| S&P BSE Sensex* |

Re/US $ |

Gold Rs/10g |

Crude ($/barrel) |

FD Rates (1-Yr) |

34,915.38 |-54.32

-0.16% |

66.67 |0.24

0.36% |

30,905.00 | -384.00

-1.23% |

73.62 |-1.12

-1.50% |

5.00% - 6.90% |

Weekly changes as on May 03, 2018,

BSE Sensex value as on May 04, 2018

Impact

The concept of a pension and its system remains a borrowed first-world one in India even today. Unfortunately, like most borrowed concepts, it still is a half-baked recipe.

A pension aims to provide a dignified life post-retirement to elderly people. It reduces the dependency of senior citizens on their children —their so-called only support of old age.

In the initial phase, only government employees were entitled to receive a pension. Later, various central governments in India tried their hand at running comprehensive pension programmes.

However, there weren’t any major breakthrough.

Why?

Because, like most political agendas, their pension proposals looked brilliant only on paper.

Today, Life Insurance Corporation of India (LIC) is the most active player in the ‘pension market’.

And yes, ‘pension’ is a market.

Read this piece patiently for the next few minutes and you will completely agree with this statement.

The current government launched the Pradhan Mantri Vaya Vandana Yojana (PMVVY) scheme to “provide social security during old age and to protect elderly persons aged 60 and above against a future fall in their interest income due to uncertain market conditions.”

The schemes promised to pay 8% returns p.a. for 10 years. The minimum subscription amount was fixed at Rs 1.5 lakh and the upper limit was Rs 7.5 lakh of the scheme. Click here to read the press release.

Recently, the government decided to double the ceiling of the maximum purchase price of the PMVVY.

Now you can invest upto Rs 15 lakh and earn a pension of upto Rs 10,000 per month.

Further, the government has extended the subscription period by two years. Now the scheme will be open for subscription until March 31, 2020.

While government believes it’s doing its best to set up a full-fledged pensioned society in India, critics feel the returns offered by the scheme are low and inadequate to take care of post-retirement expenses, given its proportionate relationship with inflation.

These are extreme positions.

On the one hand, we are making government accountable for containing fiscal deficit, and rightly so. But on the other side, why are we annoyed about the returns it’s offering?

Such double standards are obviously an impediment to the implementation of a decent pension system.

Similarly, on the one hand, the government claims to be concerned about senior citizens. Then, why is it acting as an opportunist trader?

The first pertinent question: What’s the logic behind having a pension scheme for a 10-year period?

So, if somebody purchases an annuity at 60; does the government assume demise at 70? If not, then ditching that person at age 70 years is worse than not offering any security at when they qualify as senior citizens.

And the timing of the extension of PMVVY is brilliant, just like its launch. Inflation is slowly inching up, and there is likely a strong case for interest rates offered by banks creeping up. Unless you don’t make pension tax-free or offer some additional incentives, how different is PMVVY compared to any other bank deposit?

In other words, the government is trying to protect its skin by luring investors to lock their money for long-term at low rates, at a time when interest rates may rise. It’s trying to limit its liability. Does it then really care about India’s senior citizens?

Ideally, it should make PMVVY a 30-year scheme. But for that, it will really need to have the chest of 56 inches.

LIC is responsible for managing the scheme and if it fails to generate 8% returns, the government will bridge the gap—that’s the nature of the scheme. If the government of India can stick its neck out and promise to pay 8% returns for next 30 years, it will indeed create a history. It would be good enough to silence all critics who are complaining about paltry yields.

Why has India performed miserably on pension reforms so far?

Some governments in India lacked the motivation and some lacked intelligence.

Are we going down on both these counts day by day?

In the present form, the PMVVY isn’t anything more than a scheme that any government would like to use to propagate its pro-people stance before elections.

Do you still think the pension is more about security and less about business?

Let’s face it.

‘Pension market’ is no less than a jungle. You have to care for yourself, no one else will.

That’s why you should start planning for your retirement when you’re young.

The corpus that you build for your retirement depends on two broad factors:

We have no control over the behavior of the financial markets, so let's leave that one aside.

Consider this:

Can you imagine what your retirement life would be like if all the choices you made were absolutely perfect? If you didn't make a single retirement planning mistake, if every time you invested, it was according to plan, in the right asset class, in the right instrument, in the right option, and at the right time? Wouldn't life be grand?

Retirement planning isn’t as difficult as it may look.

First, try to estimate the corpus you might require at retirement using PersonalFN’s retirement calculator.

Second, depending on years left for your retirement and your risk appetite create a personalised retirement plan. You should also take into account your existing kitty of retirement savings.

Want PersonalFN to help you accomplish your goal of blissful retirement?

Yes?

Do not hesitate to call us on 022-61361200.

You can also Schedule a Call with our investment consultant, or even drop a mail at info@personalfn.com or reply to fns@personalfn and we will be happy to help you.

PersonalFN is a SEBI registered investment advisor. We will handhold you on the path of wealth creation and living a blissful retired life.

Want To Generate Higher Returns In Volatile Markets? Design Your Portfolio Strategically

Impact

Volatility is constant in the stock markets.

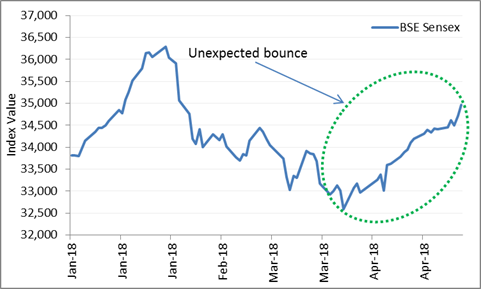

But 2018 seems to be a year of sharp swings.

Markets started the year with a bang! Investors showed tremendous faith in equity. On January 29, 2018, BSE Sensex hit an all-time high on the closing basis.

Investors had an expectation of favourable announcements in the Budget 2018—reshuffling of tax slabs, additional tax exemptions, and more sops for the industry.

But the Budget turned out to be a rural-centric one that took a tough stance against tax-non-compliance. It brought long-term gains made on equity shares under the purview of capital gains tax.

Sharp market swings

Data as on April 27, 2018?

(Source: BSE)

Investor sentiment changed quickly and the key indices frequently started touching lows. This story continued for two months—February and March. On March 23, 2018, BSE Sensex closed at 32,597—thereby falling 10% from the top it made in January.

Come April, Bulls took the Bears head-on and recovered majority of the ground they lost earlier.

This topsy-turvy market movement might continue indefinitely, but what are the chances that this will benefit you?

Creating an all-weather portfolio is challenging. So, you need to design your portfolio of equity-oriented mutual fund schemes in such a way that it makes the most of market volatility.

Have you heard of the ‘core and satellite’ strategy of investing?

What’s so unique about this?

Good question.

This strategy aims to get the best of both worlds, that is, short-term high-rewarding opportunities and long-term steady-return investing, and the good thing is, it works!

The term “core” applies to the more stable, long-term holdings of the portfolio; while the term “satellite” applies to the strategic portion that would help push up the overall returns of the portfolio, across market conditions.

To read more please click here.

Are Mutual Funds Losing Interest In ICICI Bank and Axis Bank?

Impact

ICICI Bank and Axis Bank have been embroiled in controversies during the past few months. Naturally, investors across the board are perturbed because the market value of these banks has significantly eroded. Both the stocks have declined by 19% and 16% respectively as on April 26, 2018, from February 1, 2018.

The shares of ICICI Bank fell amid reports about the alleged involvement of MD & CEO Ms Chanda Kochhar and her family members in a Rs 3,250 crore loan provided to Videocon Group on ‘quid pro quo’ basis.

The market regulator is considering a forensic examination on the financial statements and disclosures made by ICICI Bank in the last few years pertaining to this controversy over an alleged conflict of interest.

Axis Bank, on the other hand, came under scrutiny after the Reserve Bank of India asked the company's board to re-consider the decision to re-appoint Ms Shikha Sharma as its MD and CEO for a fourth term in the wake of concerns over rising bad loans at the country's third largest private sector lender. Later, Ms Sharma announced that she was cutting short her tenure by over two years.

To read more about this story and Personal FN’s views, please click here.

Accomplish Your Child’s Future Needs With Financial Planning

Impact

What are the common things most people want to give their children?

An education, a decent lifestyle, and the ‘great Indian’ wedding…

And you might not be an exception, but having high aspirations isn’t enough.

Nothing is possible without proper planning.

Here’s perspective — even God plans!

Do you think you can quit your job today, park all the money you have in a savings bank account, and still continue with your same lifestyle forever?

Perhaps, only then you don’t need to plan for your life goals.

This is the key — what are your life goals?

Once you’ve decided that, start planning ASAP (As Soon As Possible).

To read more and Personal FN's views, please click here.

FUND OF THE WEEK

HDFC Prudence Fund Now HDFC Balanced Advantage Fund – Time To Sell?

HDFC Mutual Fund manages two equity-oriented hybrid funds (better known as balanced funds) in the form of HDFC Balanced Fund and HDFC Prudence Fund. While they both branch out from the same category, each of them adopts a unique investment style.

However, the fund house faced a dilemma when SEBI dictated the different categories for mutual funds, allowing them only one scheme under each category.

HDFC Mutual Fund had to decide whether to merge the schemes or categorise them differently. Given that HDFC Balanced Fund has an AUM of Rs 20,000 crore and HDFC Prudence Fund a corpus of Rs 36,000 crore, a merger was ruled out. It chose the latter.

Click here to read the complete note!

And Other News...

With the aim of encouraging retail participation in the government securities market, the Bombay Stock Exchange (BSE) and National Stock Exchange (NSE) have planned to launch an online platform for retail investors. Through the non-competitive bidding route, retail investors can now bid for government securities.

Tutorials…

Your Guide To Insurance

Financial Terms. Simplified.

Forensic Accounting: Forensic accounting utilizes accounting, auditing and investigative skills to conduct an examination into a company's financial statements. Forensic accounting provides an accounting analysis suitable for court. Forensic accountants are trained to look beyond the numbers and deal with the business reality of a situation. They are frequently used in fraud cases.

(Source: Investopedia)

Quote: "To be an investor you must be a believer in a better tomorrow.”‒Benjamin Graham