“It is health that is real wealth and not pieces of gold and silver”—Mahatma Gandhi

India faces the challenge of a triple burden of disease—rising Non-Communicable-Diseases (NCDs), dominant infectious diseases, and other health injuries.

In 2015, the Insurance Regulatory and Development Authority of India (IRDAI) mandated the Federation of Indian Chambers of Commerce and Industry (FICCI) to constitute a task force to review the existing definitions of critical illness and also to identify and define new conditions.

According to the FICCI Health Insurance Committee’s report published in December 2015, cardiovascular diseases, cancers, chronic respiratory diseases, kidney failure, and other Non-Communicable-Diseases (NCDs) are estimated to account for 60% of total deaths in India. Furthermore, NCDs account for about 40% of total hospitalisations and roughly 35% of all recorded outpatient visits. Stress, poor diet, and lack of exercise, all banes of modern life are now exposing more and more Indians to critical illnesses each year. This, coupled with the increasing cost of treatment has made recovery an expensive journey.

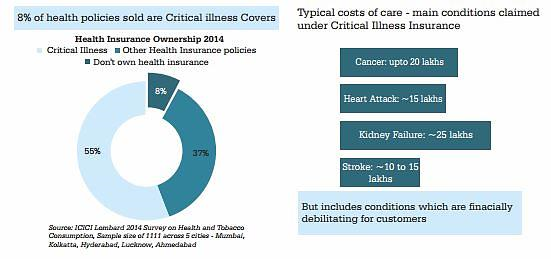

Health insurance in India is estimated to be Rs 21,000 crore (as on March 2015); however the main product sold is hospitalization indemnity cover (sold as a generic “Mediclaim” category of product). The lack of investor awareness and complex communication about the plan's benefits is the primary reason critical illness plans see fewer takers. While the market statistics on the number of critical illness policies and sum insured are not available, a 2014 market research survey estimated that only 8% of health insurance buyers purchased critical illness. However, the most common causes of claims include conditions that are financially debilitating for the consumer as shown in the picture below:

(Source: FICCI Health Insurance Committee Report, 2015)

Critical illnesses may lead to loss of income, changes in lifestyle, and even permanent disability. At times, the expenses incurred for the treatment of the ailment are so high (as shown above) that it isn't covered under a regular health insurance policy. In such situations, critical illnesses policies come to one's rescue.

But before you purchase a

critical illness policy, make sure to go through the common man’s checklist –

| Parameters |

Ideal Solution |

| Entry Age |

The higher the entry age the better it is as it gives you the necessary flexibility to purchase the policy at a later stage too. |

| Renewal Age |

The higher the renewal age the better it is. |

| Sum Insured |

Should be at least 5 times your current gross annual income + any outstanding debts |

| Survival period |

The claim will be settled after the survival period so lesser the survival period the better it is |

| Tax Benefit |

Should provide benefit under Income Tax |

| Free look in period |

Higher the free look in period the better it is, as it gives you the cushion to return the policy if doesn't match your expectations. |

| No. of diseases covered |

The policy should extensively cover a wide range of illnesses |

| Waiting period |

The critical illness cover begins after the waiting period is over. Lesser the period the better it is |

| Claim process |

It is ideal to choose that insurer who has a hassle free claim handling process. Remember, it's your loved ones who will have to follow-up. |

| Premium |

Premium is the consideration you pay for getting the cover. An extensive cover with low premiums is always better to go for. |

(Source: PersonalFN Research)

Some of the best critical illness plans for an individual male, aged 34 are as follows:

| Insurer and Plan |

Key Features |

Medical Check-up |

Sum Assured (Rs) |

e-Policy premium (Rs) |

| Apollo Munich Health Insurance—Optima Vital |

37 diseases covered |

Not required |

20 lakh |

8,624 |

| Bharti AXA—Smart Health Critical Illness (Lump sum) |

20 diseases covered. No claim bonus of 5%. Family option available. |

Not required |

5 lakh |

1,713 |

| PNB MetLife—Major illness premium back cover |

35 diseases covered. Return of premium option. 5% online discount |

Not required |

20 lakh |

25,919 |

| Reliance General Insurance—Reliance Critical Illness |

10 diseases covered. No claim bonus of 5%. 1 year and 3 year payment option |

Not required |

10 lakh |

3,147 |

| Max Bupa Health Insurance—Health Assurance Critical Illness |

20 diseases covered. No claim bonus of 5%. Riders available |

Not required |

10 lakh |

3,161 |

| HDFC Ergo—Critical Illness Plan |

8 diseases are covered. High claim settlement ratio |

Not required |

10 lakh |

3,449 |

Note: The table above is indicative, not exhaustive. Read the proposal documents carefully to make a prudent choice.

(Source: policybazaar.com)

Conclusion – The threat of facing a major ailment is always present considering today's lifestyle which comprises of long working hours, stress, lack of physical exercises, skipping of meals, junk food, alcohol, and smoking. This lifestyle is the primary reason that a critical illness cover is required today to take care of not only the rising treatment but also the lifestyle expenses. We at PersonalFN understand that choosing a critical illness policy could be daunting and so it would be prudent to engage the services of a financial planner who will take into account host of factors before recommending an appropriate critical illness policy with an optimum cover.

Add Comments