Mutual Fund direct plans are the first choice of do-it-yourself investors. The reason is simple, direct mutual fund investment eliminates the need of a distributor. Hence, it not only saves on transaction costs if any, mutual fund direct plans come with lower fees. While the difference in costs may seem negligible at first, but over time—thanks to the magic of compounding—the difference in value terms works out to lakhs of rupees.

To know more about mutual fund direct plans and the benefits of direct mutual funds, do read though this guide first: Mutual Fund Direct Plans - Everything You Need To Know

In this article we delve deeper on how to buy direct mutual funds or rather how to invest in direct plans of mutual funds. Many of you may be wondering from where to buy direct mutual funds, as the option of direct plans is not available with your local mutual fund distributor or stock broker. Hence, you need to invest in direct mutual funds online through an investment advisor or the mutual fund's website or MF Utilities.

If you wish to invest offline, you will may need to visit the office of the Mutual Fund company or their registrar such as CAMS or Karvy MFS. Therefore, if you wish to invest in schemes of HDFC Mutual Fund or SBI Mutual Fund or Reliance Mutual Fund or any of the 40-odd fund houses, you will need to visit their branch to submit the application form and payment. Or else, you will need to visit the office of the fund's registrar.

So along with your pursuit to select the best direct mutual funds, it will be of some benefit to check out the different options for direct plan investments. Do have a look at the different direct mutual fund platforms. Opt for one that is backed by strong research and services.

Navigate through the article with the help of the links provided below:

How to Invest In Direct Mutual Funds Online?

You can invest directly in mutual funds online through multiple options. But before you start, keep your PAN, Aadhaar, bank account details (account number, IFSC code, MICR, etc.) and online banking transaction login details ready.

|

Please note: First-time mutual fund investors will need to complete their Know Your Customer (KYC) formalities first. Mutual Fund KYC can be completed online in a few easy steps and needs to be done just once and can be used across all platforms. You can complete your KYC offline as well by visiting the fund house or registrar.

|

Also read: 5 Easy Steps To Become KYC Compliant

The KYC is linked to your PAN number, hence, when investing through different platforms they first check if your KYC is completed using your PAN details.

Once done with the KYC formalities you may invest through any of the routes below. Choose the one you feel is most convenient.

Invest in direct plans through mutual fund house website

Once you have decided in which fund to invest, you could invest in mutual fund schemes directly through the online portal of the Asset Management Company.

For instance, if you wish to invest in Fund A, you can go to its fund house website and buy the fund units online.

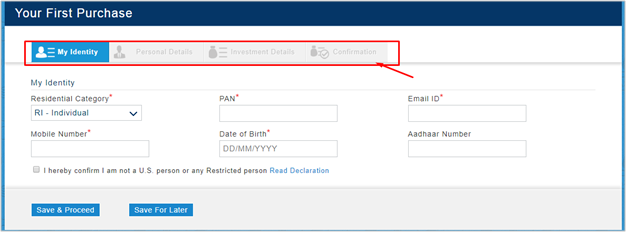

If your KYC is complete, you may follow the below steps.

(Source: quantumamc.com)

(Source: quantumamc.com)

- Register account with the mutual fund company

Most mutual funds will require you to create an account first. The personal details that are required are similar to that required in the mutual fund application form. Some fund houses may ask you for a basic registration first and then a detailed registration when completing the transaction. The process would vary from one fund house to another.

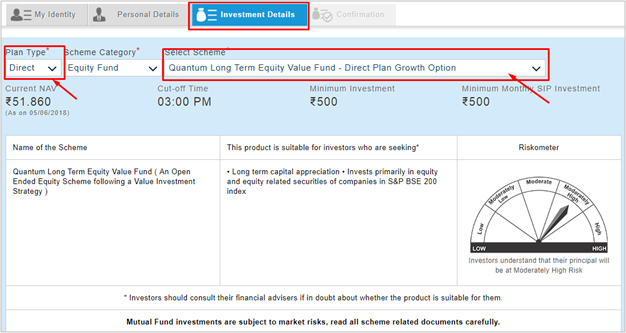

- Choose the desired scheme and investment details

When you come to the investment section of the online from, do ensure you select the Plan Type as ‘Direct’. Also double-check the scheme option. Under direct plan, you will get the Growth or Dividend Option. Choose the option that conforms to your financial goals.

(Source: quantumamc.com)

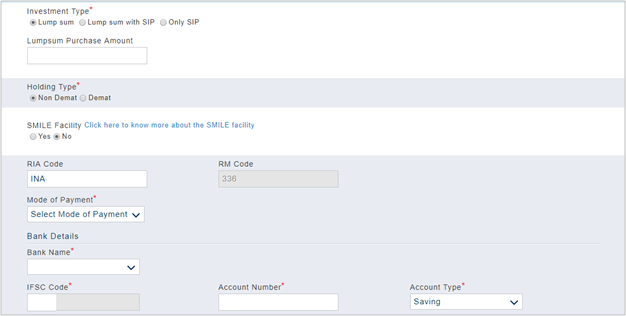

You will also need to enter the investment details such as the

Investment Type – Lumpsum, one-time payment or through a Systematic Investment Plan (SIP),

Holding Type – Non-Demat or Demat,

RIA Code – If availing the services of a Registered Investment Adviser,

Mode of Payment – Net banking, NEFT, Debit Card, IMPS etc. This options will differ across AMCs.

Bank Details – Bank name, IFSC Code, Account Number, Account Type. You may also be asked to confirm the branch address and MICR code.

- Verify and complete transaction

After submitting the above, you will be asked to verify the details. Many overlook this and proceed ahead. It is best not to proceed hastily and take time to read the form carefully. Many a times there are typo errors in the bank account number. Getting it changed later is a tedious task. Hence, try to avoid such mistakes early on.

You may also need to authenticate the form submission through a One Time Password (OTP) that is sent to the registered mobile number or email id. Some fund houses may complete this authentication process as the first step.

(Source: quantumamc.com)

Once successfully verified, you can complete the transaction on the next page using mode of payment opted for earlier. You will be provided a Transaction Reference Number. Note this down, as it may be helpful if an error occurs in the transaction process. Once the payment is completed successfully, you will receive a confirmation on your email, mobile or both.

The above process completes your investment in direct plans if mutual funds through a specific fund house. Broadly, the process remains the same.

For additional purchases in direct plans of a fund house, you will not need to enter all the details again. All you need to do is login to the online account, pick the desired scheme, choose the desired investment amount, and complete the transaction.

|

Please note: You should opt for investing in direct plans at a fund house level only if you are investing across a few fund houses. Else maintaining account details across multiple fund houses can lead to operation nightmares. If you are investing in schemes of multiple fund houses, it will be best to opt for a platform through which you can get access to most major fund houses, if not all.

|

Invest in direct mutual funds through Registrar & Transfer Agent (R&TA)

The registrars also facilitate online investing in mutual funds, however, the investment will be limited to the mutual funds registered with them.

You can either visit the CAMS or Karvy website and invest in schemes of your choice.

List of Mutual Funds serviced by CAMS

|

Aditya Birla Sun Life Mutual Fund

DSP BlackRock Mutual Fund

HDFC Mutual Fund

HSBC Mutual Fund

ICICI Prudential Mutual Fund

IDFC Mutual Fund

IIFL Mutual Fund

Kotak Mutual Fund

|

L&T Mutual Fund

Mahindra Mutual Fund

PPFAS Mutual Fund

SBI Mutual Fund

Shriram Mutual Fund

TATA Mutual Fund

Union Mutual Fund

|

List of Mutual Funds serviced by Karvy

|

Axis Mutual Fund

Baroda Pioneer Mutual Fund

BOI AXA Mutual Fund

Canara Robeco Mutual Fund

DHFL Pramerica Mutual Fund

Edelweiss Mutual Fund

Essel Mutual Fund

IDBI Mutual Fund

India Bulls Mutual Fund

INVESCO Mutual Fund

|

JM Financial Mutual Fund

LIC Mutual Fund

Mirae Asset Mutual Fund

Motilal Oswal Mutual Fund

Principal Mutual Fund

Quantum Mutual Fund

Reliance Mutual Fund

Taurus Mutual Fund

UTI Mutual Fund

|

As can be seen in the table above, all of the major fund houses are covered, except Franklin Templeton Mutual Fund and Sundaram Mutual Fund. Both these fund houses operate through their own registrar.

CAMS offers a service known as myCAMS, through this service you can make one-time investments in mutual funds, set up Systematic Investment Plan (SIP), opt for Common One Time Mandate (OTM) and other facilities across Mutual Funds serviced by CAMS through a single account.

You can transact in mutual funds serviced by Karvy here. However, as per the website, the facility is available only for online additional purchase, redemption and switch.

|

Please note: Though CAMS is the most convenient of the two registrars for online purchases, if you plan to invest in mutual funds apart from those serviced by CAMS you will need to opt for different routes for those funds. This can again cause inconvenience to you as an investor. It will be best to have all mutual funds under one roof.

|

Buy Direct Mutual Funds through Mutual Fund Utilities

Mutual fund transaction portal, MFU (Mutual Fund Utilities) is a single window for you to transact across mutual fund schemes.

Mutual Fund Utilities is a shared platform of different fund houses. You need to create an account first, before transacting and you can transact in mutual funds of almost all the AMCs. Using a Common Transaction Form (CTF) or through the online portal you can invest in multiple funds of different fund houses.

Moreover, there is no additional charge for mutual fund investments made through this portal. The cost of the platform is shared by the participating fund houses.

Most of the major fund houses are a part of this platform, hence, it eradicates the cons of the above routes where the mutual fund investment universe is limited.

To invest in direct mutual funds via the MFU platform, you will first need to create a CAN (Common Account Number). CAN is a unique reference number issued by MFU. The CAN will map all your existing mutual fund folios across fund houses (participating in MFU), thereby providing you with a consolidated view of all your mutual fund investments.

This is similar to a Mutual Fund Folio, the only difference, while the folio is limited to one fund house, the CAN is applicable across fund houses of a single type of holding.

You can create and e-CAN online. Follow the simple process outlined here - 3 Steps to Generate Your Mutual Fund e-CAN

Once you have created your CAN, you can signup for online access through their portal - https://www.mfuonline.com/. You will need to create a User ID and setup a password for the account.

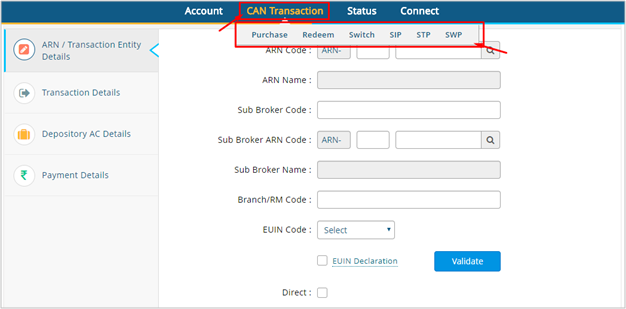

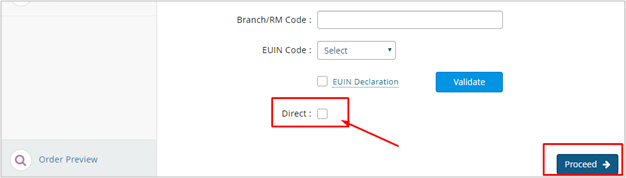

Once logged in, you can begin transacting in the account by clicking on CAN Transaction as highlighted below. Choose Purchase for a lumpsum investment or SIP if you would like to start and SIP. If you are investing in Regular Plans and wish to switch to Direct Plans, you can use the Switch option.

(Source: MFUonline.com)

Choose Direct and click Proceed. You may be asked to enter details of the RIA if any. If you have not availed of an RIA you can leave the form blank.

(Source: MFUonline.com)

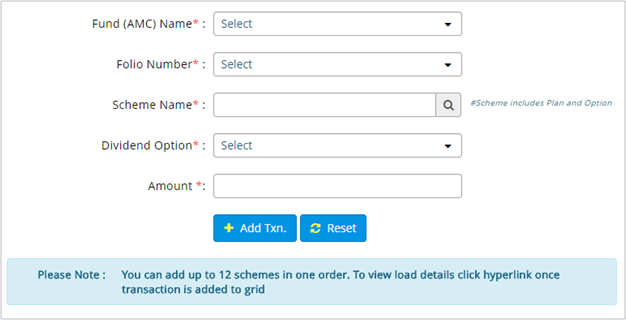

You will then be asked to enter details of the investment. You can even invest in as many as 12 schemes at one go. Ensure you select the correct scheme option.

(Source: MFUonline.com)

Once you have added all the fund details, you may complete the transaction on the next page.

|

Please note: MF Utilities is one of the best options for do-it-yourself investors. The best part is that the portal is entirely free and you will get access to a wide range of mutual fund schemes. However, it is good only as a transaction platform. If you are seeking further analysis on your portfolio if may not be possible. If you are seeking advice on your investments, you may need to opt for a direct mutual fund platform or a robo-advisory.

|

Invest in Direct Plans of Mutual Funds online through an Investment Adviser or Robo-adviser

There are multiple aspects to look at when investing in mutual funds, such as:

-

Setting realistic and measurable goals

-

Investing as per your risk profile

-

Adopting the right asset allocation strategy

-

Picking the right mutual fund schemes

-

Regularly reviewing your portfolio for changes in the scheme's investment attributes

-

Tax implications on redemptions

-

Monitoring your goals regularly and making appropriate changes

When investing through direct plans, you need to manage all this yourself or opt for the services of a fee-based financial planner or investment advisor. Over the past few years, the way we invest and the way we receive advice has changed drastically and for the better.

A new form of investment advisory has emerged – robo-advisors. These online platforms use technology that runs complex algorithms to develop automated customised portfolio allocation and investment recommendations.

These platforms are convenient, engaging, and simple to use. Some robo-advisors are able to attract clients with their attractive low costs and offer direct plans. Some even claim it to be a free service or virtually free.

However, under mutual funds, there are hundreds of plans available under the different categories. A good and unbiased robo-advisor will help you separate the wheat from the chaff.

In other words, the robo-advisor needs to select mutual funds backed by sound research. Performance should not be the only criteria. There are different qualitative and quantitative parameters that need to be looked at before arriving at the top schemes.

PersonalFN's soon-to-be-launched robo-advisor may be your best bet.

Backed by its massive experience of well over 15 years in the financial market, PersonalFN has come up with an exclusive virtual investment advisor, uniquely built in such way that it knows the market -- and above all, it knows YOU!

You just got to follow these simple steps below:

-

Complete the registration

-

Submit necessary documents to activate your investment account

-

Assess your risk profile

-

Get a recommended portfolio based on your inputs

-

Invest with a single click

More reasons why you should invest through PersonalFN's robo advisory platform

-

It can help you reap extra returns since it provides only Direct Plans.

-

It brings outstanding research experience of over 15 years. (Outperforming the BSE-200 index by 80 percent!).

-

It comes at a pocket-friendly price.

How To Buy Direct Mutual Fund Offline?

If you decide to invest in mutual funds directly, here are the different paths:

- AMC or Registrar office: Once you have decided in which fund to invest, you can visit the nearest AMC office or the office of their registrar to invest in the mutual fund. Here is a list of AMC offices.

The process is simple. Fill in the Common Application Form / SIP form carefully and completely, mentioning the name of the mutual fund scheme and other details. If investing through SIP, provide your NACH mandate form stating all details of your SIP.

Hand over the forms (as mentioned above) to the office of the Registrar and Transfer Agents (RTAs) / AMC.

- Mutual Fund Utilities: Mutual Fund Utilities is a shared platform of different fund houses. You need to create an account first, before transacting. We explain how you can create a Common Account Number (CAN) here. You can transact in mutual funds of almost all the AMCs. Through a single transaction form, you can invest in multiple funds of different fund houses. You can download the required forms from the MF Utility website here.

In case you are investing through MF Utilities, you need to submit the PayEezz form. PayEezz is a facility offered by MFU, where an investor can register a one-time mandate and provide a standing instruction to his banker authorising MF Utility to debit his/her account for future subscription transactions (Lump sum or SIP).

By registering under PayEezz, investors need not issue cheque or other payment instructions every time they make an investment through MFU. There is an upper limit mentioned in the PayEezz mandate.

Once a PayEezz is successfully registered and the PayEezz reference Number (PRN) is communicated by MFU, investors are free to register any number of SIPs quoting the same PRN. However, investors/distributors/RIAs should note that the cumulative debits in a day cannot exceed the maximum limit mentioned in the PayEezz mandate.

- Investment Adviser: If you hire the services of a fee-based investment adviser, you may send over your transaction documents to them to begin investing in mutual funds. Your investment adviser will also receive newsfeed from the fund house and they can keep track of your mutual fund investments.

How To Select The Best Direct Mutual Fund Platform?

A visit to the website of any robo-advisor (by the way, ‘robo-advisor’ is the nickname for automated money management services) will leave you awed with the interactive user interface. Each provider will claim the ease of use, advanced technology, low costs, and so on. Many offer direct plans as the lower costs attracts investors, but they charge a fee for their services.

Over the past few years, many such direct mutual fund platforms have cropped up. So, how do you separate the wheat from the chaff?

PersonalFN has outlined five steps to zero-in on the right robo-advisor.

Step 1: Identify your need

Financial planning services can vary from simple goal-based planning, to a more comprehensive service of managing your debt and cash flows. Most robo-advisors today are only equipped to handle the former.

So before you get your expectations too high, remember that a robo-advisor may only be able to automate your investments towards new financial goals.

Therefore, if you have not started actively saving and investing towards any financial goals or if you are planning to add new investment goals, then robo-advisors are for you.

Here again, robo-advisory platforms come with different options – some may offer complete automation, while others may offer hybrid services that pair the computer algorithms with financial planners. You need to choose wisely.

If you are looking for simple goal-based planning, the former may help. But, as your investment portfolio and financial needs grow, you may someday require the services of a human advisor or a Certified Financial Guardian. Hence, it would be prudent to select a robo-advisor that offers advanced financial planning (with human interaction) as an add-on service.

Step 2: Shortlist only SEBI-registered investment advisers

Once you have decided on the ‘type’ of robo-advisor, you need to shortlist such platforms and make sure they are registered as ‘Investment Advisers’ under the Securities and Exchange Board of India (SEBI).

SEBI has laid out stringent guidelines to ensure that investment advisors – both online and offline – offer only ‘suitable products’ to their clients, with proper risk profiling. Under the regulations, the advisor also needs to divulge any conflict of interest in the advice provided.

You need to be wary of mutual fund distributors who act as robo-advisors. Though some may offer the platform free, they earn a commission from the mutual funds they suggest. Hence, there is a conflict of interest and the investment advice may not be completely prudent and unbiased.

Step 3: Take the free trial or free membership

Most robo-advisors allow you to create a free account to explore their services. Some offer the entire platform free, as they earn from commissions. So before you commit your money, either by subscribing to the service or making an investment, you can first take a test drive of the platform.

Doing this, will ensure you get a feel of their platform – whether the user interface is friendly and easy to understand, and if it is free from technical glitches. Though glitches may arise once you start transacting, it will be better if you confirm that the platform moves smoothly before any monetary commitment.

Step 4: Rate the robo-advisor on 5 important criteria

Once you have tried and tested the robo-advisors, it’s time you evaluate them. PersonalFN has outlined five important criteria…

- Service offerings

As mentioned earlier, some robo-platforms may offer you only transactional services, while others may provide you with a host of offline and online personal finance offerings. In addition, some robo-advisors may offer advanced tracking and portfolio rebalancing services. Those that offer a mix of services should be worthy of your long-term financial commitment. However, you need to keep an eye on costs too. Robo-advisors offering advanced services as an add-on subscription will go easy on your pocket as compared to those that charge a lumpsum package.

- Unbiased and research-backed advice

Most robo-advisors will suggest investing in mutual funds as these are the most convenient instruments to invest in and you can allocate your investment among different asset classes. A robo-advisor backed by strong research processes will help you select the right mutual fund schemes. Remember, fund performance should not be the only criteria. There needs to be different qualitative and quantitative parameters that need to be considered before arriving at the top schemes suitable for your portfolio. Robo-advisors that prudently pick the best schemes for your portfolio should rank high amongst those shortlisted.

- Established and reputed company

There is no dearth of robo-advisory platforms as the barrier to entry is low. While the competition is immense, you need to choose wisely, entrust your money to best advisor!

Don’t fall for the freebees offered such as gifts, lucky draws, attractive discounts or extended subscription plans. You need to opt for robo-advisors who are genuinely concerned about your long-term financial well-being. Care should be taken such that you do not entrust your money with fly-by-night operators. With the immense competition, smaller robo-advisory firms may find business unviable, could shut shop, and leave you in the lurch.

Opt for robo-advisors backed by established companies in the financial services space. Sound and ethical research processes fully support their investment recommendations. They should be fee-based to ensure that the commissions they earn do not influence their advice.

- Query resolution

The robo-advisor should be backed by a team of experienced customer service associates and financial planners. If you have any query related to the investments you make or if you are facing issues when transacting, your problem should be resolved quickly and professionally. After all, robo-advisors cannot operate all on their own. Human intervention may be needed at some point down the line.

- Costs

Costs play a crucial role when you are planning your investments. Different robo-advisors may charge you through one of the methods below:

- An advisory or subscription fee (monthly, quarterly or yearly)

- A transaction fee (each time you execute a transaction through them, they charge you a fee)

- A percentage of the amount invested. (Popular in the US)

- A percentage of the amount invested. (Popular in the US)

You can always decide whether the subscription fee or transaction fee is worth your money depending on the quality of advice and services offered. Also, if you have a high quantum of assets, you can avoid investing with robo-advisors that charge you a percentage of your investment value. The costs may end up higher than the one-time fees you would pay otherwise.

Step 5: Make a decision and stick with it

After the crucial evaluation process, now the time has come to pick the robo-advisor worthy to manage your investment. As you have followed a stringent 4-step process to narrow down the list, you may feel there’s little that can go wrong; however, selecting the right platform is just the first step to your financial independence.

Once you set out to achieve your financial goals, keep it on track. Many a times, individuals avail of the services of a financial planner or investment adviser, but are unable to stick with the plan through the entire investment horizon. This can adversely affect their financial well-being.

So remember, once you begin, make sure you stay on until the end. If there are genuine issues with the robo-advisor that warrants an exit, make sure you continue with another. This will ensure that your financial goals are not impacted.

Key Takeaway

Robo-advisors certainly may be a compelling alternative to many sources of traditional advice, and in many cases may be a step ahead of such sources of advice due to their lower costs, well-grounded investment methodology, and alignment with you financial interests.

At the same time, you need to acknowledge that not all robo-advisors are perfect. Their advice may not be fully customisable. Hence, the robo-advisory service you choose needs to be well equipped to care for your investments and financial goals.

|

Note: In less than 72 Hours, the doors to become a Founder Member of PersonalFN Direct, our brand new smart Robo Adviser, will close.

Act Now to Sign up at over 80% off and a FREE Year of access

PS: If you are reading this now, you are already late. The Founder Member offer closes sooner than it seems

CLICK HERE TO SIGN UP NOW!

|

Related topics you may find interesting to read

Mutual Fund Direct Plans - Everything You Need To Know

Mutual Fund Regular Plan Or Direct Plan: Which to choose?

How To Switch From Mutual Fund Regular Plans To Direct Plans

Why You Should Opt For Direct Plans While Investing In Mutual Funds

Here’s How Direct Plans Can Add Significant Wealth Over Time

Author: Jason Monteiro