Impact

Keeping no surprise element in the policy review, RBI held repo rate unchanged in its 1st bi-monthly monetary policy for the Financial Year (FY) 2015-16. The Government has also preferred to maintain status quo on Cash Reserve Ratio (CRR) as well. On back of unseasonal rain damaging Rabi crop and fruits and vegetables, the upside threat to food inflation has increased. Taking a note of that, RBI took a precautionary step of taking a pause in its endevour of making monetary policy accommodative. Moreover, despite of poor credit growth, banks have not opted to pass on the benefits of previous rate cuts to borrowers so far. RBI also considered this as a reason for not lowering the policy rates this time.

After the recent policy review; key rates stand as given below;

- Repo Rate (i.e. policy rate) 7.50%

- Reverse Repo rate 6.50%

- Cash Reserve Ratio (CRR) 4.00%

- Bank Rate 8.50%

Background to policy action

RBI had reduced policy rate by 0.25% ( outside policy review) on March 05, 2015 in response to declining inflation and valuable structural changes initiated by the Government in the budget that are expected to help curbing inflation going forward.

Since 6th bi-monthly monetary policy statement released in February 2015, global recovery turned out to be moderate and uneven largely due to unprecedented fluctuations in currencies and commodity prices. The speculation of Federal Reserve (Fed) hiking interest rates in the U.S. sooner than expected, had made markets anxious. Such speculations waned subsequently, boosting the global markets. The sentiment of investors globally, largely affects India’s currency as well. Currency and commodity fluctuations impact inflation and inflation expectation in India.

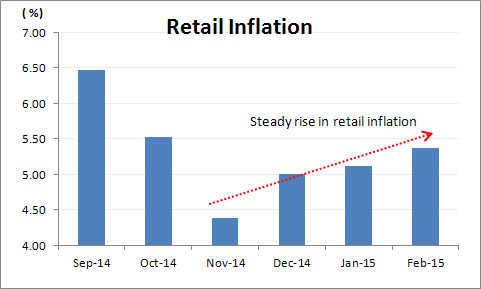

Back home, as per RBI assessment, the industrial sector, and in particular, manufacturing appears to be regaining momentum, with the growth of production in positive territory for three consecutive months till January. Mainly led by falling international crude oil prices; inflation moderated until recently. However, steady rise in food price inflation has been pushing the retail inflation up since November 2014. However, at 5.37% in February 2015, it still remains well below the upper limit of 6.0% set by RBI to be achieved by January 2016. RBI appears to be confident of achieving its target of keeping retail inflation below 6%.

Is fall in Inflation over?

Note: The data points above are from the Consumer Price Index

(Source: MOSPI, PersonalFN Research)

Although policy stance of RBI still remains accommodative; it has taken a pause considering some risks to its projections of inflation expectations. As stated by RBI, “there are upside risks to the central projection emanating from possible intensification of El Nino conditions leading to a less than normal monsoon; large deviations in vegetable and fruit prices from their regular seasonal patterns, given unseasonal rains; larger than anticipated administered price revisions; faster closing of the output gap; geo-political developments leading to hardening of global commodity prices; and spillover from external developments through exchange rate and asset price channels." The central bank also believes business confidence and the consumer confidence have been increasing; which enhances the possibility of achieving higher growth.

What status quo means to you?

Monetary policy may not have any impact on you unless it is transmitted through various channels. RBI has nudged bankers to lower base rates now. In response major banks such as SBI, HDFC Bank, ICICI Bank to name a few, have lowered their base rates. Base rate is a reference point to loan pricing. Therefore, when the base rate is lowered, borrowing becomes cheaper. Now it remains to be seen if other banks follow industry leaders and slash their base rates. When this happens, borrowers stand to gain despite of no rate cut accorded in 1st bi-monthly policy for FY 2015-16.

Those of you who have borrowed at floating interest rate may benefit. Lower borrowing cost may also push the corporate profitability upwards as companies have to shell out less on interest cost.

How capital markets reacted?

Both, equity and bond markets remained volatile on the day of policy announcement. Immediate reaction of the equity market to the policy action was negative; as market indices dipped a bit. However, towards the closing of the session; markets not only did recover but also posted some mild gains. On the other hand, bond yields went up slightly. Yield on 10-Year benchmark sovereign bond went up nearly 7bps (0.07%). Having said this there wasn’t any panic among investors.

What to expect?

As stated by RBI, “going forward, the accommodative stance of monetary policy will be maintained, but monetary policy actions will be conditioned by incoming data. First, the Reserve Bank will await the transmission by banks of its front-loaded rate reductions in January and February into their lending rates. Second, developments in sectoral prices, especially those of food, will be monitored, as will the effects of recent weather disturbances and the likely strength of the monsoon, as the Reserve Bank stays vigilant to any threats to the disinflation that is underway. The Reserve Bank will look through both seasonal as well as base effects. Third, the Reserve Bank will look to a continuation and even acceleration of policy efforts to unclog the supply response so as to make available key inputs such as power and land. Further progress on repurposing of public spending from poorly targeted subsidies towards public investment and on reducing the pipeline of stalled investment will also be helpful in containing supply constraints and creating room for monetary accommodation. Finally, the Reserve Bank will watch for signs of normalisation of the US monetary policy, though it anticipates India is better buffered against likely volatility than in the past."

PersonalFN is of the view that, investors may closely track the movement of retail inflation, going forward. As and when inflation would inch up above 6.0% mark, there will be a negative reaction from the investors and bond prices may take a hit. Furthermore, equity markets, although be affected to a lesser extent, may take a dip if inflation inches up as it would increase the likely chances of RBI holding rates unchanged for longer than expected.

PersonalFN suggests you not to speculate on any economic variable and endanger your money. On the contrary, you should meticulously follow your personal asset allocation that is designed to take care of your financial goals. PersonalFN provides unbiased financial planning and mutual fund research services, giving a solid platform to investors.

Add Comments