What does the abbreviation PSB stand for?

In normal circumstances, it means Public Sector Banks—‘nationalised banks’ is a synonym. But in the present scenario, it wouldn’t be inappropriate to deviate from the terminology and label them ‘Perennially Stressed Banks.’

The shareholders of PSBs have already lost a great deal of their capital. The current state of affairs at many PSBs even depositors fearing the loss of their hard earned money someday.

What’s the cause of their fear?

PSBs—down but not out…

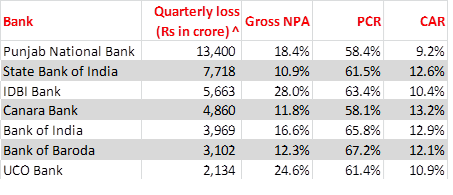

^ For the quarter ended on March 31, 2018

(Source: Bank press releases, Bloombergquint)

PSBs are incurring mind-boggling losses and their Gross Non-performing Assets (GNPAs) are severely high in proportion to the money they have lent. The Capital Adequacy Ratio (CAR) which denotes the risk absorption capacity of a bank is also low with almost every PSB, barring a few exceptions.

While it’s natural to be mortified of loss, it’s unwarranted to give in to the fear mongering. Believe it or not, fear mongering is a business. Fact is, bad news sells faster that good news and sells more.

The business of fear mongering is founded on these premises:

Unless you create a panic in the minds of readers, how would you create a market for your products?

Unless you propagate the fear of losing an opportunity, how would people buy more?

While the mainstream media, financial experts, and politicians make a noise on the deteriorating state of PSBs, they tend to go overboard. Now, it’s up to you. Do you want to take a 360-degree view or just the pilot’s perspective?

[Read: Are Banking Sector Mutual Funds Worth Risking Your Money?]

Please note:

But how safe are your fixed deposits with PSBs?

(Image source: thebluediamondgallery.com)

Think technically, and there will always be if and buts. Think practically, and you get clarity.

Let’s come straight to the point of safety.

No political party—irrespective of who comes to power in 2019—will stake its reputation and endanger its existence by messing up with depositors’ money. Since the single-largest promoter of PSBs is the government of India, no government at the helm can run away from its responsibility to its debtors— i.e. depositors.

And many of you must be keen to read about the loses PSBs have been suffering.

The losses you saw above are mainly due to increasing provisions. The Provision Coverage Ratio (PCR) is a measure of how adequately the bank is covered against the potential loss.

Higher the PCR, better the condition of a bank. It denotes that the bank will have to set aside a lesser amount to cover the loss in the future, if the NPAs are not likely to rise.

PCR = Cumulative provisions / Gross NPAs

If you fill in figures in the formula above, you would realise that, when you increase provisions and your GNPAs stay unchanged, you will be in a much better position.

For banks, the ideal condition is the falling denominator and rising numerator.

For instance, IDBI bank has a high GNPA of 28.0%, but its PCR has improved to 63.4% as on March 31, 2018, from 55.0% a year ago. In other words, if the flow of bad loans stops and the bank maintains the pace of provisions, it can emerge stronger.

Are PSBs doing enough for it?

-

Well, only time can tell if what they are doing is enough. They are trying to come out of the mess for sure. Continuing the example of IDBI Bank, it seems the bank has decided to stay clear of corporate lending—the root cause of NPAs.

-

The government announced a bank recapitalisation plan last year, which is in the implementation stage. If it can change the corporate culture at PSBs and make them more accountable for their actions, and more importantly, ensure no political interference in their functioning, PSBs might regain their lost stature.

-

Naysayers will always raise doubts, but the fact is Insolvency and Bankruptcy Code (IBC) is making its presence felt now. While it’s premature to comment about its success, the beginning has been excellent.

-

Successful acquisition of the bankrupt company—Bhushan Steel—by Tata Steel has helped banks par their NPAs by 35,000 crore at a consolidated level. It is the first major breakthrough. A similar outcome seems possible in other cases.

-

The RBI has tightened the reporting norms for banks, making them more transparent and accountable in the future.

Other alternatives, to improve the governance of PSBs such as privatisation, appear distant possibilities for now. Bank mergers and capital infusion by equity dilution are possibilities in the case of many public sector banks, but it is too ambiguous right now.

What should you do?

(Image source: pixabay.com)

If you are a depositor, you should be watchful of banks’ affairs but you should avoid being a victim of fear psychosis.

Speaking about the banking scam, they are undoubtedly of unprecedented magnitude, but as they are getting exposed, and cases pending with National Company Law Tribunal (NCLT) are being finally disposed of with concrete solutions, the chances of fiascos in future appear dim.

Many of you might ask: If the future looks promising, why not become shareholders in some PSBs?

That’s a tough call, since there are so many variables involved. Things may not go from bad to worse for depositors, but that doesn’t mean they will improve for shareholders. One needs to look at the individual case before taking a call.

Alternatively, you might consider leaving the job of stock-picking to professional fund managers and investing in diversified equity mutual fund schemes.

Here's one of the best way to select winning mutual funds for your investment portfolio. Please check out this offer:

To invest in winning equity-oriented mutual funds, Systematic Investment Plan (SIP) is the best strategy, whereby you can accomplish your long-term financial goals.

Add Comments