Impact

In India, the penetration of mutual funds has been abysmally low with only one crore unique investors. On the other hand, there are close to 60 crore bank account holders. This number includes nearly 20 crore accounts added under Jan Dhan Yojana.

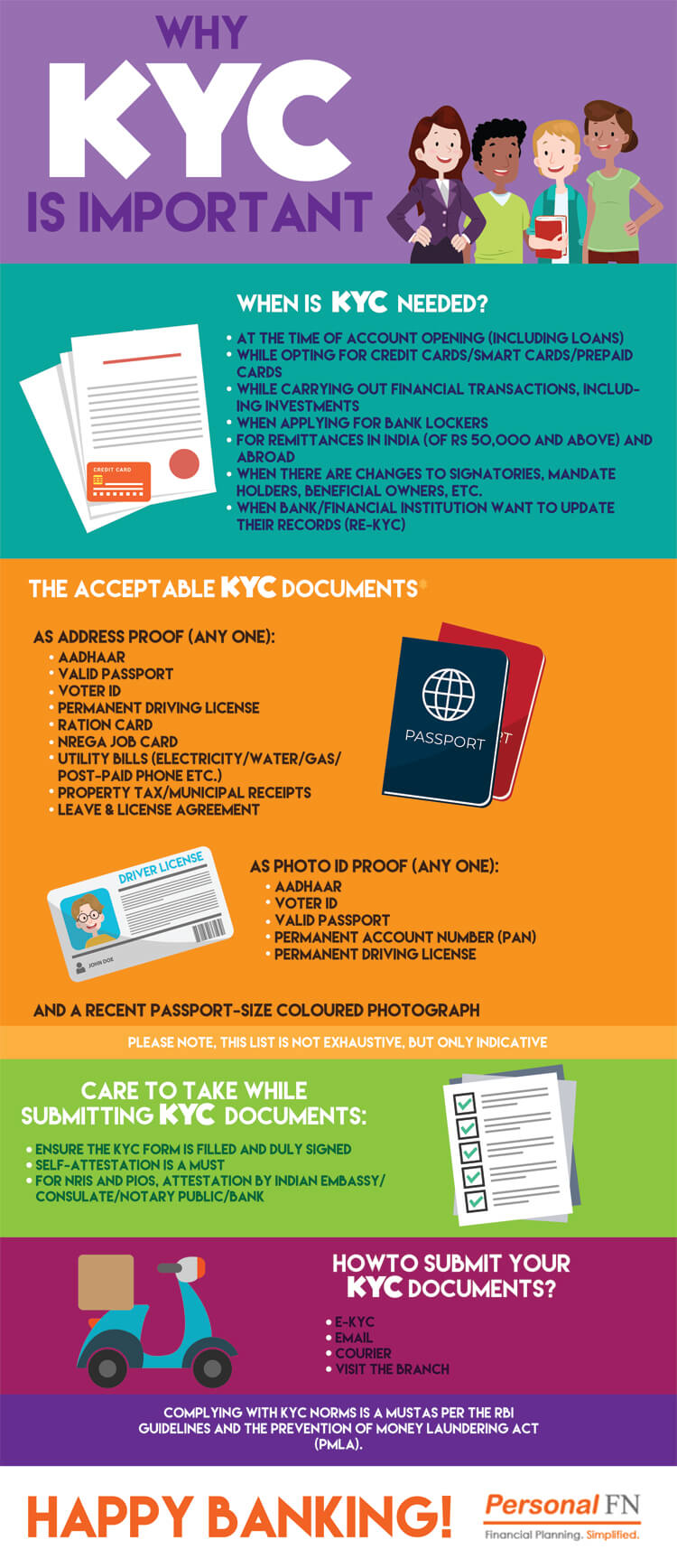

Recently, SEBI wrote to the Finance Ministry seeking a nod for allowing mutual funds to accept investments on Bank’s Know Your Customer (KYC). At present, mutual fund houses are expected to collect a separate set of documents before taking any investment from the first-timer. Many industry experts believe that allowing investors to invest in mutual funds using their bank KYCs will encourage greater participation. They opine that Indian investors are extremely sensitive about divulging personal details.

PerosnalFN believes it is a good suggestion. If the Finance Ministry gives SEBI the go-ahead on its proposal, investing in mutual funds will become easier. However, this highlights another point.

PerosnalFN believes it is a good suggestion. If the Finance Ministry gives SEBI the go-ahead on its proposal, investing in mutual funds will become easier. However, this highlights another point.

And that is,

People are ready to share their personal details at the time of opening a bank account. (as they feel bank account is a necessity.)

But

When it comes to mutual funds, they prefer to keep their personal details secret (forgoing the benefits of investing in mutual funds?) In other words, investors are inadequately informed of mutual funds. PersonalFN is of the view that, educating the investor is the only way ahead. Doing away with separate KYC for mutual fund investing may initially help mutual funds grow their reach, but they may again get stuck after a point. Mutual funds may help an investor create long-term wealth. Many people do not recognize this. It remains to be seen what initiatives mutual funds take to impart financial literacy.

PersonalFN has something to share with investors

- Don’t speculate. Only invest

- Don’t try to time the market. Invest regularly

- Know your risk appetite before investing

- Invest for the fulfillment of your financial goals

- Create a suitable asset mix

- Assess the performance of competing schemes before investing

- When investing in equity oriented schemes, invest only for long term

- Don’t forget to review your portfolio periodically

Hopefully, mutual funds will take investor education more seriously rather than roll out more New Fund Offers (NFOs).

Impact

The National Pension System (NPS) is not as popular as the Employees’ Provident Fund (EPF) is Out of the total asset base of Rs 1 lakh crore, nearly 90% of NPS’ assets belong to central and state Government schemes. It seems the Pension Fund Regulatory and Development Authority (PFRDA) wants to introduce some changes to improve the competitiveness of NPS.

Proposed changes...

- The PFRDA, a regulator, is considering allowing government employees to invest up to 50% of their contribution in equity. The same is currently capped at 15%.

- Furthermore, it may also permit government employees to opt for personal-fund manager services. At present, there are only 3 state-run fund managers managing pension money of public sector employees.

- There’s another proposal—to appoint a fund manager for 5 years as against the prevailing practice of 3 years.

The PFRDA has invited comments on these proposals from various stakeholders. It is hopes to gain the Government’s acceptance. The NPS has done well in the last 5 years and managed to outperform EPF. They are of the view that allowing greater participation in equity may increase the returns for government employees.

PersonalFN believes, making comparisons between NPS and EPF would be inappropriate as the latter invests only in fixed income instruments. Moreover, even if the Government allows government employees to invest up to 50% of their pension contribution in equity, the age of the contributing employee would matter. For example, a person who has just 2 years left to retirement shouldn’t ideally take 50% exposure in equity, even if it is permitted.

Importantly, the tax treatment for NPS makes it unattractive more than anything else. Instead of considering this aspect, the Government tried to impose a tax on EPF in Budget 2016-17. In the absence of any other social security scheme, imposing a tax on pension money appears less convincing.

Impact

As expected, the RBI reduced policy rates at its first bi-monthly monetary policy meeting for the Financial Year (FY) 2016-17. While the market’s anticipations and analysts’ estimates were running wild with <a data-cke-saved-href="https://www.personalfn.com/knowledge-center/fixed-income/fip-views-on-news/16-03-16/a_" href="https://www.personalfn.com/knowledge-center/fixed-income/fip-views-on-news/16-03-16/a_" wide_net"_perspective_why_dr_rajan_would_cut_policy_rates_soon.aspx?utm_source="website&utm_medium=home?utm_source=FNS&utm_medium=Mailer&utm_campaign=FNSTracking"" style="color: #fd7319;" target="_blank">the consensus building around a minimum of 50 bps of a rate cut, the actual rate cut came in at 25 bps. One basis point is a hundredth of a percent.

Monetary Policy Action at Glance:

- RBI reduced the policy repo rate from 6.75% to 6.50%

- It narrowed the policy rate corridor from 100 bps to 50 bps by cutting the MSF rate by 75bps and increasing the reverse repo rate by 25 basis points,

- Reverse repo is adjusted to 6.0% and Marginal Standing Facility (MSF) to 7.0%

- The central bank lowered the minimum daily maintenance of the Cash Reserve Ratio (CRR) from 95% of the requirement to 90% with effect from the fortnight beginning April 16, 2016.

- CRR is unchanged at 4.0%

The RBI introduced many changes to the liquidity management framework as well as bringing in new measures to strengthen the banking structure, broadening and deepening financial markets while extending the reach of financial services to all. The central bank’s assessment of growth, inflation and foreign exchange reserves has also been crucial.

In short, the first bi-monthly monetary policy may look disappointing if we focus primarily on 25 bps of a rate cut. However, if you look at the broader picture, the monetary policy has been extremely effective and may have a long-term positive impact on your borrowings, savings, and investments. Let’s have a look all these aspects one by one.

To ready more about this story and Personal FN’s views over it, please click here.

Impact

If you were asked to select one of two options, it may be easy to choose. Now, if the number of alternatives increased to 10; your job might become slightly tougher. Naturally so. You would have to understand pros and cons of all 10 options along with their suitability in the given context. How about selecting 5-6 from 2,266? It sounds crazy, doesn’t it?

Well, this is what people are expected to do if they plan to invest in mutual funds. As per the data published by Association of Mutual Funds in India (AMFI) on February 29, 2016, there are 2,266 schemes across 9 categories. So if you want to pick up 2 in Equity, 2 in debt, 1 in ELSS, and 1 in Gold, you have a herculean task at hand. You may always seek the experts views to figure out a winning mutual funds for your portfolio. PersonalFN has been doing this for years—without holding any bias for or against a particular fund house. At PersonalFN, research is driven by a well-established and tried-tested process.

To ready more about this story and PersonalFN’s views over it, please click here.

|

|

© Quantum Information Services Pvt. Ltd. All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of PersonalFN is strictly prohibited and shall be deemed to be copyright infringement.

Disclaimer: Quantum Information Services Pvt. Limited (PersonalFN) is not providing any investment advice through this service and, does not constitute or is not intended to constitute an offer to buy or sell, or a solicitation to an offer to buy or sell financial products, units or securities. All content and information is provided on an 'As Is' basis by PersonalFN. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. PersonalFN and its subsidiaries / affiliates / sponsors or employees, personnel, directors will not be responsible for any direct / indirect loss or liability incurred by the user as a consequence of him or any other person on his behalf taking any investment decisions based on the contents and information provided herein. This is not a specific advisory service to meet the requirements of a specific client. Use of this information is at the user's own risk. The user must make his own investment decisions based on his specific investment objective and financial position and using such independent advisors as he believes necessary. All intellectual property rights emerging from this newsletter are and shall remain with PersonalFN. This is for your personal use and you shall not resell, copy, or redistribute this newsletter or any part of it, or use it for any commercial purpose. The performance data quoted represents past performance and does not guarantee future results. As a condition to accessing PersonalFN's content and website, you agree to our Terms and Conditions of Use, available here.

Quantum Information Services Private Limited Regd. Office: 103, Regent Chambers, 1st Floor, Nariman Point, Mumbai - 400 021 Corp. Office: 101 Raheja Chambers, 213, Free Press Journal Marg, Nariman Point, Mumbai 400021. Email: info@personalfn.com Website: www.personalfn.com Tel.: 022 61361200 Fax.: 022 61361222 CIN: U65990MH1989PTC054667

|