With robo-advisory platforms mushrooming over the internet, there’s no dearth of tech startups promising you sound advice on investments and on mutual funds in particular.

Many robo-advisory platforms may not even know how many mutual fund houses operate in India. Exaggerations aside, tech startups are toddlers in the arena of investing. They might not even have seen the sharp swings of the market ever.

But as they say, they are data-driven. They know as much about the history of markets as experienced investment gurus do, because they are take data-backed powered by technology. Tall claims!

If you think tech startups can give you sound financial advice just because they know technology better and can offer you conveniences, then you wouldn’t mind learning a dance form from a cricketer, isn’t it? Footwork is important in cricket, and a better dancer always has a pair of nimble feet.☺

And you should learn how to bat from an actor. Yeah, sometimes a batsman appears an innocent actor to deceive the umpire that he’s not out. ☺

If this sounds bunkum, what makes it so logical to approach a tech startup for advice on mutual funds?

Many tech startups rely solely on third-party recommendations or only number-crunch to recommend mutual fund schemes to potential investors. But be careful: they could be rendering an illogical advice logically.

Imagine this…

A scheme was consistently generating the highest returns in the category, and ‘data filters’ set by the tech startups rushed to announce it as the best scheme for your portfolio.

This is a data-driven decision, with some number crunching on an excel sheet. Great!

But, what about volatility it exposed you to?

Oops!

That wasn’t a parameter.

No problem! A robo-advisory platform realised its mistake and incorporated a few more filters that shortlisted schemes with lower volatility and higher returns.

This was meant to work better, but contrary to the expectations, many of the recommended schemes were on the downside within a few quarters of recommending them, owing to change in their fundamental attributes.

You see, some robo-investing platforms might have a founder with a personal finance background. But the critical question is, can he/she make the entire setup, a technologically-enhanced investment platform meaningful for your long-term financial wellbeing?

What’s more interesting is to see how a robo-advisory platform earns money for itself.

If it makes tall claims and tries to promote Regular Plans offered by mutual funds, or charges you no money and promises to offer you everything for free, you are most likely to make a bad decision opting for it.

Let’s now try to understand the difference between a mutual fund Direct Plan and a Regular Plan...

Regular Plan — This is the conventional kind of plan, where you invest/transact through your mutual fund distributor/agent/relationship manager. The recommendations are usually guided by the mutual fund distributor/investment advisor/relationship manager, backed by indirect commissions earned from the mutual fund house while there is after-sales support and service.

In regular plans due to the distribution cost involved, you incur a higher expenses ratio.

Direct Plan — Opting for the Direct Plan eliminates the services of a mutual fund distributor/agent/relationship manager. You choose to invest directly with the fund house selecting Direct Plans. You do your own research or bank on mutual fund research reports to invest. The transactions can be performed online, using a robo-advisory platform or even physically by visiting the registrar’s or the asset management company’s office.

And since, transactions are routed directly; no commissions are paid by the fund house on the money you invest. Hence, the expense ratio for a Direct Plan is lower compared to Regular Plan.

How do you, as a investor, benefit from a Direct Plan?

One of the advantages of a Direct Plan is you circumvent the rampant mis-selling that goes on to earn commissions.

You will agree that today the scenario is at odds. It’s rare to find a ‘financial guardian’ whom you can trust for sound advice on investing and wealth creation. There are only a few who render financial advice diligently and ethically.

Inflows under Direct Plans are witnessing a steady rise, only from cities such as Delhi, Mumbai, Chennai, Bangalore, Pune, and Chandigarh.

Over last few years, a majority of fund houses have managed to generate higher returns on assets of the same scheme coming through Direct Plans. This is because, besides the fact that market are in the uptrend, Direct Plans make a positive difference to your investments every year.

You earn approximately 0.5% - 1.0% additional returns every year by investing in Direct Plans, abetted by a lower expense ratio. This appears small to the eye at the outset; but over a span of a 15-20 year investment horizon, it reaps you a rich harvest.

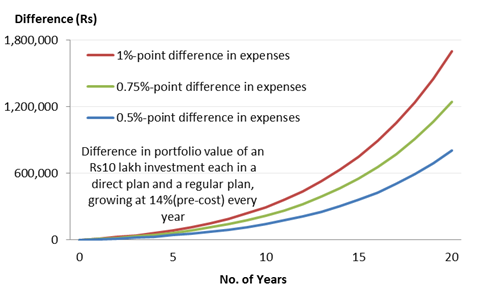

Direct Plan: Reaping The Long-Term Benefits

(Source: PersonalFN Research)

As can be seen in the chart above, on Rs 10 lakh investment, a small difference in costs can result in savings anywhere between Rs 8 -17 lakh over 20 years. Yes, you can earn an additional amount of as much as Rs 17 lakh, if the difference in costs is as much as 1% point.

The final portfolio value varies with the magnitude of difference in expenses. Every 0.25% point difference in the expense ratio works out to an additional earning of Rs 4.50 lakh in 20 years’ time, if Rs 10 lakh is invested.

The additional returns earned by investing in Direct Plan of a mutual fund scheme can enable you to fulfil the envisioned financial goals such as buying a dream home, a car, children’s education, their marriage expenses, and your own retirement among others.

Hence, sow the seeds of these small savings to reap a sweet fruit powered by the benefit of compounding.

Does a Regular Plan and a Direct Plan of mutual fund schemes have different portfolios?

No, the portfolio is the same for a Direct Plan and for a Regular Plan of a mutual fund scheme.

The mutual fund scheme constructs its portfolio as per a detail invest mandate cited in its offer document. The fund manager and his research team are expected to follow the investment mandate to meet the set out investment objectives.

Is Direct Plan suitable for naïve investors?

Yes, ideally everyone should opt for a Direct Plan.

Usually, the time-consuming and tedious task of selecting the best mutual fund schemes deters many individuals to opt for Direct Plans.

But with PersonalFN’s research-backed recommendations based on comprehensive mutual fund research methodology, you do not need to worry on that front.

PersonalFN’s flagship mutual fund research service, ‘FundSelect’ is celebrating 15 years of wealth creation. ‘FundSelect’ is time tested mutual fund service that has helped beat the market by a whopping 80%

It will provide Buy, Hold and Sell recommendations… intended at solidifying your mutual fund portfolio and make it free from any bias.

If you subscribe now you can avail this premium mutual fund research service for just Rs 2,950 and get 1 year additional access (worth rs 5,000)... virtually free!

Click here to know more and subscribe to ‘FundSelect’ today!

Do robo-advisory platforms offer Direct Plans?

Yes, some of them do.

PersonalFN is soon launching an ultimate robo-advisory platform and will provide only Direct Plans. And the recommendations will be backed by on PersonalFN’s comprehensive mutual fund research methodology which accounts for host of quantitative and qualitative parameters.

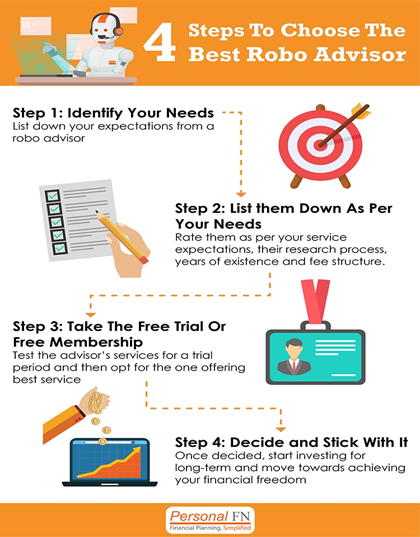

Here are four criteria that make a good robo-advisory platform:

-

Service

Some robo-platforms may offer you only transactional services, while others may provide you with a host of offline and online personal finance offerings.

But in addition, a good robo-advisory platform should also have advanced tracking and portfolio rebalancing services. Those that offer a mix of services should be worthy of your long-term financial commitment.

Also, the platform should be backed by a team of experienced customer service associates.

If you have any query related to the investments you make or if you are facing issues when transacting, it should be resolved quickly and professionally.

-

Unbiased and research-backed advice

A robo-advisory platform backed by astute and comprehensive research processes will help you select the right mutual fund schemes. It plays a vital role; the fund’s performance should not be the only criteria.

A Robo-advisory platform that prudently selects best schemes for your portfolio backed by comprehensive research process and risk profiling is the right one for you.

-

Established and reputed company

As mentioned before, there is no dearth of robo-advisory platforms as the barrier to entry is low. While the competition is immense, you need to choose wisely and entrust your money to the best robo-advisor.

In this milieu, small robo-advisory firms may find business unviable, could shut shop, and leave you in the lurch. Therefore, opt for a robo-advisor platform backed by established companies in the financial services space, who have been unbiased in their approach and serving investors diligently for decades.

They should be fee-based to ensure that the commissions do not influence their advice. And sound and ethical research-backed investment recommendations are imperative.

-

Costs

Costs play a crucial role when you are planning your investments. Different robo-advisory platforms may charge you through one of the methods below:

- An advisory or subscription fee (monthly, quarterly or yearly)

- A transaction fee (each time you execute a transaction through them, they charge you a fee)

- A percentage of the amount invested. (Popular in the US)

- Commissions earned from fund houses of recommended funds

While the first three forms are upfront one-time costs, watch out for the last option, as the advice here may be biased. You can always decide whether the subscription fee or transaction fee is worth your money depending on the quality of advice and services offered.

Also, if you have a high quantum of assets, you can avoid investing with robo-advisors that charge you a percentage of your investment value as fees. The costs could end up higher than the one-time fees you would pay otherwise.

In addition consider this:

Do not be penny-wise and pound foolish while you invest your hard-earned money via a robo-advisory platform.

PersonalFN is soon launching an ultra-reliable robo-advisory fee-based platform offering only Direct Plans, and will be backed by honest & unbiased research that outperformed the BSE-200 index in last 15 years by over 80%!

Add Comments