: A Securities Transaction Tax (STT) will be levied at the time of exit i.e. from one equity scheme to a debt scheme, or even another equity mutual fund scheme (of the same fund house). However, for transfer from debt mutual fund schemes to equity oriented mutual fund scheme, STT is not levied.

SWP: Any gain on sale of equity mutual fund units held for less than 1 year attracts a Short-term Capital Gains Tax(STCGT) of 15%. However, your withdrawals with SWP will be in a smaller amount and in the first year, it will be your principal amount. Hence, it may not attract STCGT in case you withdraw via SWP.

In case of debt funds, short-term is defined as 3 years and any profit made within this duration is classified as a Short Term Capital Gain (STCG) and will be taxed as per your income-tax bracket (i.e. marginal rate of taxation). And Long Term Capital Gain (LTCG) i.e. investments held for a period of more than 3 years, at 20% tax rate with indexation.

To Sum-up

Both STP and SWP are smart ways of gaining the best of your money. You can benefit from different facilities. It depends on your goal, whether you aim to re-allocate your assets or want to let your money grow even while you spend.

The STP facility is best suited for investors who wish to completely stay invested, while they transfer funds from one mutual fund scheme to another, from a portfolio review standpoint or for the purpose of systematic asset allocation in the objective of wealth creation. Debt funds are ideal for capital protection and equity funds are suitable for investors looking for capital growth. Hence, a blend of different types of funds always helps to strike the balance between both asset classes.

SWPs can be used as a means to source your monthly expenses or retirement planning. It won’t only provide you with a fixed source of income, but also a disciplined approach to spending. Rupee-cost averaging works in your favour when you withdraw systematically.

Add Comments

| Comments |

alakhinvestments@gmail.com

Aug 06, 2018

Dear Sir,

As an IFA for my client who is interested to invest Rs. 15 lakhs in any scheme of Mutual Fund for short period of 3-4 years... It is my client wish..

I would request you to recommend the correct and ideal way for this ...

Regards.

Akhilesh |

alakhinvestments@gmail.com

Aug 06, 2018

Dear Sir,

As an IFA for my client who is interested to invest Rs. 15 lakhs in any scheme of Mutual Fund for short period of 3-4 years... It is my client wish..

I would request you to recommend the correct and ideal way for this ...

Regards.

Akhilesh |

1