(Image source: Image by paulracko from Pixabay)

(Image source: Image by paulracko from Pixabay)

Lakhs of investors received a rude shock just as the festival season was about to kick-start. The RBI has imposed restrictions on Punjab and Maharashtra Co-operative Bank and depositors of the bank will not be permitted to withdraw more than Rs 10,000 over the next six months.

PMC, one of the leading co-operative banks in India, is under the scanner for the under-reporting of bad loans.

The cap on withdrawals has caused panic among the customers. Many of them who had parked their hard-earned money in the bank are worried about the fate of their savings. While others are anxious about not being able to meet the daily expenses and other urgent needs given the low amount that can be withdrawn.

To be clear, the directions by the RBI should not be construed as cancellation of banking licence. In the past, the banking regulator had imposed restrictions on other co-operative banks such as Kapol Co-operative Bank, Vasantdada Nagari Sahakari Bank, and Karad Janata Sahakari Bank, among others.

Some of these banks were taken over by other established banks and the depositors were paid off, while in other cases the restrictions were extended. Customers of PMC Bank can expect a similar outcome for the bank.

The curb on PMC Bank has yet again raised a question on the safety of the depositor's money in co-operative banks.

[Read: Factors To Look At While Investing In Bank FDs]

One of the main factors that attract people to deposit in co-operative banks is the higher interest rate they offer. These banks typically cater to small depositors and businesses and are important institutions for increasing financial inclusion in the highly under-banked Indian economy.

But undue political interference in such banks has raised issues of governance and professionalism. Further their small scale of business makes them vulnerable to concentrated lending.

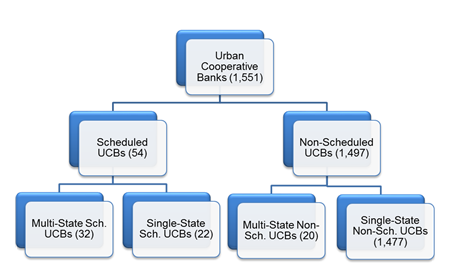

As on March 31, 2018, there were 1551 urban co-operative banks in India of which 1,497 are non-scheduled, i.e. they are not governed by the RBI.

Chart: Structure of Urban Cooperative Banks in India

(Source: RBI)

Since non-scheduled banks are not governed by RBI, it would not be safe to park your money there. In case of scheduled cooperative banks, even as there have been issues plaguing them, it would not be right to say that you must completely avoid parking your savings in them.

The rules that apply to scheduled commercial banks such as private banks and public sector banks apply to scheduled cooperative banks as well. Besides, RBI has time and again taken steps to improve governance in co-operative banks.

One way to shortlist a good co-operative bank to park your money in will be to look at their financial position. NPA growth, capital adequacy ratio, and return on assets are some of the parameters that can be considered to measure the performance of such banks.

[Read: Read This If You Hold Deposits With Public Sector Banks]

It may not be an easy task to compare cooperative banks on these parameters. Therefore, you would be better off if you limit your exposure to such banks.

The fact that cooperative banks offer higher returns for deposit is a clear indicator of higher risk involved. For better safety of deposit and good governance policies, you should consider scheduled commercial banks to deposit your hard-earned money.

In case of an extreme action by RBI such as liquidation of a bank, the Deposit Insurance and Credit Guarantee Corporation of India (DICGC) insures deposits up to Rs 1 lakh (principal + interest) across accounts of an account holder of a bank. In such a case, if you have deposits over Rs 1 lakh, the recovery may not be possible.

Hence, you must plan your deposits accordingly and diversify your deposits across different banks instead of parking all your savings in one bank.

[Read: 6 Safe Avenues To Park Your Monthly Savings]

If you are an account holder in PMC bank, debits for auto payments such as equated monthly instalments, systematic investment plan, etc. will not clear due to the restrictions imposed on amount. To avoid defaulting on loan and to continue with your investment, you can link another bank account for this purpose.

Only time will tell what will be the outcome of restrictions on PMC Bank. But as an investor one should always exercise caution and make prudent investment choice. Make sure to diversify your investment across asset classes to minimise the risk and optimise returns. Invest in schemes that provide transparency and safeguard investor's interest.

Add Comments