| S&P BSE Sensex* |

Re/US $ |

Gold Rs/10g |

Crude ($/barrel) |

FD Rates (1-Yr) |

34,924.87 |76.57

0.22% |

68.23 |-0.53

-0.78% |

31,164.00 | 334.00

1.08% |

78.79 |-0.81

-1.02% |

5.0% - 7.0% |

Weekly changes as on May 24, 2018

BSE Sensex value as on May 25, 2018

Impact

Operation Blue Ocean is underway.

If you thought it’s some maritime mission, you were completely off target.

HDFC Bank’s business strategy is to sell loan products digitally to the underserved market.

HDFC Bank has been disbursing Rs 1,000 crore worth of loans every month through its digital platform and has plans to grow this portfolio in the future.

Now, the Bank has decided to expand its LAS (Loan Against Securities) portfolio further.

It will soon offer you a loan against your mutual fund holdings.

Yes! You read it right.

HDFC Bank is trying to address your urgent cash requirements. Despite doing all the planning and maintaining a contingency reserve, you could fall short of cash.

What’s the product rationale?

Even if you liquidate your mutual fund investments, barring those in liquid funds, usually it takes 3 days to receive the proceeds. Therefore, you can pledge your mutual fund investments and get a loan in 3 minutes flat, which is treated at par with the overdraft facility received on a current account.

How much will you be able to borrow through this window?

If you are pledging equity-oriented mutual funds, you can choose any amount between Rs 1 lakh and 10 lakh in the permissible multiple.

In the case of debt funds, the amount can be as high as Rs 1 crore.

Depending on the nature of the pledged scheme—equity or debt—you can avail the overdraft facility of 50% and 80% respectively.

How much will this digital loan against mutual funds cost you?

Since you offer security, the interest rate charged on the loan is lower than that on a personal loan (unsecured).

Interest rate on LAS for January-March quarter

| Annual Percentage Rate (APR) |

Min |

Max |

Average |

| On equity-oriented mutual funds |

9.25% |

11.14% |

10.32% |

| On debt mutual funds |

7.95% |

10.62% |

9.71% |

(Source: HDFC Bank)

Note that the interest rate on loan against mutual fund units is linked to the MCLR (Marginal Cost of Funds Based Lending Rate). Thus, any rise in the MCLR will make this-overdraft-cum-loans expensive.

The good part is the Bank that will charge you interest only on the amount you actually utilise, and not on the amount you opted for.

Further, the Bank will charge you 0.5% towards the annual maintenance charges with an upper and lower cap of Rs 5,000 and Rs 1,000 respectively. The loan processing fee is Rs 500.

If you have investments in any of the following equity-oriented and/or debt schemes offered by these mutual funds, you may avail loan against your mutual fund units.

DSP BlackRock Mutual Fund

SBI Mutual Fund

ICICI Prudential Mutual Fund

Kotak Mahindra Mutual Fund

HSBC Mutual Fund

L&T Mutual Fund

Tata Mutual Fund

Mahindra Mutual Fund

HDFC Mutual Fund

IDFC Mutual Fund

Aditya Birla Sun Life Mutual Fund

Union Mutual Fund

PPFAS Mutual Fund

IIFL Mutual Fund

Shriram Mutual Fund

[Access mutual fund factsheets here]

Although the product has been launched officially, it could be some time before you can get an instant disbursal of the loan. The bank may (or may not) choose to partner with more fund houses to offer a credit facility to their investors.

And it appears that many other banks will follow suit, if a product idea gets a good response in the market.

A word of caution…

The purpose of the loan is important. You can’t borrow under this facility to make money out of speculative transactions including those related to the capital market activity. Likewise, the loan can’t be availed for any illicit purpose.

Should you opt for such loans?

Instead of breaking your mutual fund investments and discontinuing your SIPs (Systematic Investment Plans), loan against your mutual fund units could be considered. But, it depends on the purpose and urgency.

If you want to avail this facility to finance your new bike or buy an expensive watch, think twice — it is not a very prudent idea.

Loan against mutual fund units can considered only when you are in a dire need of funds and do not wish to liquidate your existing investments, built with your hard-earned money over the number of years.

[Read: How To Take A Loan Against Your Bank Fixed Deposit]

Ideally, you should have a contingency plan in place to meet your needs on a rainy day.

[Also read: A 3-Step Guide to Building A Liquid And Secure Emergency Fund]

Note excessive credit/loan, can harm your credit score. Hence, borrow prudently only within your means and make sure to repay sooner in the interest of long-term financial wellbeing.

Further, to accomplish your life goals, viz. buying a dream home, car, your children’s future needs (education and wedding expenses), your retirement, etc., have a well-drawn financial plan in place.

The real role of mutual funds isn’t to be pledged for a loan. Mutual funds, on the contrary can help you create wealth and help achieve the envisioned financial goals. Therefore, don’t pledge them unless it’s absolutely essential. Now, to be successful with your investment in mutual funds, you need to choose them carefully.

Many of you might not have the time, expertise, or both to select mutual fund schemes on your own. If you are one of them, don’t lose heart because PersonalFN’s unbiased mutual fund research service—FundSelect is just meant for people like you.

Every month, PersonalFN’s FundSelect service will provide you with insightful and practical guidance on equity funds and debt schemes – the ones to buy, hold, or sell. Thus assisting you in creating the ultimate portfolio that has the potential to beat the market.

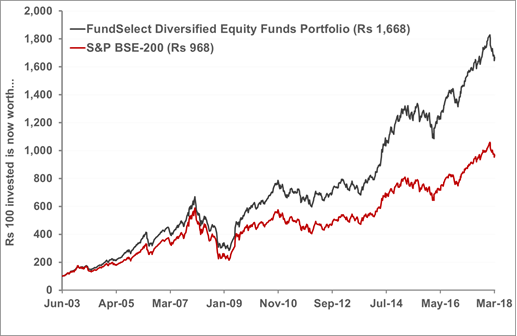

Out of every four funds recommended in the FundSelect, three have always outperformed BSE 200 index. That's the success rate of PersonalFN.

PersonalFN's Mutual Fund Research service 'FundSelect' Vs. S&P BSE 200

Data as on March 28, 2018

(Source: ACE MF, PersonalFN Research)

FundSelect is turning FIFTEEN.

On this auspicious 15th anniversary of FundSelect, we intend to make it “ultra-special” for you.

How?

Well, how about getting 1-Year of access to FundSelect virtually Free?

And there’s MORE...

Get FREE access to our premium report, 'Top-5 Funds For 2020

So, hurry and subscribe to PersonalFN's FundSelect NOW!

Sell-In-May-And-Go-Away: How Sound Is This Advice For Mutual Fund Investors?

Impact

Disciplined players follow the rules of the game.

That's so true about the experienced Wall Street traders.

Some of them follow this strategy: sell-in-May-and-go-away (and buy again in November)

They believe this strategy is highly profitable as it helps avoid the seasonal weakness in the U.S. economy. Apparently, there's some historical evidence to support this argument.

According to Investopedia, average returns generated by Down Jones Industrial Average for May-October period between 1950 and 2013 have been just 0.3%. In contrast, those for the November-April period have been 7.5%.

To read more please click here.

How To Take A Loan Against Your Bank Fixed Deposit

Impact

A bank Fixed Deposit (FD) as we all know is a secured way to generate wealth, particularly for conservative investors. It takes care of your liquidity needs, addresses short-term goals, and can even help you in tax planning (a 5-year Tax Saver bank FD).

[Read: Everything You Need To Know About Tax Planning]

But along with these attributes, a bank FD also stands as the last resort on a rainy day, when you are in dire need of funds. Yes, it helps in contingency planning!

Broadly, you have two options during an exigency: liquidate your bank FD, or take loan. If you choose the former, it can disrupt the path to wealth creation.

To read more please click here.

Do You Fear The Decline In Mid Cap Funds? Don't, If You Invest The Right Way!

Impact

Not too long ago, Mid- and Small Cap mutual funds were sitting on returns in excess of 40% over a 1-year period. Some schemes generated returns in excess of 50% in the 1-year periods ending in January 2018, a month when the market peaked to its all-time highs. It is natural to be lured by these supernormal returns.

To read more please click here.

The Good, Bad, And Ugly Of Inflation

Impact

Black magic!

It’s a symbol of evil.

Long black hair!

It’s the top-selling slogan of the whole hair cleansing industry.

So whether the word black is used to denote ‘fair’ or ‘unfair’?

Well, depends on the context.

The same is true

about inflation.

To read more please click here.

FUND OF THE WEEK

HDFC Balanced Fund Merged To Form HDFC Hybrid Equity – What Will Change?

HDFC Mutual Fund currently has two equity-oriented hybrid funds (earlier known as balanced funds) in its kitty. These are HDFC Balanced Fund and HDFC Prudence Fund. Despite belonging to the same category, each adopts a unique investment style.

However, to comply with SEBI's diktat on mutual fund categorisation, HDFC MF needed to categorise them differently. Merging the schemes would have been an imprudent strategy, given that HDFC Balanced Fund has an AUM of Rs 21,000 crore and HDFC Prudence Fund a corpus of Rs 38,000 crore.

HDFC MF proposes to categorise HDFC Balanced Fund under this category, after merging it with HDFC Premier Multi-Cap Fund. The new scheme will be known as HDFC Hybrid Equity Fund. The effective date for these changes is June 1, 2018

To read more please click here.

And Other News...

If you are planning to invest in the six schemes of Axis Mutual Fund, given below and opt for Systematic Withdrawal Plan (SWP), you may consider their newly introduced automatic encashment facility. Under the facility, investors can redeem a fixed percentage of net asset value of units on a monthly basis. Refer the addendum for details.

The minimum value of redemption shouldn't be less than Rs 500.

You might opt for the encashment of 0.7% of the net asset value of your investment in the following schemes:

And it can opt for the encashment of 0.5% of the net asset value of your investment if you hold the following schemes:

Tutorials…

Step-By-Step Approach To Retirement Planning

Financial Terms. Simplified.

Annual Percentage Rate (APR): An annual percentage rate (APR) is the annual rate charged for borrowing or earned through an investment, and is expressed as a percentage that represents the actual yearly cost of funds over the term of a loan. This includes any fees or additional costs associated with the transaction but does not take compounding into account. As loans or credit agreements can vary in terms of interest-rate structure, transaction fees, late penalties and other factors, a standardized computation such as the APR provides borrowers with a bottom-line number they can easily compare to rates charged by other lenders.

(Source: Investopedia)

Quote: "The investor's chief problem - and even his worst enemy - is likely to be himself.”‒Benjamin Graham