With the world turning deranged and petrified with debt-overload and timid economic growth in the developed economies, investors are wary of investing and diversifying across countries. With gloomy clouds and negative ripples sent across the global economy, along with de-coupling being far-fetched; it is time that our Indian friends residing abroad or Non-Resident Indian (NRI) investors search for economies with robust fundamentals, together with sensible policies and regulations in place.

While cocky over-confidence and exuberance is all good in the short-term, in the long-term it could provide only dismal returns. The present precarious economic situation in the developed economies is a reflection of being over-confident in the past, by resorting to printing more currency. And interestingly to uplift the economic sentiments, amid wobbly economic recovery - and in some countries such as Euro zone even with a negative growth rate, central banks are continuing to keep their policy rates low.

Table: Policy rates across nations

| Country | Policy rates (%) | Unchanged since |

| Japan | 0.10 | 5-Oct-2010 |

| United States | 0.25 | 16-Dec-2008 |

| United Kingdom | 0.50 | 5-Mar-2009 |

| Eurozone | 1.00 | 8-Dec-2011 |

| South Africa | 5.50 | 18-Nov-2010 |

| China | 6.31 | 7-Jun-2012 |

| India | 8.00 | 17-Apr-2012 |

| Russia | 8.00 | 23-Dec-2011 |

| Brazil | 8.50 | 30-May-2012 |

(Source: Central banks of respective nations, PersonalFN Research) Even now as talks of ‘Grexit’ (a term used for Greece’s exit from the Euro) looms around due to their anti-austerity stance, the only thing the European Central Bank (ECB) would do is print more Euros to bail out their ill members in the Euro zone. It seems that basic principles of printing currency could be challenged, thereby having a detrimental impact on inflation management and may do no good to the economic activity.

Although world leaders (through the G8 summit) are backing to keep Greece within the Euro zone and are taking all the necessary steps to combat a financial turmoil from happening, it is clear that views are different and thus even the division of views remain. Mr Fracois Hollande’s victory against Nicolas Sarkozy, the erstwhile French President, in a way reveals that the French people too aren’t ready for any budget -cutting austerity, and therefore while addressing to thousands of supporters Mr Hollande said that his victory was a rejection of austerity measures as the answer to the euro crisis.

Thus now amid this situation of debt-overhang in the Euro zone and fragile economic recovery in the U.S., all eyes are now focused on the emerging market economies (EMEs) - especially the BRICS (Brazil, Russia, India, China and South Africa). In fact we can say that, this turmoil could actually be in favour of EMEs, due to the relatively robust fundamentals they have to offer.

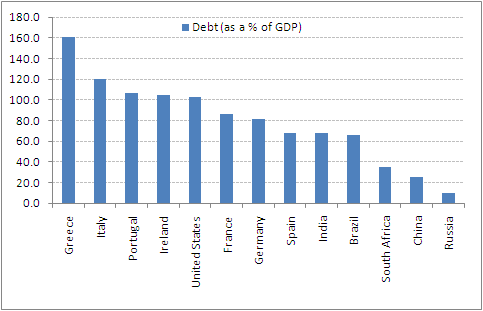

Debt-to-GDP

(Source: IMF Estimates, PersonalFN Research) If we compare the debt-to-GDP ratio of the BRICS Vs. Euro zone economies and also the U.S.; the chart above reveals that BRICs have a well-controlled debt-to-GDP.

Moreover, the economic growth rate which EMEs have to offer is far more luring than that clocked by developed economies. There are of course leaders and laggards in them, but nonetheless they look far more promising investment destinations. It is noteworthy that even the International Monetary Funds (IMF) estimates that nearly 70% of the world growth in the next five years would come from the emerging markets, with China and India accounting for more than 40% of this growth. But in comparison to China, India has demographic conditions which work in its favour. On the other hand China has a rapidly aging population, which could dramatically shrink its workforce; while India has younger population with talents galore.

That’s not all; there are other fundamental factors which make India an attractive investment destination for Resident as well as Non Resident Indian investors. These factors are:

- Prudent policy measures:

While ‘policy paralysis’ occurring at present may seem to have eroded the lustre from India, the policy measures adopted by the Government, thus far (especially during turbulent times), have been prudent to keep the growth momentum on in the country. Thus although many would denunciate the Reserve Bank of India (RBI) for keeping policy rates elevated and upsetting economic growth, the anti-inflationary monetary policy stances have produced the desired results of taming the inflation bug. Even now while Indian Rupee continues to be under pressure and breaches the Rs 56 mark to the U.S. dollar, amid speculation that a state-run company was buying greenback to repay overseas loans, and because of demand for oil imports; the central bank has stepped down to curb the volatility in currency movement. The RBI has already excluded banks’ net overnight open positions from currency futures and options segment. Moreover, it has also guided that foreign exchange future and options positions cannot be offset against Over The Counter (OTC) trades. It is noteworthy that RBI has capped position limit in the exchanges for trading currency F&O at $100 million or 15% of the OTC market.

On the fiscal policies (which feed into economic trends and monetary policy actions), while one may be dismayed with the fiscal deficit target not being met, NRIs should recognise that in developing economies the risk of deviation on fiscal deficit always exist, since infrastructure spending, education, industrial development and agriculture will always comprise a major composition of the budgeted expenditure. In the last Budget 2012-13, the Government has focused on strengthening financial sector reform, deepen the capital markets and bring in financial inclusion as well.

As far as Foreign Direct Investment (FDI) is concerned, we recognise that it is indeed required to fuel economic growth. Although in the recent past, the Government under pressure rolled back the FDI limit in multi-brand retail; it has once again proposed an increase (through the Budget 2012-13) in multi-brand retail limit to 51% after making efforts to arrive at a broad-based consensus with the state Governments. There seems to be realisation to the fact that increase in multi-brand retail can indeed help the nation and the retail industry due to inherent demographic advantage and strong consumption power. Likewise, assessing that the civil aviation is bleeding, the Government in power is also considering increasing FDI limit in the civil aviation sector. Moreover, in an attempt to provide aid to the airline industry (which is facing financial crisis), the Government has already permitted direct import of Aviation Turbine Fuel (ATF) by Indian Carriers. Also in order to address immediate financing concerns of the civil aviation sector, the budget 2012-13 has also proposed to permit ECB for working capital requirements of the airline industry for a period of one year, subject to a total ceiling of U.S. $1 billion.

Hence, although rating agencies may view the Government as the "single biggest drag" on the business activity, gradual policy measures are being taken by the central Government after evaluating the macro-economic environment. Having said that, we affirm to the view that economics has to be seen over politics, since only that can put the country on a reform path and not the myopic opposition.

In our view, while making investment decision, NRIs should look at policy measures adopted by the Government, while identifying economies for investing their hard earned money, since only prudent policy measures can provide gains in the long-run.

- Robust economic growth rate:

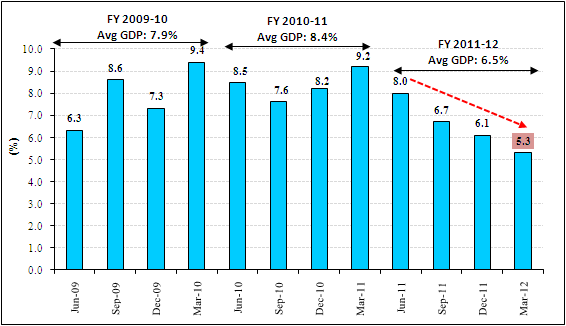

The economic growth posted by India, has thus trended in accordance to the policy actions taken.

India’s GDP growth

(Source: CSO, PersonalFN Research)

Although it has depicted a descending trend in current fiscal year amid Euro zone economic and political uncertainties along with certain domestic policies inaction, a noteworthy point is that the growth rate clocked by the Indian economy looks far more appealing when compared to the developed economies (see table below).

GDP growth rate clocked by DEs and BRICS

| Country/ Region | Average of Quarterly GDP Growth (%) |

| United States | 1.6 |

| Eurozone | 1.5 |

| India | 7.1 |

| Brazil | 4.4 |

| China | 9.3 |

| Russia | 4.3 |

| South Africa | 3.2 |

Data for C.Y. 2011 of respective countries

(Source: BEA, ECB, BCB, NBSC, Stats South Africa, World Bank, PersonalFN Research)

Also despite all the political backlash and uproar about policy paralysis, it is noteworthy that the Indian economy has been able to deliver average 6.2% GDP growth rate since 1980 - i.e. across 8 Governments.

It is noteworthy that the 12th five year plan has become effective from April 1, 2012 and so has the new manufacturing policy, thus going forward we may witness a quantum of shift in economic growth, if the opposition does not create myopic arguments impeding the path to economic growth.

- Renewed focus on infrastructure and agriculture:

Virtuous infrastructure would also be required to achieve economic growth rate. As long as focus on infrastructure spending is there it would attract foreign direct investment as well. The Government has already set its ball rolling on India’s infrastructure debt funds. Moreover, in the Union Budget 2012-13 the Government has highlighted the need for Public Private Partnerships (PPPs) and thus investment therein has increased. During the 12th Five Year Plan investment in infrastructure is expected to go up to Rs 50 lakh crore with half of this, expected to be from private sector. Also in order to encourage PPP in road, construction projects, in the Union Budget 2012-13 the Government has allowed external commercial borrowings (ECB) for capital expenditure on the maintenance and operations of toll systems for roads and highways so long as they are a part of the original project.

As far as agriculture is concerned, it remains a priority. Thus apart from increasing allocation towards Department of Agriculture and Cooperation, Rashtriya Krishi Vikas Yojana (RKVY) and various other agriculture schemes, the Government has also encouraged research in agriculture and thus a sum of Rs 200 crore has been set aside for incentivizing research with reward. Moreover, since food processing industry has been growing over 8% over the past 5 years, an agenda to start new centrally sponsored scheme titled "National Mission on Food Processing", is also in place.

This commitment to infrastructure and agriculture should also be considered by NRIs as path to long-term wealth creation while India remains on the path of long-term economic growth.

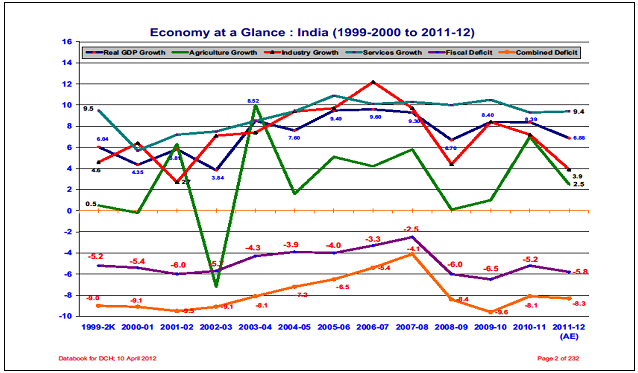

- Services industry taking the lead:

It is noteworthy that over the past few years the the services industry has played a major role services industry has played a major role in fuelling India’s economic growth. Thus if we assess the contribution of agriculture, industry and services to India’s GDP, it is services which has taken the lead (see chart below).

Services Industry taking the lead

(Source: Planning Commission Data book)

It is noteworthy that in the fiscal year 2011 Services GDP stood at 9.3%, and in the fiscal year 2012 too it is estimated to be at 9.4%. Thus it can be said that India stands out for the dynamism of the services sector. Moreover, year-on-year it has been depicting a steady growth and has been contributing about a quarter of the total employment. Thus now India’s rank (computed from UN National Accounts Statistics accessed on February 8, 2012) in Services to GDP is 11th in the world.

While population has always been construed as major threat, interestingly it is this growing population which has played a vital role in the growth of services theme in India. Moreover, from a demographic angle if we assess, it is the fairly young population (as compared to the countries in the developed economies), which has contributed to growth of this sector. The IT and BPO industry is a classic example of this. Likewise the banking & financial services sector, media & entertainment sector have also contributed a lion’s share in the progress of services sector in India.

- Robust consumption theme:

A supportive factor for inclusive economic growth which India has reported thus far is its robust consumption theme, favourable demographic conditions and inward looking economy.

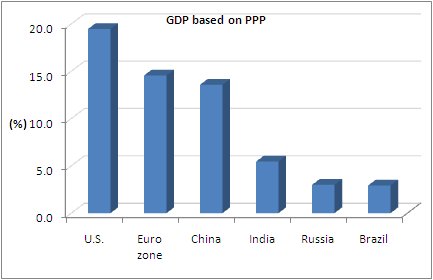

Chart: GDP based on Purchasing Power Parity (PPP)

(Source: World Bank, IMF PersonalFN Research)

It is noteworthy that today, India ranks 4th in global ranking for Purchasing Power Parity (PPP) at USD 3.78 trillion (according to data sourced from World Bank), and is the second fastest growing economy in the World. Moreover, in the fiscal year 2011-12 favourable demographic conditions have made a strong case with 70.1% of GDP being consumed internally. Even now although slowdown in the economic growth rate has occurred, it has not adversely dampened India’s consumption story.

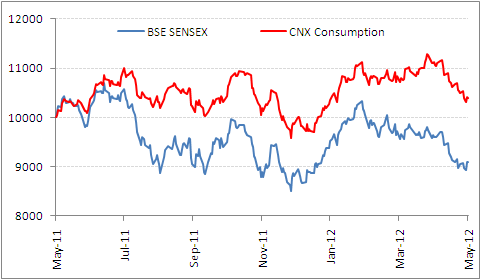

Chart: CNX Consumption Index Vs. BSE Sensex

Base: Rs 10,000

(Source: ACE MF, PersonalFN Research)

In fact, the chart above reveals that the consumption theme in India has done well (when compared to the benchmark Indian index). Thus say if one were to invest Rs 10,000 each in the CNX Consumption Index and BSE Sensex a year back (i.e. on May 25, 2011), one would have fetched a sum of Rs 10,385 and Rs 9087 respectively as on May 25, 2012.

As mentioned earlier, India’s demographic advantage has worked in its favour. The young population who take home good pay packages today and are willing to spend, has helped the consumption theme to contribute in GDP growth. Moreover, with their dependency on aging population being reduced due to them (young population) joining work force, the rise in disposable income within the family as well has also helped in this contribution. Along with rising income levels, easy credit availability has also assisted in growth. Rise in sales of consumer durable goods is a classic example of this. Today if one aspires to own a household appliance, car, home, personal gadgets etc. swiping credit card or easy financing options is the recourse if one affords it. This therefore has fuelled the consumption story, and it will continue to grow. It is this consumption theme well supported by favourable demographics, which in our view also makes India an attractive investment destination.

- Well regulated capital markets:

The Government reforms made in 1991 have enabled creation of effective regulations in the Indian capital market and also promoted sophistication in the way one transacts. Although there has been time when exuberance has been galore, it has been well shielded by effective and pro-investor capital market regulation as well, by all the regulators - be it Securities and Exchange Board of India (SEBI) or Reserve Bank of India (RBI) or even the Insurance Regulatory & Development Authority (IRDA). Moreover, efforts also have been take to preclude rampant mis-selling.

Thus there seems to be good understanding of the fact that for conducive growth, a healthy capital market regulation is indeed vital. Hence, today one can say that efforts have been made to make the Indian capital markets one of the safest in the world.

Also with companies adopting professional standards of management along with corporate governance practices, showing a far better improvement after its introduction in financial year 2000-01 (based on the recommendations of Kumar Mangalam Birla committee), the environment for direct investing in equity is also well self-regulated. Yes, the penalty(s) for poor discipline and unethical behaviour is fairly low as compared to developed countries, but regular audits on various aspects keeps a vigil. Moreover, the harsh stance adopted by the Finance Ministry to adopt General Anti-Avoidance Rules (GAAR) (though it has been postponed by a year) in order to curb the menace of black money, once again manifests the stringent regulatory environment in the country.

This is thus another encouraging factor why NRI investors should consider India as an attractive investment destination, which offers a robust regulatory environment along with some prudent investment avenues.

- Lucrative interest rates for fixed income market:

The interest rate scenario in India makes it a lucrative investment destination for risk-averse NRIs who are in search of preserving capital or their hard earned money. When compared to the U.S., Euro-zone and the other BRICS nations India offers high interest rates. For example a 1-Yr bank fixed deposits offer interest rates in the range of 7.25% - 9.25% p.a.

This lucrative coupon / interest rate scenario has thus contributed to fair amount of depth in Indian debt market, well supported by domestic investors as well as the Foreign Institutional Investors (FIIs). Today in the fixed income segment there are host of investment avenues available such as corporate bonds, corporate deposits, Government Securities, debt mutual funds, fixed deposit with a bank and non-convertible debentures; in which even you can invest as NRIs.

All you need is one of the following accounts to make an investment in the above mentioned fixed income securities:

- NRE (Non-Resident External Rupee) Account: This account is a bank account which allows the transfer of your foreign earnings to India. You can repatriate the funds held in the account along with the interest earned at any point of time. This is a rupee denominated account, which is opened by depositing foreign currency at the time of opening a bank account and the funds in this account are required to be maintained in Indian rupee only. The source of the funds to this account needs to be from your foreign exchange earnings or from another NRE account. As far as the tax treatment of the interest earned on this account is concerned, it is totally exempt from income tax and the credit balance in the account does not attract any wealth tax either.

- NRO (Non-Resident Ordinary) Account: This account operates like a normal bank account opened by an Indian going abroad with the intention of becoming an NRI. Such an account is opened with the intention to send remittance or transferring funds from your NRE / FCNR account held in other banks in India. It offers the same facility like the NRE account, except that repatriation done through this account should be reported to RBI by filling up prescribed forms. Also, from a taxation perspective, the interest earned on this account is liable to income tax.

- Foreign Currency Non Resident Deposit Account: This account is in the form of term deposit of 1 to 5 years, which allows all credit and debits like in the NRE account. Moreover, FCNR account allows one to maintain the account in freely convertible currency, as one can hold their deposit in any of the 6 foreign currencies - U.S. Dollars, Pounds Sterling, Euro, Japanese Yen, Australian Dollars and Canadian Dollars. One can fully repatriate principal and interest and even enjoy tax exemption on the entire deposit. FCNR account also allows you as an NRI to avail a loan upto a sum of Rs 1 lakh against the security of funds held in this account.

Moreover, the present depreciation of the Indian rupee vis-à-vis the U.S. dollar is good news (although negative for India per se) for you NRIs, because the appreciation in the foreign currency has enabled in getting more bucks for your money brought into India. Moreover to add a cherry on the cake, the increase in interest rates offered by NRE, NRO and FCNR accounts is like a cherry on the top. But a flip side to that is the currency risk when you repatriate your money abroad, where further deprecation of the Indian rupee could erode your gains from high interest rate.

India can still offer long term investment benefits for NRI’s

Hence, there are galore of long-term benefits of investing in developing economy such as India, which is the second fastest growing economy in the world. The demographic advantage (with more young population) adds synergy to economic growth, which thus can lead you NRI Investors on the path of wealth creation as well. However, having said that, it is imperative that NRI Investors adopt enough prudence investing and invest across various asset classes. In our view, where you NRI Investors invest should be a function of your investment objective and risk profile (amongst other factors) for you to invest appropriately.

In India, the strong fundamentals, present valuations of the Indian equity markets as well as the high interest rate regime makes it an opportune time to invest in this country, which offers promising growth prospects. Likewise, for your alternative investment portfolio, the real estate market in India too looks appealing given the rampant emphasis on infrastructure growth and spending. However, before investing we recommend you NRIs to be well-versed with the tax implications and then make a prudent choice.

This NRI article by PersonalFN was written exclusively for Quantum Mutual Fund for the NRI section on its official website www.quantumamc.com. Quantum Mutual Fund is India’s first dedicated, direct-to-investor mutual fund.

Disclaimer:

This note / article is for information purposes and Quantum Information Services Limited (PersonalFN) is not providing any professional / investment advice through it. The facts mentioned in the note are believed to be true and from a reliable public source. The Service should not be construed to be an advertisement for solicitation for buying or selling of any scheme / financial product. PersonalFN disclaims warrants of any kind, whether express or implied, as to any matter/content contained in this note, including without limitation the implied warranties of merchantability and fitness for a particular purpose. PersonalFN and its subsidiaries / affiliates / sponsors / trustee or their officers, employees, personnel, directors will not be responsible for any direct/indirect loss or liability incurred by the user as a consequence of his or any other person on his behalf taking any investment decisions based on the contents of this note. Use of this note is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. PersonalFN does not warrant completeness or accuracy of any information published in this note. This note is for your personal use and you shall not resell, copy, or redistribute this note, or use it for any commercial purpose.

Add Comments

| Comments |

ifa@smartbrief.com

Jul 25, 2012

As is the case in a lot of areas, gov.sg does the kiasu (literally, scare to lose ) multi-pronged thing, including stuff like : fines, CWO's (corrective work orrdes a form of public punishment), and for a time littering offenders even had their 15 minutes of fame in the local mass media!However, there are limits to government intervention. Once out of their own country, the Ugly Singaporean comes into play, joyfully littering in other countries (!!)Hence, promoting education and cultural change would be the better long-term solution. But this kind of thing takes time. |

1