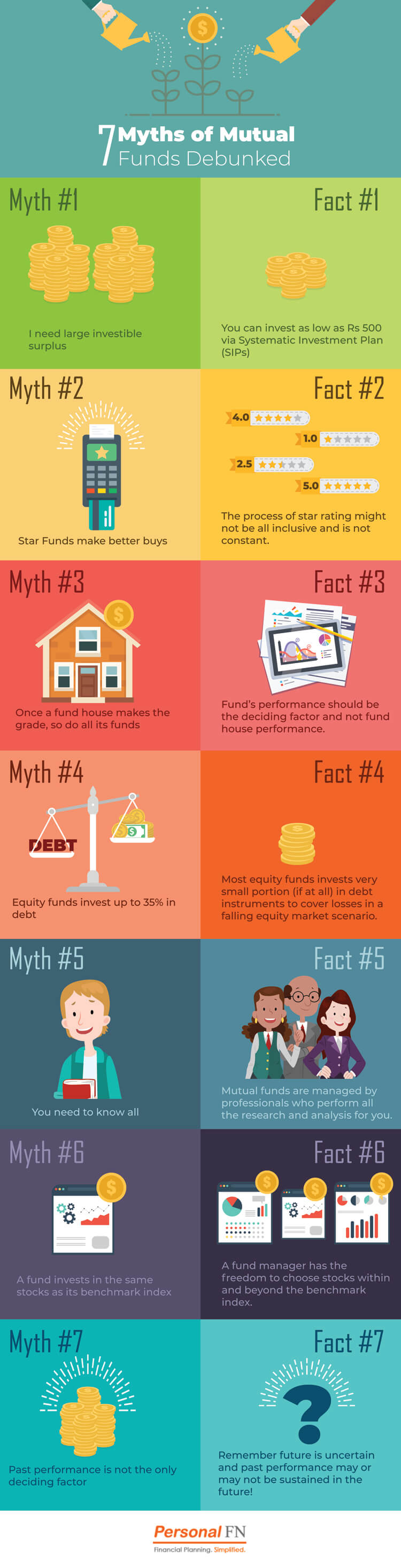

“Myths and creeds are heroic struggles to comprehend the truth in the world.” - Ansel Adams

In the world filled with information galore and cultural change, many of us develop our own set of beliefs and judgements. While that’s great to do, it is vital to recognise whether you are living with plain truth or mere delusions.

In the world of investments too, today we are exposed to galore of information. Take for instance when you step out for a social gathering; you may have come across individuals discussing about the stock markets, which sectors to invest, which market capitalisation segment (i.e. large caps, mid caps or small caps) to invest in, or simply even which avenue of investment to deploy money. And mind you, while we do recognise that while everyone has view on all these, we think that for your financial well-being it is necessary that you conduct enough research, thus enabling you take a wise investment decision suiting your investment objectives. This is because if incorrect information sometime shared by your friends and broker, may blind your ability to understand things in the right perspective, thus guiding you on the wrong path.

In the present volatile market conditions, while there’s lots talked about the market outlook it imperative for you not only to take a well informed decision, but also be free from myths. As in our last article while we have explained you how Systematic Investment Plan (SIPs) can help you manage the market volatility, over here we thought of sharing some of the common myths which we have experienced some investors have while approaching SIPs.

Myth no. 1 : Only Small investors go in for SIP

Please note that SIP stands for Systematic Investment Plan (SIP) and not Small Investors Plan. Hence, it is incorrect to be under the delusion and arrogance that SIP, is meant only for small investors.

Remember those good old days, where our parents subscribed us to a good, regular saving habit by buying us a piggy bank, where we all saved some money every day or week or month to build a corpus at the end of a particular period. But the fact was the regular deposits in your piggy bank, did not earn a rate of return.

In case of SIPs (Systematic Investment plans) too, if you go by the same logic of the piggy bank, you would realise that your money saved in a systematic manner – may be daily, monthly, quarterly, for a said tenure (period of SIP) will help you to build a corpus earning a rate of return, in order to attain your financial goal.

Myth no. 2 : Rupee cost averaging can be done in a stock itself – then why SIP?

It’s noteworthy that, certainly you can bet on equity, but diversification through mutual funds would help you to reduce the stock specific risk which you are exposed in direct equity (stocks). Moreover, as per the market cap bias (i.e. large cap, mid cap and small cap) which a fund follows, you can also strategically structure your portfolio depending upon your risk appetite. Similarly, you can structure your portfolio on the basis of the style (viz. value, growth, blend, opportunities, flexi-cap, multi-cap etc.) of investing followed by the mutual fund. And by adopting the SIP mode of investing for mutual funds, you’ll benefit from rupee cost averaging and compounding.

Remember a SIP experimented on single scrip, can expose you to more volatility unlike SIP in mutual funds which reduces the risk, due to diversification provided by mutual funds.

Myth no. 3 : SIP mutual funds are different from lump sum mutual funds

Well many have this delusion. The fact is, there are no special schemes for SIP investments. SIPs are just a mode of investing. You can enrol for a SIP in any mutual fund scheme, but ideally you should select a mutual fund taking into account the qualitative parameters such as investment processes and system, fund manager’s experience, uniqueness of the products etc., along with quantitative parameters such as returns, risk, average AUM (Assets Under Management), liquidity, expense ratio, portfolio characteristics etc.

Remember, there’s more than just a return while selecting a mutual fund scheme for your portfolio.

Myth no. 4 : Lump sum investments cannot be done in a scheme, where a SIP account exists

It is noteworthy that SIP, is just a mode of investing in mutual funds. Hence, pumping a lump sum amount to a mutual fund where your SIP exists is possible. So, say you have a SIP of Rs 1,000 going on in a mutual fund scheme and suddenly you have a surplus of say Rs 50,000, then you can pump a lump sum amount to your ongoing Rs 1,000 SIP account.

Myth no. 5 : I’ll be penalised if I miss one or two SIP dates

While enrolling for the SIP mode of investing you are required to provide your ECS mandate form along with the common application form. Your SIP details (as selected) are already mentioned in the ECS mandate, thus your bank at regular SIP dates keeps debiting the SIP amount in favour of the fund where you have opted a SIP. Hence, the question of missing dates doesn’t arise. Now for some reason if you are not maintaining a balance in your bank account for your SIP to be debited, you would simply miss that SIP instalment, but your SIP account will remain active and further SIPs (subject to your bank balance) will be debited to your bank account. So, it’s not like the EMI (Equated Monthly Instalment) of your loan, where you miss an instalment; you are penalised. Remember, SIP infuses discipline in investing and is entirely at your free will.

Myth no. 6 : I’ll accumulate through SIP and liquidate through SWP during retirement.

Well, if you adopt this financial planning strategy, you are bound to face nightmares during your retirement. It is noteworthy that, as you approach retirement your appetite for risk reduces, as your number of years of earning life decreases. Hence having savings lying in equity mutual funds during retirement years can be risky. In order to maintain a lifestyle post-retirement, you should transfer your savings to low risky asset classes such as debt and cash from a high risk asset class like equity.

Remember to adopt the right strategy while planning your finances - think wise!

Myth no. 7 : Markets are high to start a SIP

Well, if that’s what you think, then you should be starting a SIP immediately. That’s because as the market corrects you would by accumulating more number of units, with every fall in the NAV, thus enabling you to lower you average purchase cost. And, as the markets, post the correction surge once again, you would gain as the yield will work to be higher.

Remember by adopting the SIP route for mutual fund investments, you are shielding your portfolio against the wild swings of the markets. Don’t unnecessarily try to time the markets as it is not always possible.

Myth no. 8 : In a tax saver SIP, entire money can be withdrawn after 3 years

In case of a SIP in tax saving mutual funds (commonly known as Equity linked Saving Schemes – ELSS), very often a delusion exists that, the entire investment in a tax saving mutual fund can be withdrawn once the lock-in period is over. But that’s not the case!

The fact is: your every instalment of SIP should have completed the lock-in tenure. So say if you put in Rs 5,000 through SIP in the month of January 2012, the lock-in period for only 1 instalment (i.e. January 2012) will get over on Janaury2015. While other SIP instalments need to complete 3 years as well.

This article was written exclusively for Equitymaster, India's leading Independent research initiative. Trusted by over a million members all over the world, Equitymaster is known for its well-researched, unbiased and honest opinions on the Indian Stock Market.

Disclaimer: This note / article is for information purposes and Quantum Information Services Limited (PersonalFN) is not providing any professional / investment advice through it. The recommendation service, views, articles and other contents are provided on an "As Is" basis by PersonalFN. The facts mentioned in the note are believed to be true and from a public source. The Service should not be construed to be an advertisement for solicitation for buying or selling of any scheme / financial product. PersonalFN disclaims warrants of any kind, whether express or implied, as to any matter/content contained in this note, including without limitation the implied warranties of merchantability and fitness for a particular purpose. PersonalFN and its subsidiaries / affiliates / sponsors / trustee or their officers, employees, personnel, directors will not be responsible for any direct/indirect loss or liability incurred by the user as a consequence of his or any other person on his behalf taking any investment decisions based on the contents of this note. Use of this note is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. PersonalFN does not warrant completeness or accuracy of any information published in this note. All intellectual property rights emerging from this note are and shall remain with PersonalFN. This note is for your personal use and you shall not resell, copy, or redistribute this note, or use it for any commercial purpose. Please read the terms of use.

Add Comments

| Comments |

geevis@operamail.com

Dec 30, 2011

This information about SIP is indeed useful. But how useful is an SIP during rising markets and then at the end of SIP period there is a crash in markets? |

research@personalfn.com

Jan 13, 2012

Dear Gee,

In case you have an ongoing SIP and the markets rise, you end up buying at a high price and thus effectively get less number of units in your kitty. Thus effective rupee-cost averaging may not happen in the SIP route of investing in case of rising markets.

But having said that one should recognize that since volatility would always be an integral part of the markets, the risk is well managed.

If you enrolled for an SIP in case of rising markets, and at the end of SIP period the markets witness extreme volatility or crash, then as mentioned earlier effective rupee-cost averaging may not happen, resulting in ordinary returns (or sometimes even a loss). But if you have enrolled for a longer term period of time, and also stayed invested in the long-term you would get sweet fruits for investment made. However, while you investing in mutual funds create wealth in the long-term it is vital for you to have winning mutual fund schemes which have a consistent performance track record, and which are from fund houses which follow strong investment processes and systems. Its is only then you will receive a sweet fruit for the seed you sowed. |

1