| S&P BSE Sensex* |

Re/US $ |

Gold Rs/10g |

Crude ($/barrel) |

FD Rates (1-Yr) |

34,142.15 |131.39

0.39% |

65.10 |-1.19

-1.86% |

30,405.00 | -170.00

-0.56% |

65.40 |1.07

1.66% |

5.00% - 6.75% |

Weekly changes as onFebruary 22, 2018

BSE Sensex value as on February 23, 2018

Impact

Wondering where the Indian markets are headed in these stormy conditions?

This article will shed some light and recap what’s been happening in the recent times.

Volatility in the global markets, the government’s decision to tax Long Term Capital Gains (LTCGs) on equity, and overheating of Indian markets despite the highly expensive valuations had hit the investors’ sentiment badly.

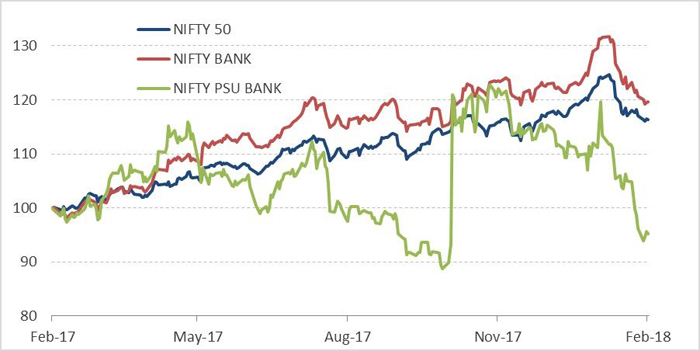

The shocking PNB scam negatively affected the stock market and it lost more than 33% in February alone. Within a 5-month time horizon, it has dropped down nearly 50%. The country’s second largest PSB reporting a fraud of this scale was detrimental to other banks as well with the possibility of direct exposure to this fraud. The fear of the ‘domino effect’ rocked the boat of other PSBs.

Soon after the government announced a comprehensive recapitalisation plan for the PSBs, investors had a suspiration of relief. In October last year, the government announced a revival package of Rs 2.11 lakh crore, to deal decisively with the problem of mounting Non-Performing Assets (NPAs) of PSBs.

Until then, the PSB stocks were under pressure, as not many had expected the government to announce such a massive rescue-package. Consequently, the market was jubilant with this news and PSB stocks rallied sharply.

Losing streak continues for PSBs

Data as on February 23, 2018

(Source: ACE MF, PersonalFN Research)

Those who had made investment decisions based on the announcement of government’s recapitalisation plan have burned their fingers with PNB and other PSBs .

The hard truth about the PNB fraud is that it has not only pushed back PSBs by five months, but has sent a dangerous message to investors —— government run banks can only squander taxpayer’s money and unabashedly get away with it.

If the consensus starts building up on this, investors may downgrade these institutions further.

For them and for all of you, PersonalFN has only one message — Diversify, diversify, and diversify!

This is the mantra many of you may have often heard when it comes to investing. Though it has merits to offer, many investors often incorrectly or incompletely follow it.

Diversification is one of the basic tenets of investment planning, and therefore vouched by many investment advisors. It helps one in reducing the risk in one’s portfolio, and thus builds it resilience.

Between January 1, 2015 and March 31, 2017, as many as 5,200 officials of public sector banks have been penalised for fraud, as per an article published by Times of India, citing data from the Reserve Bank of India.

As many as 1,538 officials of the State Bank of India faced legal action for fraud, putting the bank on top of the chart. Indian Overseas Bank and Central Bank of India occupy the second and third place with 449 and 406 unscrupulous insiders, respectively. At PNB, 184 officials were caught for fraudulent activities during the same period, the data revealed.

Separate data accessed from the RBI records for the period between April 1, 2013 and December 31, 2016 shows that all commercial banks, including private ones, lost Rs 66,066 crore to 17,504 frauds.

Following the PNB episode, PersonalFN received many queries from the anxious and disheartened investors who were worried about their investments in PSBs and also in mutual funds having exposure to PSBs. Investors were equally worried about putting money in fixed deposits of PSBs——especially those of PNB.

Among the schemes with maximum stake in PNB are HDFC Prudence Fund, HDFC Equity Fund, HDFC Mid-Cap Opportunities Fund, Reliance Tax Saver (ELSS) Fund, and HDFC Top 200 Fund. As on January 31, 2018, the market value of their holdings totalled Rs 728 crore, Rs 409 crore, Rs 334 crore, Rs 262 crore, and Rs 182 crore, respectively.

Several equity funds have a significant exposure to the State Bank of India. The stock would have created a drag on the returns of these schemes. Similarly, mutual funds with exposure to other PSB stocks would have suffered a similar fate.

Given the shoddy state of Public Sector Banks (PSBs), mutual fund houses are demonstrating their professional approach and astute wisdom. The exposure of PSBs is at a sub-2% level. This is because PSBs significantly contribute to the overall stress in the banking system. After all, they are the prime corporate lenders.

On the flip side, a majority of private sector banks lend to retail borrowers, a relatively less risky customers for banks, compared to the corporate borrowers.

Thus barring a few schemes, most equity-diversified funds will have low exposure to PSBs. Since professional money managers oversee your investments, mutual funds are a worthy investment avenue. Diversified equity mutual funds not only spread investments across sectors to curtail risk, but also enable you to achieve superior returns.

Investing in mutual funds may help you achieve your financial goals.

However, investing in the right mutual funds is key. You should invest in mutual funds having a proven performance record. A period review of your mutual fund portfolio helps you get rid of laggards. Moreover, it ensures that your investments are aligned with your personalised asset allocation.

|

Editor’s note:

If you are worried about the unpredictability of the equity markets and confused about which mutual funds to invest in this year, we have just the remedy for you.

PersonalFN’s latest exclusive report: Top 5 Equity Funds To Invest In 2018 has been created keeping the current investment scenario in mind. This exclusive report is already gaining popularity among our readers. So do not miss it.

Subscribe now!

|

MustRead

Best Midcap Funds For 2018. Look Before You Leap!

How To Pick The Best Mutual Funds For SIPs in 2018

Even if you pick the best performing mutual fund, it may NOT always be the best mutual fund when invested though a Systematic Investment Plan (SIP).

Strange, isn’t it? But it’s a fact.

On analysing the performance data of equity diversified schemes, it has been found that the performance ranking differs when comparing the point-to-point performance and returns generated via a SIP in the fund.

See for yourself in the table below:

Best Mutual Funds For SIPs in 2018? Think Again…

P2P - Point to point; SIP - 1st of every month, February 1, 2013 to January 1, 2018. Valuation date: February 1, 2018

(Source: ACE MF, PersonalFN Research)

PersonalFN considers the performance of equity diversified mutual fund schemes over a five-year period for this study. Of these, the top 25 schemes in terms of point-to-point (P2P) performance are considered.

We then compared the P2P performance to the annualised returns (XIRR) generated via a SIP. The P2P returns and SIP returns are ranked and then compared.

On studying this data closely, it is seen that though Aditya Birla SL India Opportunities Fundranked 18th in terms of point-to-point returns, it fell to the 39th rank when comparing the SIP performance.

Similarly, UTI Mid Cap Fund ranked in 13th place when considering single period returns. A SIP in the same fund over generated a return that ranked the fund 25th on the list.

Schemes that have delivered inferior performances on a point-to-point basis may do well if invested in systematically. HDFC Small Cap Fund took 28th place for its point-to-point performance. However, the returns generated via a SIP would have ranked the fund in the 15th place.

Kotak Emerging Equity Scheme too, ranked on the 35th position for its returns over five years. A SIP over the same period in the scheme would have ranked it in the 23rd place.

To read more about this story and Personal FN’s views over it, please click here.

4 Things To Do When You Are Not Able To Pay EMI

“I am unable to pay my monthly EMI and I need help”.

We received a mail from Akash (name changed to protect privacy) with this written on the subject line.

We further contacted him and understood his situation. Here it is for you…

Akash, works with an IT conglomerate as a consultant and his career spans a decade. Two years ago, when he had accumulated enough savings for down payment he decided to fulfil his dream of buying house with the help of home loan. Today he lives there with his parents and wife.

Due to down turn in the IT sector, many companies were laying-off engineers over the last few months. And Akash lost his job 9 months ago. Along with the trauma of loss of job what Akash is worried about meeting the debt obligation.

Akash’s experience of dealing with debt had been very short in the past. 3 years he had serviced the personal loan for wedding on timely basis. The cash outlays were planned well, and everything was sorted. This time too he assumed that he would be able to service the home loan. But unfortunately, luck isn’t in his favour. He is finding it difficult to get another job at the same salary. And is unable to make the regular EMI payments.

Sadly, he does not even have an insurance on home loan amount.

Consider Akash's plight. Such stressful nature of this situation can lead people to panic, or worse.

Have you ever been in such a situation? Or are you going through it and embossed to even face it.

Then be assured that all is not lost! It is possible to grow out of such a crisis.

To read more about this story and Personal FN’s views over it, please click here.

PNB Fraud: Which Mutual Funds Have Exposure To PNB? Know Here...

Impact

Mutual funds are not immune to corporate frauds and have seen their share.

Corporate frauds can often go unnoticed for years; thanks to unethical employees and corrupt auditors.

However, when these scams are unearthed, investors dump the stock. Mutual funds with exposure to such stocks suffer the most.

Despite having a rigorous process to pick stocks with the best corporate governance practices, mutual funds are no better equipped to handle sudden scam-shocks.

On February 14, Punjab National Bank (PNB) disclosed that it had discovered fraudulent and unauthorised transactions totalling Rs 11,300 crore at their Mumbai branch. This was pursuant to an investigation after a complaint was filed on January 29. Over the next few days, the PNB stock lost more than one-fifth of its value.

A PNB official had filed a criminal complaint with Central Bureau of Investigation (CBI) against three companies, Solar Exports, Stellar Diamonds and Diamond R US, and four people, including Nirav Modi and Mehul Choksi, the managing director of Gitanjali Gems, saying they had defrauded the bank and caused a loss of Rs 280 crore.

PNB’s Rs 11,300 crore fraud has allegedly been perpetrated by its staffers – Gokulnath Shetty and Manoj Kharat. They are suspected of steering fraudulent loans to companies linked to billionaire jeweller Nirav Modi and entities tied to jewellery retailer Gitanjali, which is led by Modi's uncle, Mehul Choksi.

Other banks that are likely to be affected include the UCO Bank, Allahabad Bank, and State Bank of India (SBI), while Axis Bank stated that it had already sold its exposure to Nirav Modi and his firms.

The UCO Bank said it has an outstanding exposure of about Rs 2,636 crore and that it was confident of receiving the payment. At the same time, Allahabad Bank has an exposure of around Rs 2,000 crore by way of Letter of Undertakings (LoUs) issued by PNB to Nirav Modi. The State-owned Union Bank of India said it has an exposure of around Rs 1,915 crore in the fraud, but stressed its money is safe and it will recover the funds.

To read more about this story and Personal FN’s views over it, please click here.

Why Putting Your Hard-Earned Money In Bank FDs May Not Be Safe

Impact

What’s wrong with India’s state owned banks nowadays?

Sure you have suite of answers!

The real challenge is to find what’s right with them.

Given the on-going PNB (Punjab National Bank) episode, nobody will believe that the problem of Non-Performing Assets (NPAs) is a result of poor loan underwriting. Scams and the abuse of power seem to be the biggest reasons for the current woes of asset quality with Public Sector Banks (PSBs).

Also, trusting PSBs with your hard-earned money would be equally difficult for many of you—you never know, PNB might just be the tip of the iceberg. In fact, the brazen behaviour of bank officials, their collusion with business houses and the corporate-political nexus makes the frauds unfathomable for now.

Prima facie, the recently reported fraud at PNB which is worth an astronomical value of Rs 11,400 crore won’t add to its NPAs. Although Mr Nirav Modi is a debtor of PNB, the presiding drama is about Letters of Undertakings (LoUs)—a guarantee given by PNB to overseas banks for Mr Nirav Modi’s group companies.

Collectively, All PSBs including PNB, have a collective exposure of over Rs 17,000 crore to Mr Nirav Modi’s group companies.

To read more about this story and Personal FN’s views over it, please click here.

FUND OF THE WEEK

HDFC Balanced Fund: Will Its High AUM Become A Burden On Its Returns?

HDFC Balanced Fund is among the few well-managed funds from the stable of HDFC Mutual Fund. Launched nearly two decades ago, the fund has consistently outperformed the benchmark across market periods, while maintaining a tab on risk. The fund boasts of a stable fund management, with Mr Chirag Setalvad being at the helm for over a decade.

With the equity market rally over the past few years, investors would be tad disappointed with the fund's returns. Over the past year, ended February 21, 2018, HDFC Balanced Fund generated a return of 16.31% in comparison to its benchmark return of 17.13%.

The longer-term returns of the fund are more encouraging. Over the longer periods of 3-years and 5-years, HDFC Balanced Fund has outpaced the Crisil Balanced Fund Index by a decent margin with returns of 10.76% and 18.92% respectively. The index generated a return of 8.19% and 12.12% over the same period.

Click here to read the complete note!

And Other News...

Nearly 6 crore subscribers of the Employees’ Provident Fund (EPF) will be affected by the EPFO ’s (Employees’ Provident Fund Organisation) decision of paying 8.55% interest for the Financial Year (FY) 2017-18. This is the third consecutive fall in the interest rate. In FY 2015-16, investors had received 8.80% interest; and in FY 2016-17, they had settled for 8.65%.

TUTORIALS:

Mutual Fund Direct Plans - Everything You Need To Know

Financial Terms. Simplified.

Haircut: A haircut is the difference between prices at which a market maker can buy and sell a security. The term comes from the fact that market makers can trade at such a thin spread. The term may also refer to the percentage by which an asset's market value is reduced for the purpose of calculating capital requirement, margin and collateral levels.

Quote: "It’s far better to buy a wonderful company at a fair price, than a fair company at a wonderful price."‒Peter Lynch