Vishal works with a reputed company. His first salary was equal to his father’s last drawn salary.

Naturally, Vishal’s father is very proud of this fact and thankful to God for showering blessings on his family. However, he is just as tensed.

He believes he could retire peacefully because he had saved enough for himself and his wife. During his earning tenure, Public Provident Fund (PPF) fetched double digit returns.

He wonders if his son would retire as comfortably as he could.

Vishal likes to live life king size. He saves money regularly, but spends lavishly too on things he like.

According to Vishal’s father, if Vishal doesn’t take investments seriously, he might repent later in his life.

This isn’t just the story of Vishal. If you visit any middle-income family house in India, you would see similar cases.

Is retiring rich an illusion for millennials (and retiring poor a reality)?

Thankfully, successful retirement planning is a science. Here are some important points:

✔ Start early

✔ Estimate your post-retirement inflation-adjusted cash-flow requirements

✔ Consider your life-expectancy

✔ Take into account your risk appetite too before you invest

✔ Invest regularly and intelligently

✔ Review your portfolio periodically

And…you are done!

Those who aren’t serious about retirement planning, often feel their current income will suffice them in their post-retirement life. But they forget the impact of inflation.

[Read: Will The Retirement Fund Last Till My Last Breath? Know Here...]

Vishal’s father is worried about his son precisely for this reason.

Table 1: Inflation, the spoiler

| Current monthly household expenses |

Rs 40000 |

| Household expenses after 30 years assuming 5% inflation |

Rs 1,78,710 |

(For illustration purpose)

If your monthly household budget is Rs 40,000 at present, after 30 years you will need Rs 1,78,710 to maintain the same standard of living.

Hence, there’s an urgency to start early, which has multiple benefits. By starting as early as possible, you give yourself additional time to build a dependable retirement savings corpus.

Suppose Vishal remains ignorant about his retirement planning for five years. If he starts saving money later, that too after a friend who’s a regular investor insists that Vishal makes investments, he will be at a disadvantage.

You will be shocked to see the results…

Table 2: Postponing retirement planning can cost you dear

|

Vishal's friend |

Vishal |

| Monthly investments (in Rs) |

10,000 |

10,000 |

| Tenure in (Years) |

30 |

25 |

| Return assumption (compounded annualised) |

12% |

12% |

| Corpus at the end of tenure (In Rs) |

3.5 crore |

1.9 crore |

(For illustration purpose)

A delay of five years can cost Vishal Rs 1.6 crore. Do you know why Vishal’s friend would earn so much more than Vishal? Just because he started planning his retirement 60 months before Vishal did. This is the power of compounding.

[Read: What Is Power Of Compounding And The Wonders It Does In Wealth Creation]

Now many of you might feel 12% p.a return on retirement savings is too bold an assumption.

However, if you invest in equity mutual funds, and trust their performance track record for the last three decades, you would realise that 12% p.a isn’t an unrealistic assumption at all.

The power of compounding makes equity mutual funds the perfect investment avenue for retirement planning. Moreover, investing in direct plans offered by mutual funds can fetch you even higher returns.

For the last two-three decades, major equity indices such as the S&P BSE Sensex and CNX Nifty have generated 15%-17% compounded annualised returns. And given the shape of the Indian economy today, it won’t be unwise to assume that the equity asset class still remains an attractive proposition.

This is about markets in general. Well-managed active mutual funds often outperform their respective benchmark indices.

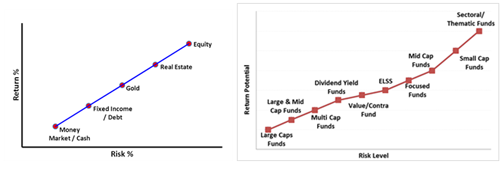

Before you invest in mutual funds through SIPs, you should check your risk appetite. Please remember, although equity mutual funds generate returns, they carry a certain level of risk too. Like in case of any other goal, when it comes to retirement planning, you should follow your personalised asset allocation plan which takes into account a number of factors including your risk appetite.

Consider risk factors before investing in equity mutual funds…

While it’s true that investing in mutual funds for the long-term is crucial for generating a sizable retirement corpus, it’s equally important to choose mutual fund schemes carefully.

Given there are a plethora of options available, it’s quite possible for you to invest in a wrong mutual fund scheme.

This brings us to the most interesting discussion.

How to select a winning mutual fund scheme for retirement

-

Primarily, the mutual fund scheme/s should be from a fund house/s that follows robust and well-established investment processes and systems. The idea behind this is to have funds that are process-driven and not the ones that work on the fund manager's whims and fancy. The experience of the mutual fund house's fund management team also plays a crucial role in the overall performance of a fund house.

-

Ideally, the fund house should not focus on launching too many schemes, but must have unique ones in its product basket. If the funds-to-fund manager ratio is high, i.e., if there are many schemes which a single fund manager handles, it could weigh on the performance of the schemes.

For example, if a fund house employs five fund managers and has floated 30 schemes; there will be a pressure on the fund management team. Against this, a fund house that offers only 12 schemes and still employs five fund managers will have a less pressing environment for its fund managers.

-

When you look at the past performance of a scheme, judge it across time frames and market cycles (i.e. bulls and bears). This will help you appraise the consistency of the scheme/s and include only the worthy ones in your portfolio. Moreover, do not merely look at returns; also recognise the risk the mutual fund scheme/s has exposed you to.

-

Besides, evaluate mutual fund schemes based on their portfolio characteristics; because ultimately it's the portfolio and how the fund manager handles it that will drive returns and draw risk. For example, a concentrated portfolio may eventually expose you to a greater risk as opposed to a well-diversified one.

Watch this video to know about mutual fund selection

End note:

You can retire rich only if you plan it well and choose right investment vehicles.

PS: PersonalFN offers you a great opportunity if you’re looking for “high investment gains at relatively moderate risk”. Based on the ‘core and satellite’ approach to investing, here’s PersonalFN’s premium report: The Strategic Funds Portfolio For 2025 (2019 Edition).

We will reveal to you a strategy followed by successful investors and the report will provide a ready-made strategic portfolio of top equity mutual funds schemes for 2025 that have the ability to generate lucrative returns over the long term. Subscribe now!

Add Comments