Impact

Only a few days left in Akshaya Tritiya. As per the Hindu calendar, the third day of Vaishakh month holds tremendous significance. This is the day in a year when the Sun and the Moon are at the acme of their brightness.

A mythological legend suggests that Lord Shiva awarded Kubera with wealth on this very day. It is also believed the Sun God presented a divine bowl that prepared food endlessly (Akshay Patra) to the Pandavas’ wife, Panchali on the day of Akshaya Tritiya. Another legend says whatever positive activity you start on this day earns you name, fame, and success.

Buying gold on Akshaya Tritiya is one such custom most follow religiously. As in every culture, customs and traditions in India has some religious and mythological roots. This helps maintain social cohesion. Needless to say, they are important. However, basing your investment decisions blindly on them may yield unfavourable results sometimes. So the question is, should you buy gold this Akshaya Tritiya?

Well, PersonalFN believes, you should buy gold on every dip as long as your gold holdings compose 10%-15% of your portfolio. People often make a mistake of expecting superior returns from gold. The role of the yellow metal is to provide diversification to your portfolio and not accelerate gains.

Does gold look attractive at this juncture?

Since the beginning of 2016, the gold prices have increased nearly 22.0% in the international markets. Taking cues from the broader trend, the price of gold in India has jumped over 20.0% during the same period. After raising the interest rates by 25 bps, the Federal Reserve (Fed) has hinted at following dovish policies going forward. This coupled with the global lacklustre economic performance has been driving up gold prices. The Fed’s stance and China’s economic progress will determine the direction this precious metal prices will head in.

The Indian rupee and gold prices...

The movement of the Indian Rupee (INR) against US$ also plays a crucial role in deciding the fate of gold prices in India. As the Reserve Bank of India (RBI) remains committed to ironing out the excessive volatility in the currency markets, INR is expected to be relatively stable in foreseeable future. The Government has instilled confidence among global investors by charting a path to fiscal consolidation. As long as the flow of US$ continues to remain stable, INR is likely to perform well. In effect, international factors would heavily influence the gold price in India. The Government is keen on discouraging people from buying gold in the physical form. Hence, it remains to be seen how jewellers react to the Government policies.

India specific factors...

On top of 10% customs duty, the Government imposed 1.0% excise duty on gold—a move that attracted the wrath of the Jewellers from all parts of India. A 42-day long jewellers’ strike impacted India’s gold demand-supply dynamics. In pre-budget times, jewellers were hoping to see some relaxation in the import duty, which is why many of them postponed their buying. As a result, gold imports in India touched a 34-month low in February, as reported by Reuters on April 04, 2016. Imports slid further by 67.3%. However, now that the jewellers have called off the strike temporarily on the Government’s assurance of no harassment from the excise and customs departments, a revival of the demand for gold is expected. The occasion of Akshaya Tritiya may help jewellers clear up the existing stock.

PersonalFN is of the view that, considering the factors mentioned above, you should avoid buying gold in large quantities on Akshaya Tritiya. Having said this, buying jewellery for consumption may be a personal choice. From an investment perspective, you should piecemeal your investments.

At PersonalFN, we encourage readers / investors to buy gold in paper form. Sovereign Gold Bonds and Gold Exchange Traded Funds (ETFs) remain the two most attractive ways of investing in gold. So, will you be buying gold this Akshaya Tritiya? Share your views with us.

Impact

Stock experts often use adages to address their followers and other investors. One such is this—“Sell in May and go away”. Are you wondering about why they chose a month that starts with the International Labour Day, that might be bad for equity markets? As quoted by Investopedia, Dow Jones Industrial Average has generated lower than 1.0% returns during the months of May-October period every year, since 1950, while the investments made between November and April are significantly higher. Beyond statistical data for years, is there a fundamental reason for making such a statement? Well, there could be only this one—in summer vacations, trade volume generally drops, which in turn dismantles the stock prices. The opposite hold true for the November-April period.

Should you apply this principle to the Indian context and sell now?

Hold yourself back if you are tempted to do so. From 2001 to 2015, S&P BSE Sensex generated negative returns only on seven occasions. This means, there’s no evidence that May is a bad month for Indian markets. In fact, returns have mostly followed the law of probability, i.e. chances are evenly distributed for every unforeseen and uncontrolled outcome.

In May 2009, the UPA Government got its second mandate. Markets had rallied ferociously, generating over 28% returns. Most investors leaving the markets missed this rally. In May 2014, when the NDA Government came to power, the S&P BSE Sensex went up by over 8.0%. These instances are enough to prove that those who sell in May are giving more importance to catchy rhymes than market fundamentals.

How are we placed in May 2016?

Markets have generated negative returns in 2015. China’s worries got us closer to a situation where distress selling could have kicked in at any time. However, the markets have been holding steady since the Budget. Of course, there are concerns of the Government overshooting its fiscal deficit target. The Government has not only reaffirmed its commitment to fiscal prudence, but has also pumped in over Rs 2.21 lakh crore to give a serious facelift to India’s infrastructure. It has generously allocated money to schemes focusing on rural development. The Markets gave thumbs up to these efforts and rallied post budget. A prediction of a more-than-average monsoon was another positive for Indian equity markets.

Foreign Institutional Investors (FIIs) have turned net buyers post union budget. The global markets have also become supportive after the Federal Reserve hinted at a much gradual interest rate hikes, going forward. There haven’t been high expectations that the Goods and Services (GST) Bill will be passed in the on-going budget session. The market’s sentiments are not bullish on corporate results either. Despite this, they have held up majority of the gains made after the union budget.

In the absence of recent positive developments, the equity markets in India are likely to remain range bound, at least until we get more clarity on the southwest monsoon. A favorable monsoon may get markets excited and uplift economic growth.

PersonalFN believes investors should not try to time markets. May 2016 doesn’t look bad; selling now without paying attention to the quality of your holdings would be a big mistake. In fact, the first quarter of every Financial Year (FY) sets the tone for the full year. The monsoon that sets in by the first week of June and departs in the last week of September, is one of the biggest driving forces of the Indian markets. How can a serious investor stay out of the markets during these crucial months? You get various versions of investing quotes and adages.

How about this one:

“OCTOBER: This is one of the peculiarly dangerous months to speculate in stocks in. The other are July, January, September, April, November, May, March, June, December, August, and February”. –Mark Twain

Sounds more sensible, doesn’t it? We would love to hear your views.

Impact

Your investment in equity shares can reward you in two ways—price appreciation and dividends. Although this is true in theory, more often than not, investors buy stocks for capital appreciation. However, when the economic growth comes under pressure and corporate profits don’t rise quickly; shares don’t rise as rapidly as investors might expect.

Equity markets jumped significantly after NDA Government came to power; but after the initial phase of the sharp movement, the rally fizzled out due to sluggish corporate performance. In such times, companies have tried pacifying shareholders by paying them higher dividends.

The question is will higher dividends sustain if corporate Inc. doesn’t see any significant jump in revenues and profits in foreseeable future?

As reported by Business Standard on May 02, 2016, out of 144 listed companies that have reported their Q4 numbers so far are set to pay dividends of Rs 61,087 collective for the Financial Year (FY) ended March 31, 2016. This has been a jump of 19.2% over the amount they paid as a dividend in FY 2014-15. The said 144 companies will retain 57% of their profits and the remaining 43% will be distributed to shareholders as a dividend. Last year the retention was 62%. The net profit of the sample companies has increased at a compounded annualized rate of 8.0% over last five years. However, the growth in dividend has been over 26% during the same period.

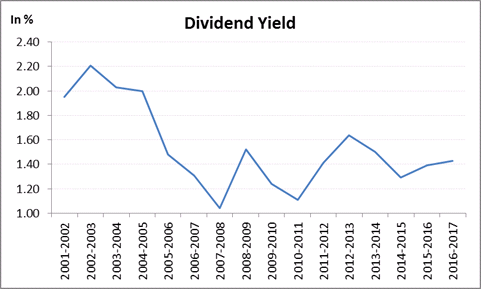

Will Higher Payouts Make Dividend Yields Less Attractive?

(Source: BSE, PersonalFN Research)

S&P BSE Sensex constituting companies have also demonstrated the similar trend of higher payouts. However, the difference in the net profit growth and dividend payout growth is lower. Sensex companies have recorded 13% growth in their dividend payout while their net profits have grown at 7.5% over last five years. A few companies are paying as high as 80% of their net profit for FY 2015-16 as dividends.

To ready more about this story and Personal FN’s views over it, please click here.

Impact

Running is known to be a good exercise, but over doing it may injure your knees. Similarly, adding spices to your diet can be beneficial, however eating spicy food a lot may cause harm to the digestive system. In day-to-day life, moderation is the key to almost everything we do. The Securities and Exchange Board of India (SEBI) seems to have forgotten this dogma.

In the zeal of protecting investors’ interest, the SEBI, perhaps, has been overregulating mutual funds. Their directive on the disclosure of fund managers’ salaries and others executives drawing over Rs 60 lakh a year hasn’t gone down well with Asset Management Companies (AMCs). The actions of fund houses are loud enough to conclude so.

Let’s look at the ways AMCs have chosen to comply with these new disclosure regulations...

A few mutual fund houses such as Quantum and Peerless appear to be inapprehensive about disclosing the pay packages of their key executives in public domain. Whereas a few fund houses such as HDFC Mutual Fund, ICICI Mutual Fund, and Reliance Mutual Fund have used unique tricks for restricting the flow of such sensitive information only to their investors. Going a step ahead, DSP BlackRock Mutual Fund has placed a barrier of a legal undertaking that may add as a deterrent to those seeking information on salaries of the top brass. As revealed by The Indian Express dated May 04, 2016, employee cost averages to 56% for top 5 mutual funds compared on their asset base. The Association of Mutual Funds in India (AMFI) tried convincing the regulator, but its efforts were in vain as the SEBI remained resolute on its previous stand.

To ready more about this story and Personal FN’s views over it, please click here.

|

|

© Quantum Information Services Pvt. Ltd. All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 101 Raheja Chambers, 213, Free Press Journal Marg, Nariman Point, Mumbai 400021. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667

|