Employees and taxpayers feeling the heat of tax-saving season could be facing a tentative 15 basis point rate cut on the Provident fund deposits. Employees' Provident Fund Organisation (EPFO) is considering reducing the interest rate to 8.5% from 8.65%, which will be discussed at the central board of trustees (CBT) meeting of the EPFO held on March 5, 2020.

A basis point is a hundredth of a per cent. Slashing rates is going to affect the millions of employees who have subscribed to contribute towards EPF scheme as they would earn lower returns on their mandatory retirement savings fund.

Reasons for the likely rate cut ...

EPFO usually invests 85% of its annual accruals in the debt market and 15% in equities through exchange traded funds (ETFs). At the end of March 2019, the EPFO had a cumulative investment of Rs 74,324 crore in equities, fetching a return of 14.74%.

Another noteworthy point is that EPFO had made investments of over more than Rs 18 lakh crore. Out of which, a significant amount, it held on to investments of debt laden toxic papers of the two biggest loan repayment defaulters---Dewan Housing Finance Corp. Ltd (DHFL) and Infrastructure Leasing & Financial Services (IL&FS), which are under scrutiny.

[Read: Are You Holding Debt Mutual Funds With Stressed Assets?]

Over the course of the year, reports of sluggish economic growth surfaced. In order to revive it growth, the RBI consecutively slashed rates in five of its monetary policy review meetings held in 2019; and in the last two meetings, the rates were kept unchanged.

Since then the earnings on long-term fixed deposits, bonds, and government securities have dipped by 50-80 basis points over the year, as was reported.

So it seems the EPFO body wouldn't be able to pay an 8.65% per annum, as reported by media "find it difficult to keep rates unchanged this fiscal," told by a source.

The EPFO was left with a surplus of Rs 151 crore in 2018-19 after an 8.65 per cent payout - much less than the surplus of Rs 586 crore in 2017-18.

Historically, the interest rate of a provident fund has been better compared to the bank FD rates

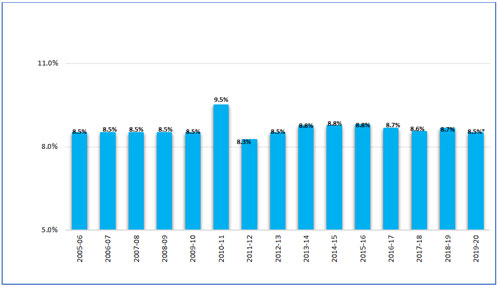

Graph: Almost stable Movement of EPF interest rate

*Expected rate.

*Expected rate.

(Source: EPFO, PersonalFN Research)

Unlike that on other Small Savings Schemes (SSS), the interest rate on EPF is reshuffled only once a year. In other words, it comes with a real lag when even the small savings schemes are under the pressure to reduce the rates, which have been kept unchanged. So, should the finance ministry give the go-ahead to the EPFO's recommendation, it would make more than 60 million subscribers unhappy.

EPF is created through the contributions made by an employee and employer. Under EPF scheme, both the employee and the employer have to make certain contributions every month towards the EPF scheme. You as an employee will get this money at the time of your retirement or if you discontinue working either temporarily or permanently due to any kind of disability.

These contributions are made every month, thereby encouraging employees to save a portion of their salary each month. Investments made by a vast number of employees across India are pooled together and invested by a trust.

The contributions made by the employee is eligible for tax deductions under Section 80C, the interest earned on the total investments and the withdrawal (including partial withdrawals for specific expenses) are exempt from the purview of taxation.

Is EPF the best retirement planning investment avenue?

Investments in EPF enjoy the EEE (Exempt-Exempt-Exempt) status from the taxation viewpoint. Meaning, the amount you invest in EPF helps you save tax, and the interest earned on EPF is also exempt from tax and proceeds too are tax-free at maturity or even otherwise. As a result, many salaried people consider EPF as one of the most dependable retirement savings avenues.

But it's time to realise that EPF is not the only alternative.

Relying solely on EPF for building your retirement savings corpus isn't a wise move. On the contrary, you should try to estimate the amount you might need to live a tension-free life post-retirement.

Have you ever calculated how much you would probably save for your retirement solely through EPF?

Use PersonalFN's EPF calculator.

It is a one-step solution to all your EPF related calculation questions. It quickly calculates the return on your EPF contribution within no time. EPF Calculator is an online tool and is accessible from anywhere at any time.

Remember for a blissful retirement as the coveted haven, planning is the gateway for it.

What's the right approach to retirement planning?

Consider a raft of things to do for your retirement investment plan

-

Set financial goals (short-term and long-term including retirement)

-

Consider your life expectancy

-

Determine the amount of money you will require to fulfil each goal

-

Ascertain the time horizon you have before the goals befall

-

Choose the perfect combination of investment avenues based on your risk profile, income, and the number of years you will work before you retire.

-

Start investing immediately and diligently

-

Periodically review your portfolio

[Read: Step-By-Step Approach To Retirement Planning]

Importance of asset allocation in retirement planning

In retirement planning, asset allocation is the most critical decision, not product selection. For those who haven't heard this phrase, asset allocation is nothing but the proportion in which you hold various assets such as equity, fixed income (debt), gold, and real estate in your portfolio.

Please remember risk and return go hand-in-hand.

[Read: Are You Paying Attention To Your Financial Fitness?]

If you invest in fixed income assets, you might be exposed to lower risk, but returns would be lower too. You might be running this risk if you depend entirely on EPF for building retirement savings.

Hence, depending on factors such as years left to retirement, your existing retirement corpus, retirement saving you need to accumulate, and risk appetite, you can invest in various asset classes such as equity, gold, and real estate, besides fixed income.

End note:

So, decide how you want your retirement to be and then focus your intentions of leading a blissful retired life. Be sensible and have an astute investment strategy that will help you create wealth and one that stands in good stead for your long-term financial well-being.

Editor's note: If you want your retirement to be blissful, don't miss out on mutual fund recommendations of PersonalFN's unbiased premium research service- Fundselect

On subscribing to PersonalFN's FundSelect service you get insightful and practical guidance on equity mutual funds and debt schemes - the ones to Buy, Hold, or Sell that will help you in your retirement planning as well.

Add Comments