Impact

In an exciting cricket match, spectators start cheering for a six, and at the very next ball if the batsman smashes it out and does the honours, there a big round of applause. However, such euphoria doesn't last for very long if batsman throws away his wicket in the same over.

Something similar seems to be happening to Indian capital markets these days.

As widely anticipated, the Reserve Bank of India (RBI) cut policy rates at its 2nd bi-monthly monetary policy review meet. It was an extremely pleasing moment, as RBI honoured the expectations in the 2nd bi-monthly monetary policy statement for 2015-16; but a hawkish tone to its outlook spoiled the rate cut party.

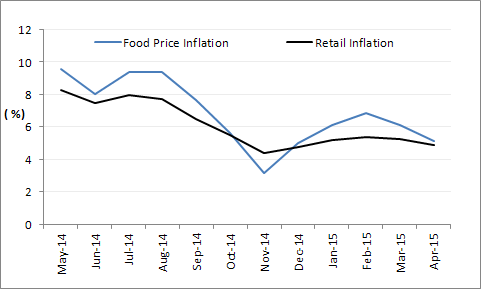

Upside risk to food inflation remains...

(Source: MOSPI, PersonalFN Research)

What stance did the RBI take?

- The central bank reduced the Repo rate by 25 basis points (bps) or 0.25% with immediate effect taking the repo rate down to 7.25% from 7.50% prior to policy action.

- Consequent to the above, the reverse repo was also re-adjusted to 6.25% from 6.50% earlier, thereby continuing to maintain the Liquidity Adjustment Facility (LAF) corridor between repo and reverse repo rate at 100 bps

- Also the Marginal Standing Facility (MSF) rate (which is determined with a spread of 100 basis points above the repo rate) was consequently re-adjusted 8.25%, and so was the bank rate to 8.25% with immediate effect

- The Cash Reserve Ratio (CRR) was kept unchanged at 4.00% of Net Demand and Time Liability (NDTL)

- The Statutory Liquidity Ratio (SLR) was kept unchanged at 21.50%

- Continue to provide liquidity under overnight repos at 0.25% of bank-wise NDTL at the LAF repo rate and liquidity under 14-day term repos as well as longer term repos of up to 0.75% of NDTL of the banking system through auctions

- Continued with overnight/term variable rate repos and reverse repos to ensure smooth liquidity

The background to policy action...

Over last the last couple of months since RBI issued its 1st bi-monthly monetary policy statement for 2015-16, global economy continued to recover slowly and albeit some wobbliness. Risk aversion emerged taking cognisance of what monetary policy stance the central banks of the world, especially developed economies may take. Bond markets, forex markets and equity markets remained volatile, and so did global crude oil prices.

Speaking about India, economic activity moderated in the first quarter of fiscal year 2015-16. Hailstorm and unseasonal rainfall went on to impact roughly 94 lakh hectors of sowing area. As per the estimates of Ministry of Agriculture, the food grain production is likely to be 5% lower when compared to that of previous year. Production of pulses and oilseeds is likely to be even worse this season. And even now, as we head to the onset of monsoon, the Indian Meteorological Department (IMD) has forecasted below-average monsoon. In April, the IMD, in its first long-range forecast, had said that the country will receive 93% long-period average) rainfall during June to September period. And now, in a very recent forecast, the IMD has downgraded its southwest monsoon forecast from below normal to deficient (as El Nino conditions are well-established over the equatorial Pacific Ocean and likely to strengthen further). Such a scenario has posed an upside risk to food inflation, especially as the outlook appears clouded for kharif crops.

Fuel inflation rose to 12-month high in April on account of rising electricity and firewood prices. Crude oil prices firmed up a bit on geopolitical risks and there was considerably volatility

On the manufacturing side, industrial production seemed to be recovering, yet it lacked consistency. Weakness in consumption, underutilisation of capacity in many industries; point at an underlying weakness in the economic progress.

Corporate results have been poor for the last couple of quarters of the fiscal year gone by, and it could have been even worse hadn't input cost gone down. For banks hit by bad loans, more capital infusion may be needed to clean up their balance sheets and support lending as investment revives.

On the positive side, coal production revived which may augur well for power generation companies. Clarity on gas pricing and prospects of gas availability bode well too for industry. Higher service tax collection and pick-up in logistic activities could augur transportation, communication and trade.

As far as the Liquidity condition is concerned, it eased in April after tightness in second-half of March on account of advance tax outflow and financial year-end behaviour of banks. Hence the central bank's liquidity management operations were reversed in view of the improvement in liquidity conditions through April. During May, however, rapid increase in currency in circulation and a build-up of government balances resulted in liquidity conditions tightening again. But fine tuning operations at regular intervals were conducted, besides the regular overnight repo at fixed rate and 14-day variable rate repo auctions. The average daily net liquidity injected through LAF fixed rate repos, besides regular 14-day variable rate repos, additional variable rate repos and MSF, was 1031 billion in May as compared with 819 billion in the month before.

Hence on the aforesaid background, RBI accorded a 25bps rate cut, mainly because:

- Banks have started passing on benefits of previous rate cuts;

- Headline inflation has so far been in line with expectations;

- The impact of unseasonal rains on food inflation has been limited so far;

- Administered price increases remained muted;

- The timing of the normalisation of the monetary policy in the U.S. seems to have been pushed back;

- Domestic capacity utilisation stayed lower;

- Still mixed indicators of recovery; and

- Subdued investment and credit growth

But the guidance to future monetary policy action had a hawkish tone...

The central bank cited the risk to inflation identified in April, three still cloud the picture.

First, some forecasters, notably the IMD, predict a below-normal southwest monsoon. Astute food management is needed to mitigate possible inflationary effects.

Second, crude prices have been firming amidst considerable volatility, and geo-political risks are ever present.

Third, volatility in the external environment could impact inflation.

Therefore, a conservative strategy would be to wait, especially for more certainty on both the monsoon outturn as well as the effects of Government responses if it turns out to be weak.

With still weak investment and the need to reduce supply constraints over the medium term to stay on the proposed disinflationary path (to 4.0% in early 2018), however, a more appropriate stance is to front-load a rate cut today and then wait for data that clarify uncertainty, the central bank said. RBI also mentioned meanwhile banks should pass through the sequence of rate cuts into lending rates.

Projection on CPI inflation...

Assuming reasonable food management, the central banks expects inflation to be pulled down by base effects till August 2015, but is of the view that may begin to rise thereafter to about 6.0% by January 2016 – slightly higher than the projections (of 5.8%) in April 2015. Putting more weight on the IMD's monsoon projections than the more optimistic projections of private forecasters as well as accounting for the possible inflationary effects of the increases in the service tax rate to 14%, the risks to the central trajectory are tilted to the upside.

Projections on GDP growth...

Reflecting the balance of risk and downward revision to Gross Value Added (GVA) estimates of 2014-15, the GDP growth for fiscal year 2015-16 has been marked down to 7.6% from 7.8% projected earlier due to the uncertainties surrounding.

So, how have the markets reacted?

A 25 bps rate cut expectation was built-up in equity and bond prices. But the hawkish forward guidance seemed to have spoiled the party. Hints of pausing rate cuts for now seemed to have upset the market. The new (7.72% 2025) 10-year G-Sec yield inched up to 7.72% from 7.64%, the previous day's close citing to risk to inflation. The Indian equity market too has taken a plunge taking cognisance of the risk to inflation and global headwinds in play.

What to expect?

If the southwest monsoon indeed turns out to be deficient as per the latest forecast of IMD, this would be the last rate cut of calendar 2015. This is because deficient or even a sub-normal monsoon would mean lower agriculture growth combined with relatively higher inflation and may also take a jibe at consumption and economic growth.

RBI would now assess the performance of the Government in containing inflation under adverse conditions. PersonalFN believes, now that the central bank has cut rates thrice in the first half 2015, there is a huge pressure to perform on the Government, banks and the industry.

What should the investment strategy now while investing in debt market?

PersonalFN believes the longer end of the maturity curve is exposed to risk. Most of the rally has already occurred in the last one year and now the longer end of the maturity curve seems to be running out of fizz. Even if you want to take the risk and bet on the longer end of maturity curve, consider only dynamic bond funds to do so (as they are enabled by their investment mandate to take positions across maturity profile of debt papers) and provided you have an investment horizon of at least 3 years.

In case you have a time horizon of less than a year, you should stay away from funds with longer maturities. If you have a short-term investment horizon of 3 to 6 months you could consider investing in ultra-short term funds (also known as liquid plus funds). And if you have an extreme short-term time horizon (of less than 3 months) you would be better-off investing in liquid funds.

Add Comments