(Image source: Image by Linda Hamilton from Pixabay)

(Image source: Image by Linda Hamilton from Pixabay)

Gold, one of the purest naturally occurring precious metals, is mentioned in a variety of expressions; most often it's associated with intrinsic worth. Over the years, it hasn't lost its sheen and still remains the most lucrative element to invest in, owing to the fact that people continue buying physical gold.

However, in current times, investing in gold isn't restricted only to buying physical gold. It has evolved, and one can invest in it in either of three ways - Sovereign Gold Bond, Gold funds (Gold ETFs and Gold savings funds), and Physical Gold. The first two options are alternative to buying physical gold, but they differ.

Gold Sovereign Bond Scheme: In order to encourage passive but direct gold investment, as an alternative to purchasing physical gold, Modi led Government sanctioned a Sovereign Gold Bond Scheme in November 2015. Under this scheme, investors have to pay the issue price in cash and the bonds will be redeemed in cash on maturity. The Bond is issued by the Reserve Bank on behalf of Government of India.

With the Sovereign Gold Bond Scheme, the risks and costs of physical storage are eliminated. Plus, it is free from issues like the costs of making charges and purity, as in the case of gold in jewellery form. But these bonds are held in the books of the RBI, or in demat form to eliminate even the risk of loss of scrip, etc.

Sovereign Gold Bonds will generate market returns linked to the price of gold, so there may be a risk of capital loss if the market price of gold declines. Moreover, these bonds will provide interest income at the rate of 2.50 per cent (fixed rate) per annum on the amount of initial investment to investors and will be redeemable.

The Bonds are issued in denominations of one gram of gold and in multiples thereof. Minimum investment in the Bond shall be one gram, with a maximum limit of subscription of 4 kg for individuals.

These bonds are sold through offices or branches of Nationalised Banks, Scheduled Private Banks, Scheduled Foreign Banks, designated Post Offices, Stock Holding Corporation of India Ltd. (SHCIL), and the authorised stock exchanges, either directly or through their agents.

For subscription to SGB, the government issues it in the form of a series of tranches for an initial investment amount of Rs 20,000. However, one can purchase units from the secondary market as well.

Recently, a tranche of 2019-20 Series III was offered for a limited subscription period, having a maturity tenure of 8 years and a lock-in period of 5 years. On maturity, the Gold Bonds shall be redeemed in Indian Rupees and the redemption price shall be based on a simple average of the closing price of gold of 999 purity of previous 3 business days from the date of repayment, published by the India Bullion and Jewellers Association Limited.

Now the next tranche of a subscription is available for the month of September.

Do note, that the interest on the bonds is taxed as per the provisions of the Income-tax Act, 1961. If you hold the SGB till maturity the capital gains tax on redemption of SGB is exempted.

But if you sold the bond in the secondary market after three years, long term capital gains (LTCGs) tax is applicable and it will be taxed at 20 per cent with indexation. And if sold before three years a short-term capital gains (STCGs) tax will be applicable and is according to the income tax slab.

Gold Funds: Both, gold ETF and a gold savings fund, are smart ways to invest in gold without actually tangibly holding it as you do not have to face storage problems or worry about theft.

-

Gold Exchange Traded Fund: Gold ETFs track prices of physical gold. Each unit of gold in the fund you can buy is equal to 1 gram of gold (some fund houses also offer 1 unit at 0.5 gram of old).

When you buy a Gold ETF, you get a contract indicating your ownership in gold equivalent to the rupee amount of your investment. A few gold ETFs give the option of taking physical delivery and some don't; and if they do, it's only after it exceeds a certain quantity.

Gold ETFs are passive investment instruments that are based on gold prices and invest in gold bullion. Because of its direct gold pricing, there is complete transparency on the holdings of an ETF. Further, due to its unique structure and creation mechanism, the ETFs have much lower expenses as compared to physical gold investments.

ETFs trade on the cash market of the National Stock Exchange, like any other company stock, and these can be bought and sold continuously at market prices. All you need is a trading account with a share broker and a demat account. One may either buy in a lump sum or even at regular intervals through systematic investment plans (SIP). What's more, you may even buy 1 gram of gold monthly.

[Read: Are SIPs Better Than Lumpsum Investments? Know Here...]

When you invest in a gold ETF, you get an opportunity to invest in standard gold bullion of 99.5 per cent purity. Besides, there is no exit load involved.

From a tax perspective, it is like that of physical gold. If you sell a gold ETF unit within three years, there will be a short-term capital gains tax applicable based on your income tax slab.

While if a Gold ETF unit sold after 3 years, a 20 per cent long term capital gains (LTCG) tax with indexation, i.e. adjusting for inflation on capital gains is applicable.

-

Gold Savings Fund : This is also known as a "gold fund" and it is another unconventional way to invest in gold. A gold savings fund is a fund of fund scheme that invests its corpus into an underlying Gold ETF which benchmarks the performance against the physical prices of gold. Hence, by doing so the returns closely correspond to the one clocked by the underlying gold ETF.

[Read: Why Dumping Gold ETFs Now Is Stupid!]

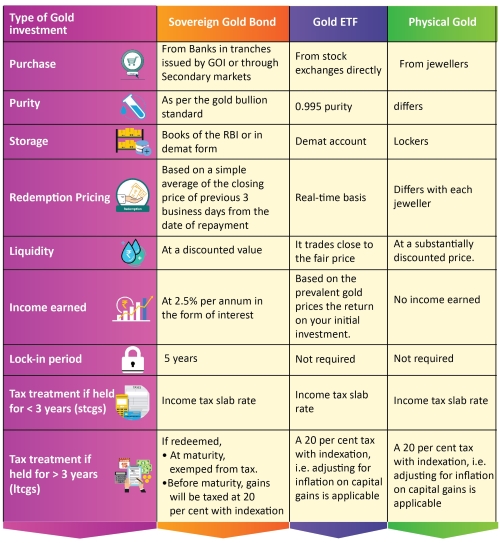

Table 1: SGB vs Gold ETF vs Physical Gold

(Illustration purpose only)

Why you should consider investing in gold?

Gold as an asset class is looked upon as one of an important strategic asset class that offers an effective hedge as a safe haven during global uncertainty and a shield against inflation. Most importantly in your portfolio, it serves as a diversifier.

Gold is being held by most central banks as a part of the reserve management. Of late, several central banks across the globe have purchased and stacked it.

[Read: Here's Why You Should Be Stacking Up Gold as Central Banks Do...]

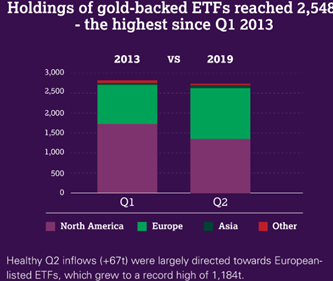

Recent data released by World Gold Council points that,

-

Gold demand was 1,123t in Q2, up 8% y-o-y. H1 demand jumped to a three-year high of 2,181.7t, largely due to record-breaking central bank purchases.

Graph 1: Global Growth in Gold-backed Holdings Since 2013

(Source: World Gold Council)

-

Gold supply grew by 6% in Q2 to 1,186.7t. A record 882.6t for Q2 gold mine production and a 9% jump in recycling to 314.6t - boosted by the sharp June gold price rally - led the growth in supply. H1 supply reached 2,323.9t - the highest since 2016.

-

Holdings of gold-backed ETFs grew 67.2t in Q2 to a six-year high of 2,548t. The main factors driving inflows into the sector were continued geopolitical instability, expectation of lower interest rates, and the rallying gold price in June.

-

A strong recovery in India's jewellery market pushed demand in Q2 up 12% to 168.8t. A busy wedding season and healthy festival sales boosted demand, before the June price rise brought it to a virtual standstill. Indian demand drove global jewellery demand 2% higher y-o-y to 531.7t.

While demand for physical gold in India (particularly from bars, coins and jewellery) is up, globally, investors are adding gold in paper form via ETFs as well. AMFI data released, shows AUM of Gold ETF stood at Rs 5,080.47 crore as on July 31, 2019.

[Read: 4 Reasons For Gold Getting All The Attention These Days]

But why is gold getting the spotlight all of a sudden?

As mentioned earlier, it's arguably the safest asset class that mitigates inflation. Though many headwinds are at play-- the weak global economic outlook amid the continued escalating US-China trade war tensions, feeble US dollar, and downbeat Asian equities has lifted the metal's safe haven appeal for investors; and, in turn, boosted prices. However, one can't eliminate the apprehensions of slower global growth that continue to plague the economy, will provide support to inflated gold prices.

The approach of...

Investing in gold in paper form can prove to be more effective. One should consider allocating at least 5-10% of your entire investment portfolio to gold and holding it with a long-term investment horizon will prove to be sensible and a smart investment strategy.

Avoid a speculative approach while investing in gold. Look at it as a portfolio diversifier and a monetary asset (rather than a mere commodity), which can help you reduce risk to your overall portfolio with its trait of being a store of value in times of uncertainties. Ideally, invest in gold with a longer investment horizon.

Add Comments

| Comments |

emailsubcriptions9@gmail.com

Aug 25, 2019

Compared to your title - can you let readers know as to where is the answer of the question raised in your title to this article? |

1