After a surprising rate cut of 25 basis points (bps) in mid-January 2015, the Reserve Bank of India kept policy rates unchanged in its 6th bi-monthly monetary policy statement, 2014-15. This was a surprise to those who expected the central bank to do another round of rate cut now that inflation had mellowed and looked benign.

So, what led RBI to cut to keep rates unchanged?

Well, Dr Raghuram Rajan flagged certain worries on the global and domestic economic front which held him back from reducing policy rates further.

Macroeconomic assessment

- Global economic concerns:

In the macroeconomic assessment the central bank cited that since the 5th bi-monthly monetary policy statement (held on December 3, 2014) the International Monetary Fund (IMF) has revised its forecasts for growth in 2015 and 2016 downwards, although they are higher than the estimates for 2014. In the U.S., growth moderated towards the end of 2014 with the boost to consumption demand from the fall in crude prices more than offset by the drag on net exports from a strong US dollar. Speaking about the Eurozone, economic conditions have deteriorated in an environment of deflation, political tensions in Greece and still-elevated levels of unemployment. While the European Central Bank (ECB) has announced quantitative easing in an attempt to reinvigorate economic growth in the Eurozone, it highlights the pain in the Euro zone.

Along with the growing belief that the U.S. Federal Reserve would hold on to rate for longer than previously thought, bond yields have fallen to their historic lows in Advanced Economies (AEs). Nevertheless the financial markets remain vulnerable to uncertainty surrounding monetary policy normalization in AEs.

As far as Japan is concerned, the demand has only begun to recover from the impact of consumption tax increase. The Yen’s depreciation nonetheless is supporting exports. China’s economy too is slowing down because of weakening in property market; which in turn has prompted targeted measures to ease financial constraints faced by corporations and banks. In other emerging market economies (EMEs), growth has weakened sharply for oil exporters, whereas inflationary pressures, subdued investment appetite and a neutral fiscal stance continue to dampen growth in non-oil exporters.

- Agricultural concerns:

Domestic activity seems to have remained subdued in Q3 of 2014-15, mainly reflecting the shortfall in the kharif harvest relative to a year ago. Agricultural growth is likely to pick up in Q4 with the late improvement in the north-east monsoon and in rabi sowing. Nevertheless, growth expectations should be tempered as lead indicators such as tractor and motorcycle sales and slowing rural wage growth all point to subdued rural demand.

- See-sawing industrial activity:

While the Index of Industrial Production (IIP) for November 2014 has reported a sharp uptick there are doubts about it sustainability. A see-saw movement is yet evident in IIP. Continuing contraction in consumer goods production underscores the persisting weakness in consumption demand (even while raising questions about measurement of production).

However the advance indicators of industrial activity which are indirect tax collections, non-oil non-gold import growth, expansion in order books, and new business reported in purchasing managers surveys; in view of the RBI point to a modest improvement in the months ahead. Moreover, according to the central bank the policy initiates in land acquisition as well as efforts underway to unlock mining activity and to widen the space for foreign direct investment in defence, insurance and railways, should create a more conducive setting for industrial revival.

- Slower activity in the service sector:

The services Purchasing Manager Index indicate slower activity, especially in new orders. However, other indicators of the services sector including foreign tourist arrivals, automobile sales, cargo handled at ports, and railway freight traffic suggest improvement. Therefore there are mixed signals. The overall growth prospects will be contingent upon a turnaround in investment and a durable improvement in the business climate to complement the upsurge in business optimism.

- Inflation:

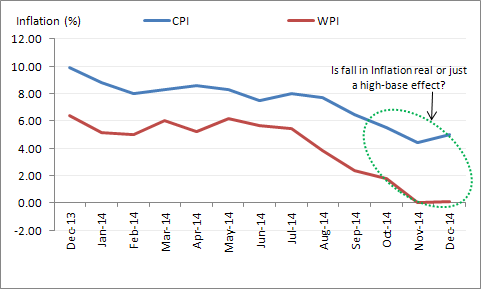

The retail inflation measured by the year-on-year changes in the Consumer Price Index (CPI) bounced a little in December 2014 on the expected reversal of favourable base effects that had tempered upside pressures since June 2014.

Inflation bounced up a little…

Data as on December 2014

(Source: Office of the Economic Advisor, Personal FN Research)

A slight softening of cereal prices and a sharp seasonal fall in vegetables prices moderated the trajectory of headline inflation, but persistent firmness was seen in prices of protein-rich items such as milk, meat and pulses. In view of the central bank, seasonal increase in vegetable prices which typically set in around March, have to be monitored carefully.

The RBI cited that while the inflation declined faster than expected due to favourable base effects during June-November 2014, the upturn in December 2014 turned out to be muted relative to projections.

Liquidity Situation

Active liquidity management operations under the revised framework adopted in early September 2014 ensured that liquidity conditions have generally remained comfortable. Money market rates evolved in close alignment with the repo rate barring some occasional aberrations around days of advance tax outflows and quarter-end tightness. The average daily net borrowings under the LAF (including term repos, reverse repos and Marginal Standing Facility (MSF)) was around Rs 850 billion in December 2014 and January 2015.

Monetary Policy Action…

Hence in the backdrop of the aforementioned macroeconomic assessment, it was decided by RBI as under:

- To keep the policy repo rate unchanged at 7.75%;

- To keep the reverse repo rate unchanged at 6.75%;

- The keep the Marginal Standing Facility (MSF) and Bank rate unchanged at 8.75%;

- To keep the CRR of scheduled banks unchanged at 4.00% of Net Demand and Time Liability (NDTL);

- Reduce the Statutory Liquidity Ratio (SLR) of scheduled commercial banks by 50 bps to 21.50% from 22.00% of their NDTL with effect from fortnight beginning February 7, 2015;

- Continue to provide liquidity the overnight repos at 0.25% bank wise NDTL at the Liquidity Adjustment Facility (LAF) repo rate and liquidity under 7-day and 14-day term repos of upto 0.75% of NDTL of the banking system through actions; and

- Continue with daily variable rate repos and reverse repos to smooth liquidity

What does the policy stance mean and its impact?

The repo rate is the rate of interest charged by the central bank on borrowings by the commercial banks. Keeping it unchanged would infer borrowing cost of commercial banks would remain at the same level. Hence as a reaction to such a move cost of borrowing for individuals and corporates may not ease keeping home loans and car loans yet expensive. The Reserve Bank too has observed that despite generalised fall in cost of funds, banks have yet to pass through these effects as also the effects of the policy rate cut on January 15, into the spectrum of lending rates.

The reverse repo rate is the rate of interest, at which the banks park their surplus money with the central bank. Keeping the repo rate unchanged will imply that commercial banks would enjoy the same rate of interest as earlier, for parking their surplus funds with RBI.

The CRR is the amount of liquid cash which the banks are supposed to maintain with RBI. Keeping it unchanged would not infuse further primary liquidity into the banking system. Likewise keeping the MSF rate would not infuse short-term liquidity in the system. But, through the 7-day and 14-day term repos, very short-term liquidity concerns will be addressed to. Likewise, the decision to continue with daily variable rate repos and reverse repos will smooth the liquidity.

The Statutory Liquid Ratio (SLR) is the amount that the commercial banks require to maintain in the form of cash, or gold or Govt. approved securities before providing credit to the customers. Lowering the rate here to 21.50% from 22.00% could improve credit flow in the system – especially to productive sectors, and thereby support growth. In fact, it is said that such a move may infuse upto Rs 45,000 crore into the banking system.

Policy Rationale

The RBI preferred to remain cautious rather than over optimistic in the backdrop of the macroeconomic assessment and with the budget coming up which may bring significant change in the fiscal space.

The upside risk to inflation stem from the unlikely possibility of significant fiscal slippage, uncertainty on the spatial and temporal distribution of the monsoon during 2015. Also the low probability but highly influential risks of reversal of international crude prices due to geo-political events, is another factor in play. Heightened volatility in global financial markets, including through the exchange rate channel, also constitute a significant risk to the inflation assessment. But by and large inflation dynamics have so far been consistent with the assessment of the balance of risks by the Reserve Bank bi-monthly monetary policy statements, although with some undershooting relative to the projected path of disinflation. Thus RBI has stayed put on its projection of 6.00% retail inflation by January 2016.

Guidance from monetary policy and path for interest rates

The RBI has indicated that the key to further easing are data that confirm continuing disinflationary pressures. Also critical would be sustained high quality fiscal consolidation. Given that there have been no substantial new developments on the disinflationary process or on the fiscal outlook since January 15, 2015, the central bank has cited in it 6th bi-monthly monetary policy statement, 2014-15 that it is appropriate to await them and maintain the current interest rate stance.

As far as liquidity is concerned, the central bank has said that it would continue to meet system wide liquidity needs as per the revised liquidity adjustment framework announced on August 22, 2014.

RBI’s projection of GDP:

The outlook for growth has improved modestly on the back of disinflation, real income gains from decline in oil prices, easier financing conditions and some progress on stalled projects. These conditions according to RBI should augur well for a reinvigoration of private consumption demand, but the overall impact on growth could be partly offset by the weaker global growth outlook and short-run fiscal drag due to likely compression in plan expenditure in order to meet consolidation targets set for the year. Therefore the baseline projection for growth using old GDP base (i.e. 2004-05) has been retained at 5.5% for 2014-15. For the next financial year the projections as per the central bank are inherently contingent upon the outlook for the south-west monsoon and the balance of risks around the global outlook. Domestically, in view of RBI, conditions for growth are slowly improving with easing input cost pressures, supportive monetary conditions and recent measures relating to project approvals, land acquisition, mining, and infrastructure. Accordingly, the central estimate for real GDP growth in 2015-16 is expected to rise to 6.5% with risks broadly balanced at this point. Nevertheless, the revised GDP statistic released on January 30, 2015 along with the estimates for 2014-15 expected on February 9, 2015 will need to be carefully analysed and could result in revisions to the Reserve Bank’s growth projections for 2015-16.

Impact on debt markets...

Some participants in the Indian debt market had expected RBI to do another round of rate cut. But as the policy rates were kept unchanged, the yields bounced. The yield on the 10-year benchmark bond rose by 8 basis points compared with its previous close to end at 7.73%. Nonetheless the yield was place below the repo rate of 7.75%.

What strategy should debt investors should adopt?

PersonalFN is of the view that, bond markets may remain optimistic about rate cuts going forward. There might be a sharp built up in bond prices. Bond investors would track a few events such as inflation, rupee strength, progress of Government in containing fiscal deficit, budget and developments on reform fronts to name a few. If broadly these factors stay positive going forward, softening in yields can’t be ruled out.

Having said this, PersonalFN believes, in case any of the macro-economic indicators affecting the decision of RBI turns unfavourable, bond rally might retreat. For any reason, RBI doesn’t cut policy rates early year, bond yields may witness upward pressure.

Having said the above, at present we believe that there are reasons for one to take exposure to longer end of the maturity curve. But while you do so, ensure that your exposure to long term debt funds does not exceed 20%-25% of the entire debt portfolio. While G-sec funds may start delivering returns as fundamentals improve and policy rates start to relax, going overboard now may not be very prudent.

If you are risk averse you can also invest in Fixed Deposits (FDs) now at high interest rates, before banks start pulling down interest rates further. Recently some banks some of India's prominent banks such as SBI, Axis Bank and HDFC Bank reduced interest rates on deposits in the range of 0.25% to 0.75% for various maturities. So, at present FD rates for tenure of 1 year is in the range of 7.75% - 8.75% (depending on the bank you opt for), while for 3 years are in the range of 7.50%-8.75%.

You see, while investing in debt market instruments it is imperative to know your time horizon in order to park your hard earned money in appropriate instruments.

You can also access Personalfn Car Loan Calculator here.

Add Comments