Impact

While patients suffering from diseases show symptoms, it is equally true that some of the symptoms emerge at a much later stage. In finance and economics the health of an economy is often gauged through resilience country’s currency depicts. But sometimes, strength or weakness of a currency can be disguising.

So while the Indian Rupee (INR) has shown resilience against the greenback, let us understand whether the value of rupee is disguising or there are genuine and fundamental reasons that support the rupee.

Rupee Domination

If Financial Year (FY) 2012-13 and FY 2013-14 were the years of debasement for the INR, the present fiscal has been a year of consolidation for INR. In the fiscal so far, INR has emerged as one of the strongest emerging market currencies against U.S. Dollar (USD).

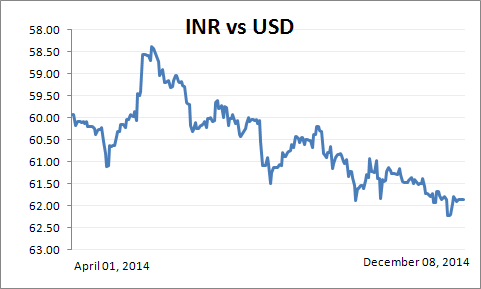

How has the Indian rupee fared

|

| Currency |

Performance against USD |

|

From 01-Apr-2014

To

08-Dec-2014 |

| Indian Rupee |

-3.2% |

| Turkish Lira |

-6.1% |

| South African Rand |

-8.4% |

| Indonesian Rupiah |

-9.5% |

| Brazilian Real |

-14.4% |

| Russian Rouble |

-49.3% |

|

Data as on December 08, 2014

(Source: Bloomberg.com, ACE MF)

So, let’s recognize that what has resulted in the Indian rupee to be moving in a narrow range…

The Federal Reserve (Fed) in the U.S. ended the bond-buying programme in October 2014 believing that U.S. economy was set to get back on track. It was also anticipated that, the labour market conditions may improve going forward. And as expected then, job market data for November 2014 has been robust, with the unemployment rate having reduced to 5.8% and jobless claims dropped to a 6-year low. The U.S. has not only seen improvement in hiring but has also witnessed wage hikes. Such signs of economic vigour depicted by the U.S. economy has pushed USD to a 5-year high.

But then, the INR amongst the emerging market economies has depicted enough strength as well. This is because….

- Inflation has mellowed down (both at wholesale and retail level);

- Expectation are high that economic growth would revive with Mod-led-NDA Government in power;

- Interventions of the Reserve Bank of India (RBI) in the forex market; and

- Improving Current Account Deficit (CAD)

CAD so far and going forward….

From the record high level of 6.7% a couple of years ago, India’s CAD has fallen steadily providing major relief to INR. For Q2FY15 it has widened to U.S. $10.1 billion from U.S. $7.8 billion in the previous quarter, as per a statement released by RBI. The gap amounts to 2.1% of the GDP, which has resulted on account of slowdown in exports (due to recession in Japan and gloomy economic outlook for the Eurozone) and surge in gold imports (soared a whopping 280.4% in October 2014 at U.S. $4.2 billion, against U.S. $1.1 billion a year earlier). But it is not much a concern as the data is yet lower than 2.5% which the central bank considers sustainable. Moreover, the Balance of Payment (BoP) is in surplus of U.S. $6.9 billion for Q2FY15, it being the fourth consecutive quarter of surplus, although lower than U.S. the $11.2 billion surplus in the previous quarter. Also, crude oil which is the principal item in the import bill and which usually contributes to CAD in a big way (as India imports about 80-85% of its requirements) has softened by more than 40% since June 2014.

RBI interventions so far and way forward….

With an aim of minimising volatility in the value of rupee, RBI has actively intervened in the forex market. After nose-diving in 2013, INR slowly recovered; thanks to monetary and administrative measures taken by the RBI and the Government from time to time in this regard. RBI kept selling dollars in the forward market which led to INR move in narrow range. You see, between January 2014 and October 2014, RBI bought approximately to the tune of over USD 38 billion in the forward market. However, as a side effect of that forward premiums shot up in the forward market and Indian companies having exposure to foreign debt started keeping their positions unhedged to avoid higher costs associated with hedging. As rupee started stabilising due to active interventions of RBI, Indian companies started feeling confident. But in turn, dollar debt of Indian companies surged to unprecedented levels. From USD 224.4 billion in 2008 external debt of Indian companies rose to about USD 450.1 billion in June 2014. As observed by RBI, hedging ratio fell to mere 15% in July-August this year. The cost of hedging went as high as 8.0% to 8.5%...and RBI has already expressed its concerns on this subject. Due to any unforeseen global event if rupee takes a hit again, unhedged dollar denominated debt might create problems. It is believed that, to discourage companies from keeping their forex exposure unhedged, RBI may stop intervening in the forward market and shift to the spot market. But since this has a rippling effect on inflation, one need to watch the effect and the action RBI takes to keep inflationary pressure under check. As RBI remains committed on it anti-inflationary stance, the intervention in the spot market may be limited. Besides, sudden and high outflows of USD from capital markets may make job of RBI even tougher.

Lowering Inflation and inflation expectations

Massive fall in crude oil prices globally has provided much needed relief on inflation front. Deregulation of diesel helped pass on the benefits to the end user thereby reducing the overall price pressures. Inflation measured by the movement of Wholesale Price Index (WPI) for October 2014 fell to 1.77% marking a 5-Year low. Similarly, consumer inflation also registered its all-time low of 5.52% since the new data series started in 2012. But as vegetable and fruit prices have been falling for some time now, the phenomenon is more seasonal rather than structural as noted by RBI. Furthermore, it is noteworthy that, inflation in vegetable prices has dropped in negative for the first time in last many months. But considering sharp drop in vegetable prices at wholesale level, fall in prices at the retail level appears negligible. Also this year, kharif crop is expected to be about 7% lower than harvested last year, causing threat to food prices. In the 5th bi-monthly monetary policy statement, 2014-15 (released on December 02, 2014), RBI also expressed the similar views. As per the assessment of RBI, there are several upside risks to food inflation stemming largely from loss of Kharif crops due to lower than normal monsoon and unlikeliness of Rabi crop compensating for the decline in Kharif crop. Likewise, prices of egg, fish and meat have fallen at wholesale level, but at the retail level buyers are yet to benefit. This in turn suggests that, phenomenon of falling inflation is more complex than it appears.

As crude oil prices have dropped below USD 70 per barrel, inflation expectation has lowered significantly. However, there is an upside risk, as always. If crude oil prices start shooting up again, for any foreseen reasons, India might re-witness the occurrence of high inflation.

If inflation fails to stay lower, it may eventually start affecting capital inflows especially in debt markets, thereby putting pressure on INR.

Economic growth

India’s GDP grew at 5.3% in July-September quarter of Financial Year (FY) 2014-15. Although growth registered by world’s third largest economy is a tad lower in the second quarter as compared to that in the first quarter of the current fiscal; it is much in line with the full-year estimate of 5.5% given by RBI. During the Q2 of FY 2013-14, Indian economy had grown at 5.2%. Although it is expected that, economic growth may gather pace going forward, at present it is contingent upon several factors.

The future of Indian economy largely hinges on how some of the important segments of economy do. Manufacturing growth has been subdued and remains a key concern. While healthy growth in services has been making GDP look better than what it could have otherwise been, had services also done poorly just as manufacturing. Having said this, there is a limit to which services can grow in absence of strong performance of other segments of economy. Therefore, PersonalFN believes, for the Indian economy to grow at a higher rate, revival in manufacturing and strong performance of agriculture sectors are the prerequisites. Stagnant Private Final Consumption Expenditure (PFCE) and Gross Fixed Capital Formation (GFCF) remain a concern.

Going forward, industry may look forward to reforms and other Government initiatives besides favourable interest rates and lower inflation. The Parliament has approved labour laws that redefines small factories and frees small companies from furnishing separate labour returns. It is expected that, with improvements in the labour laws manufacturing growth may get a boost and entrepreneurship would be promoted. Moreover, the Government has cleared more than 230 projects over last 6 months which were stuck for environment clearances. In another development, the Government placed an order for nearly 2,400 rail wagons indicating its thrust on infrastructure development. RBI envisages 5.5% growth for the current fiscal year. On the other hand, International Monetary Fund (IMF) has revised growth of India’s GDP upward by pegging it at 5.6%.

PersonalFN is of the view that, so far macroeconomic conditions and steps taken by the Government have contributed to the resilience of the Indian rupee. But there may be some hiccups in the interim. How RBI and the Government handle macro-economic conditions remains the key to rupee strength. More than domestic factors, global factors such as dollar strength, prices of crude oil and those of other commodities need to be watched closely. Currency value and capital flows are interrelated and falling currency further triggers capital outflows. To clock high economic growth reform measures are vital along with prudent monetary stance from RBI which in turn can keep the INR strong against the greenback.

Add Comments